_06_16_2026_04_54_27_535266.jpg)

Stock market lure investors, offering the opportunity to gain high returns given sound fundamental judgement, technical analysis, macro-analysis and prudent decision-making skills put in place. Given the ongoing global trade war concerns and low interest rate regime, one sector that is gaining immense traction among market enthusiasts has been Consumer Staple sector.

The benchmark index, S&P/ASX 200 Consumer Staples (XSJ) has soared by more than 20% this year. The sector primarily reflects stocks of those companies whose goods/services are always in demand, irrespective of the nature of business/economic cycle. These are typically essential products that are basic necessities of people to sustain their life, provided by businesses such as food & drug retailers, producers/sellers of tobacco, beverages, food, personal goods, etc.

Let us have a look at below mentioned five consumer staple stocks:

Freedom Foods Group Limited

Freedom Foods Group Limited (ASX: FNP) is a consumer food processing company that specializes in dairy- based and plant based nutritional products. The company operates in specialty cereal, snacks and seafood products. The company is also engaged in the marketing and logistics of its own products across Australia, New Zealand, China, South East Asia and North America.

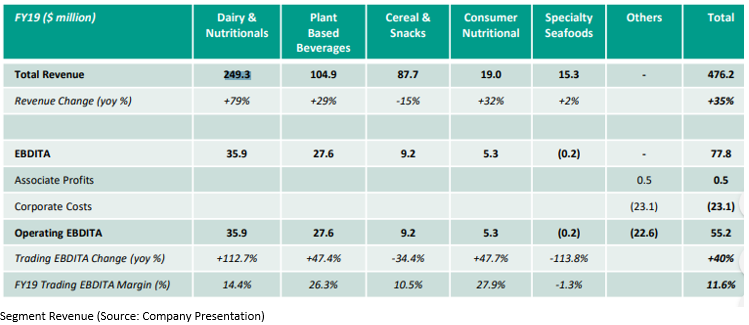

FNP recently reported its FY19 results for the year ended 30 June 2019 wherein it posted net sales revenue at $476.2 million, up 34.9% in FY18. Operating EBITDA for the period stood at $55.2 million, increase by 40.9% on the prior corresponding period. While, the companyâs net profit after tax on statuary basis for the period came at $11.6 million, a dip of 9% on y-o-y primarily due to inclusion of abnormal and non-cash expenses.

Operating performance: FNP delivered decent growth in the branded segment, well supported by distribution channels. The retail grocery segment in Australia posted above-average growth rates. In FY19, FNP formed a local team in SE Asia which aided ~178.8% growth. Sales from China were boosted by higher dairy volumes and came in at $67.4 million, up by 37.3%. Domestic sales increased by 37.5% y-o-y, well supported by 60.7% growth in dairy & organic segments. Grocery channel grew 37.8% y-o-y, driven by increased (NPD) market share. The company successfully launched pea protein milk in the Australian market, which won the âAFR Most Innovative New Productâ award.

The company distributed an unfranked half yearly dividend of AUD 0.0325 for each ordinary share held with a payment date of 2 December 2019 with the record date of 1 November 2019.

Outlook: The company estimated to produce more than 150 million litres during FY20. The management is looking to scale dairy capabilities and will focus on high value-added protein-based consumer products in the coming years. Capital expenditures are expected to be around $100million in the coming two years.

FNP is currently trading at $5.345, up 5.84% (as at 1:11 PM AEST, 2 September 2019). The stock is trading at a P/E multiple of 83.750x.

Inghams Group Limited

Inghams Group Limited (ASX: ING) is engaged in production, processing and sale of chicken and turkey products. The company also produces stock feed which is used for poultry, pig, dairy and equine industries.

On 28 August, ING informed to the market regarding Credit Suisse Holdings (Australia) as a substantial holder, holding 19,670,214 ordinary shares with a voting power of 5.29%.

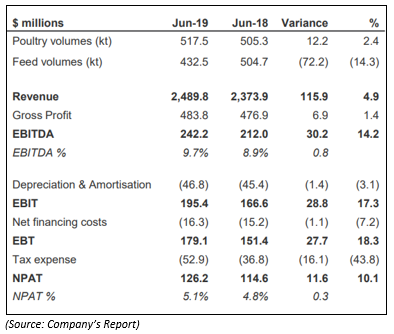

Financial Highlights for the year ended 30 June 2019: The company reported FY19 revenue at $2,489.8 million, a 4.9% y-o-y increase and a ~10% pcp rise in NPAT at $126.2 million. ING reported EBITDA at $242.2 million, up ~14.2% pcp while EBITDA margin improved at 9.7% compared to 8.9% during FY18. The company reported total borrowings at $398.3 million and net assets at $164.5 million in FY19.

Dividend: The Board declared final fully franked dividend of 10.5 cents per ordinary share with payment date of 9 Oct 2019 and record date of 18 Sep 2019.Operational performance: Core Poultry volumes stood at 414.9kt, increased by 4.3%. Feed volume due to the cycling of customer loss in March 2018 and the sale of Mitavite in October 2018. Higher customer demand created unexpected pressure on operations, which resulted in lower productivity and higher expenses. Operating performance in New Zealand was hindered by oversupply which resulted in flat core poultry volumes while the company could not pass the excess cost to the customers.

Outlook: The management cited that during FY20 the demand for poultry products will likely to be higher aided by the affordability of chicken as a healthy protein diet. Current feed costs are at historic highs, while the pricing of feed during FY20 will depend on the FY20 domestic grain harvest. Dividend policy for FY20 will remain a payout ratio of 60-70% of underlying NPAT (excluding leasing impact).

The stock of ING is trading at $3.170 at AEST 1:31 pm AEST on 2 September 2019. The stock is trading at a P/E multiple of 9.380x.

Synlait Milk Limited

Synlait Milk Limited (ASX: SM1) is engaged in production and processing of milk and other dairy products and is based in New Zealand.

Update from Supreme Court regarding a land purchase in February 2018: SM1 recently updated about the recent court hearing. As per the court, there will be a verbal discussion between the court and the company before the court announces its verdict on the decision made regarding the Pokeno site. The management cited that they are hopeful for the upcoming conversation and treated the court decision as a legal procedure.

Earlier in February 2018, SM1 purchased 28 hectares of land in Pokeno, located in Waikato District. The primary reason of purchasing the land was to set up the companyâs second nutritional powder manufacturing plant. But in November 2018, the High Court rejected the deal of setting up a manufacturing plant. During May 2019, the Court of Appeal court rejected the High Courtâs decision to remove historic covenants. In June, SM1 applied to the Supreme court for overturning the decision.

Stock performance: On 2 September 2019 (1:52 PM AEST), the stock of SM1 is trading at $8.620, down by $2.05% from its previous day close. The stock has a P/E multiple of 23.600x and has generated negative return of 13.47% in last six-months.

GrainCorp Limited

GrainCorp Limited (ASX: GNC) operates in agriculture segment and provides services like grain storage, distribution and freight services in Australia.

The company recently reported that Vanguard Group had purchased 11,493,404 units of an ordinary share, which represents 5.022% of voting rights. Vanguard is an asset management company, that manages mutual funds and accounts.

Recently, Australian Competition and Consumer Commission (âACCCâ) has notified GrainCorp Limited regarding its draft determination not to exempt GrainCorpâs Portland grain export terminal in Victoria under the Port Terminal Access. The management was not happy with ACCCâs move and informed about iâs intentions to associate with ACCC during the 28-day consultation period, due to the highly competitive exports market of Victorian grain.

Outlook: The company expects to post an underlying EBITDA in the range of $65-85 million for FY19 and an underlying net loss after tax in the range of $70-90 million.

Stock performance: The stock of GNC is trading at $8.00, up 0.125% from its previous day close. The company has a market capitalization of $1.83 billion and a total 228.86 million share outstanding. The 52-week trading range of the stock stood at $7.235 to $9.960 and currently, the stock is quoting at the lower band of its 52-week trading range. The stock has given a negative return of 8.16% and 17.80% in last one month and six-months, respectively.

Metcash Limited

Metcash Limited (ASX : MTS) is a retail-based company operating in the segments of Liquor, food and hardware.

On 29 August, MTS informed that Fiona Elizabeth Balfour ceased to exist as companyâs director with 87,804 fully paid ordinary shares.

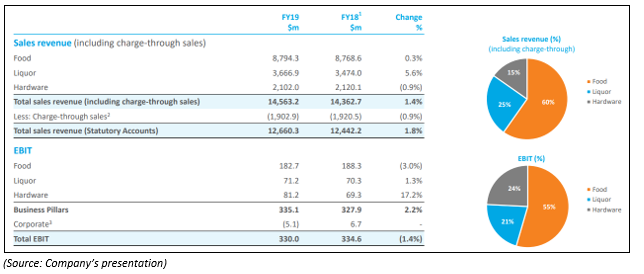

Reported FY19 Financial performance: The company recently posted its FY19 performance for the year ended 30 June 2019, wherein the company recorded an underlying net profit at $210.3 million, up 3% y-o-y. The company posted statutory revenue at $12,660.3 million, an increase of 1.8% on y-o-y basis while the companyâs EBIT came at $330 million, down 1.4% pcp.

Segment performance: Revenue from food segment during FY19 came flat at $8794.3 million compared to $8768.6 million in FY18 while EBIT from this segment was down by 3% at $182.7 million. Liquor revenue in FY19 was up by ~5.5% (y-o-y), EBIT came at $71.2 million (increase 1.3% y-o-y). Hardware business grew 0.9% (y-o-y) at $2102 million during FY19 and earnings before interest and taxes came at $81.2 million (up 17.2% y-o-y).

Stock update: The stock of MTS is trading at $2.855, down 1.55% from the previous day close. The stock has a P/E multiple of 13.940x.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.