The below-mentioned fashion retailers have produced strong results in the recent past. Letâs take a closer look at the financial and stock performance of these retailers.

City Chic Collective Limited (ASX:CCX)

A leading Australian multichannel retailer, City Chic Collective Limited (ASX: CCX) is primarily involved in retailing of women's fashion in Australia, New Zealand, USA, Germany and the UK. The company specialises in womenâs apparel, accessories and footwear market and has a network of 104 stores across Australia/New Zealand.

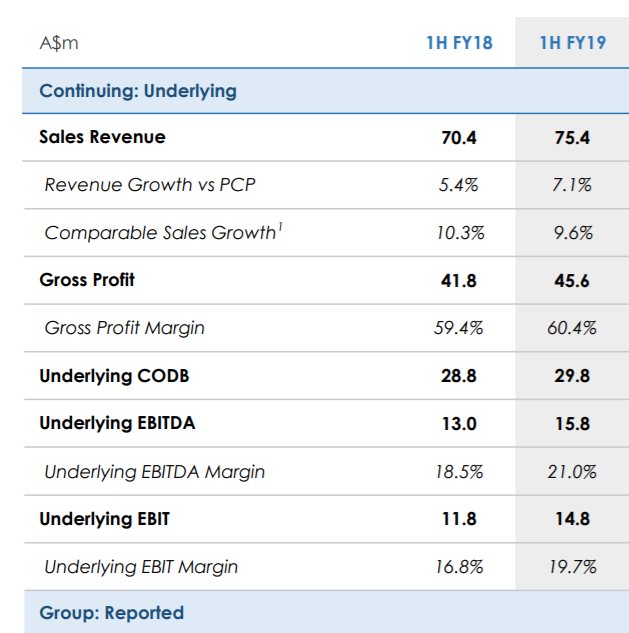

In the first half of FY19, the company reported sales revenue of $75.4 million, up 7% on the previous corresponding period, with comparable sales growth of 9.6%. Further, it earned an underlying EBITDA of $15.8 million, up 22% on pcp. The company witnessed an improvement in earnings margin driven by growth in online, tight cost control and exiting less profitable stores and concessions.

During the period, the company experienced strong momentum across all channels and regions. The companyâs online sales demonstrated a growth of 29% as compared to pcp, representing 40% on total sales. Moreover, the Cost of Doing Business (CODB) in the half year period reduced to 39.5% of sales. During the period, the companyâs top-line sales growth was impacted by the closure of loss-making stores in South Africa and Australia in 2H18, and US stores in September 2017.

During the period, the company successfully transitioned to standalone IT infrastructure allowing it to focus entirely on driving its growth strategy. During the period, the company continued to invest in its online platform and stores and expand its online exclusive range.

City Chicâs Financial Performance (Source: Company Reports)

During the period, the company declared an interim ordinary dividend of 2.5 cps and a special dividend of 2.5 cps, which was paid on 19th March 2019.

The company recently announced the resignation of Claudine Tarabay from the role of Company Secretary. Mark Ohlsson was appointed as Company Secretary, bringing more than thirty years of governance and corporate experience to the companyâs Board.

In the last one year, the companyâs stock has performed strongly, rising 149.33% during the period. In the last six months, the companyâs stock has provided a return of 76.90% as on 13th June 2019.

At market close on 14th June 2019, the stock of the company was trading at a price of $1.840, down 0.822% during the dayâs trade with a market capitalisation of ~$350.83 million.

Noni B Group (ASX:NBL)

Australiaâs leading specialty fashion retailer group, Noni B Group (ASX:NBL) is primarily involved in retailing of womenâs apparel and accessories.

In the first half of FY19, the company earned EBITDA of $29.1 million, up 31.4% on pcp. During the period, the companyâs sales increased by 140.4% to $464.4 million as compared to pcp, following the acquisition of five brands from Specialty Fashion Group on 2nd July 2018.

During the period, the companyâs Board declared a fully franked interim dividend of 9.0 cents per share, which is a fourth consecutive dividend for Noni B Group. During the half year period, the company completed the majority of the integration required across the Group, which included consolidating supply chains, systems and reporting as well as establishing a single support centre so learnings can be shared.

The company is on track to deliver the additional cost synergies of $20 million by 30th June 2019, which is over the achieved $30 million (on an annual basis). Additionally, the company is anticipating further efficiencies and margin improvements to add to the FY20 earnings. The company is expecting its full year EBITDA to be around $45 million, in line with the latest market consensus.

In last five years, the companyâs stock has performed strongly, rising 537.55% during the period, however, in the last one year, the stock of the company has provided a negative return of 3.05% as on 13th June 2019.

At market close on 14th June 2019, the stock of the company was trading at a price of $2.760, down 3.497% during the dayâs trade with a market capitalisation of ~$277.18 million.

Globe International Limited (ASX:GLB)

Globe International Limited (ASX:GLB) is a global producer and distributor specialises in purpose-built apparel, footwear and skateboard hardgoods with distribution and manufacturing centres in Melbourne, Sydney, Gold Coast, Los Angeles, Hossegor, Newport Beach, London and Shenzhen. The company has three major operating segments in Australia, North America and Europe. For over 30 years, Globe International has established a track record of successfully adapting to market changes and brand tastes.

In the first half of FY19, the company reported revenues of $78.1 mn and net sales of $77.9 mn, both up by 11% on the previous corresponding period, driven by the sales in Australasian and North American segments, which grew by 12% and 8%, respectively. In Australia, sales growth was primarily driven by the work-wear division. While the sales grew in North America, in Europe, sales decreased by 6% on pcp, mainly due to softness in the boardsports sector. Further, the company reported EBITDA of $5.0 million, up $0.9 million on the previous corresp onding period, driven by the increase in sales.

In the past few years, Globe Internationalâs strategies have enabled the company to keep improving and move forward despite various challenges. Itâs an exciting time for the company with the mix of relevant brands doing well in their respective diverse distribution channels as well as new brands and programs in development.

In last one year, the companyâs stock has performed strongly, rising 27.03% during the period, however, in the last six months, the companyâs stock has provided a negative return of 24.54% as on 13th June 2019. The companyâs stock last traded at $1.645, with a market capitalisation of circa $68.21 million.

Accent Group Limited (ASX:AX1)

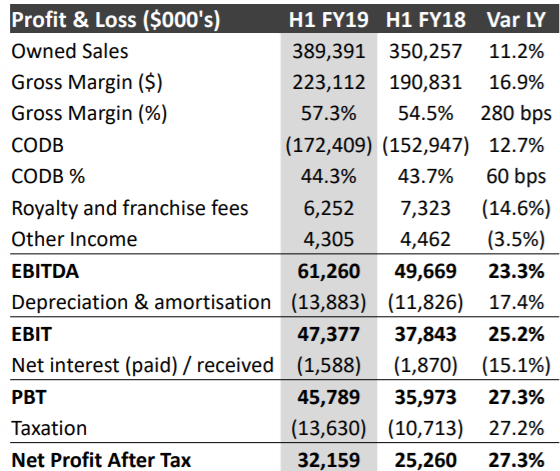

Accent Group Limited (ASX: AX1) is the regional leader in the retail and distribution of performance and lifestyle footwear, owning a powerful, scalable, end-to-end supply chain with direct access to brands and customers. In the first half of FY19, the company reported owned sales of $389.4 million up 11.2% on the prior year. The company reported total sales of $458.1 million, up 6.2% on the prior year. The gross margin of the company increased by 280 bps, and reached to 57.3%, demonstrating strong retail growth, vertical brands penetration and the strategy of reducing discount driven retailing compared to last year.

H1 FY19 Financial Summary (Source: Company Reports)

The companyâs cost of doing business increased by 12.7% during the period, driven by increased operating costs associated with new stores, the digital support team and implementation costs of TAF corporate stores. The companyâs total omnichannel sales increased by 94% in H1 FY19. This was on top of the 170% growth in the same period last year.

In last five years, the companyâs stock has performed strongly, rising 128.07% during the period, however, in the last six months, the companyâs stock has provided a negative return of 7.14% as on 13th June 2019. The companyâs stock was trading at a price of $1.290, with a market capitalisation of circa $703.61 million as on 14th June 2019. AX1âs stock is trading at a PE ratio of 13.730x, with a dividend yield of 6.35%.

Lovisa Holdings Limited (ASX:LOV)

The companyâs cost of doing business increased by 12.7% during the period, driven by increased operating costs associated with new stores, the digital support team and implementation costs of TAF corporate stores. The companyâs total omnichannel sales increased by 94% in H1 FY19. This was on top of the 170% growth in the same period last year.

In last five years, the companyâs stock has performed strongly, rising 128.07% during the period, however, in the last six months, the companyâs stock has provided a negative return of 7.14% as on 13th June 2019. The companyâs stock was trading at a price of $1.290, with a market capitalisation of circa $703.61 million as on 14th June 2019. AX1âs stock is trading at a PE ratio of 13.730x, with a dividend yield of 6.35%.

Lovisa Holdings Limited (ASX:LOV)

A fashion company, Lovisa Holdings Limited (ASX: LOV) is primarily involved in the retail sale of high quality fashion jewellery and accessories.

In the first half of FY19, the company reported EBIT of $36.5 million, up 5.1% on pcp. The companyâs total sales were up 12.3% and comparable store sales were down by -1.8% in the half year period as compared to pcp, impacted by continued tougher trading conditions in the Australian market and cycling strong first half last year comparable store sales of 7.4%.

During the period, the companyâs gross margin increased to 81% due to the benefit of currency tailwinds with continued disciplined promotional and inventory management. The companyâs gross margin was 81.0% in H1 FY19, up 60 basis points from 80.4% in the prior period, driven by the benefit of favourable USD hedge rates through the half combined with tight inventory and promotion management. The company is expecting that the currency headwinds will have an impact later in the later of FY19 and into FY20, as the companyâs average USD hedge rate reduces. In the period, the companyâs cash flow from operating activities lifted 9.4% to $49.1 million with operating cash conversion at 121%.

The company is focused on investment in people and processes to ensure that it remains efficient as it grows and able to execute on its strategic plans.

In last one year, the companyâs stock declined by 9.70%, however, in the last six months, the companyâs stock has provided a positive return of 46.93% as on 13th June 2019. The companyâs stock was last traded at a price of $11.280, with a market capitalisation of circa $1.16 billion as on 14th June 2019. The stock is trading at a PE ratio of 31.630x.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.