Summary

- Negative interest rates mean that commercial banks can charge money for an additional parking cash securely with the central bank.

- Adrian Orr, Governor of RBNZ, expressed willingness to take interest rates negative, indicating to continue to loosen monetary policy if required to fight back low inflation or deflation.

- RBNZ increased its quantitative easing program to NZ$100 billion while maintaining its cash rate at 0.25% during the Monetary Policy Meeting in August.

- The Market is predicting that OCR will fall to -0.5% from the present 0.25% in April 2021, Kiwibank economists remain far from convinced that interest rates will go negative and stated that it was not necessary.

The ongoing COVID-19 pandemic has hit businesses, disrupted supply chains, and threw the economies into a recession across the globe. Central banks of some of the leading countries are taking into consideration negative interest rates to combat the brutal decrease in economic activity and regain growth.

Interesting Read; NZ economy shrinks to most significant quarterly contraction in 29 years

Banks and financial institutions are obliged to pay interest for depositing excess cash to the central bank under a negative interest rate policy. Usually, interest is paid to the bank when someone borrows money, but the banks pay to the borrower when rates turn negative.

Countries that have adopted negative rates

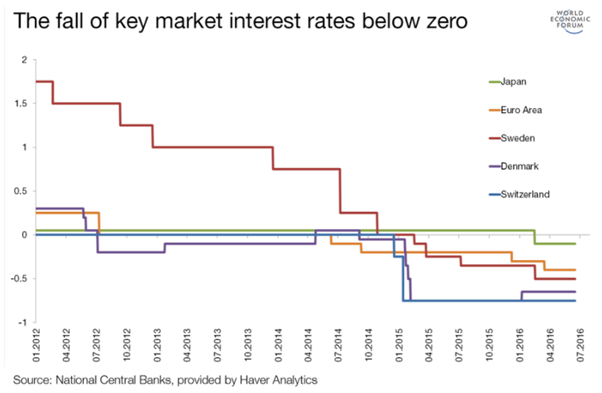

Many central banks have implemented an unmatched standard and non-standard monetary policy measures, lowering their key interest rates to 0, since the onset of the financial crisis in 2007. Many banks including the European Central Bank (ECB) and banks of Denmark, Sweden, Switzerland, and Japan have adopted negative policy rates to stimulate their economies characterised by low growth and low inflation, after the crisis.

The reason behind the banks opting for negative rates is that they provide additional monetary stimulus, giving banks an incentive to lend to the real sector and hence, supporting growth and a return to target inflation.

Source: The World Economic Forum, dated November 2016

Denmark was the first bank to take interest rates to negative in 2012. ECB adopted negative rates in June 2014 and slashed its deposit facility rates in small raises of 10 bps until it attained -0.5% in September 2019. After ECB, Bank of Japan followed suit.

Recently, COVID-19 has put a strain on central banks to consider negative rates. The US Federal Reserve has slashed the rates to just above 0 but has declined to go for negative rates. ECB has also not ruled out the possibility of negative rates as the bank stated that negative rates remain in the toolbox of possible monetary measures.

Recently, the Reserve Bank of New Zealand has expressed willingness in taking interest rates to negative territory.

Did You Read; What is the Street Anticipating from NZ Central Bank?

RBNZ willing to loosen up policy if required

Adrian Orr, Governor of RBNZ, has shown his openness to continue easing the monetary policy when needed to eliminate low inflation or deflation scenario, during a speech in Wellington on 2 September.

He stated that the pandemic arrived amid very low global inflation and historically low nominal interest rates, which reflected that the conventional policy of low interest rates had an only partial effect in counteracting a slump in economic activity.

ALSO READ: NZ Economic Charter: Three Silver Linings in the COVID-19 Cloud

Lockdowns imposed to control the spread of coronavirus have resulted in supply chain disruptions, which interrupted production and affected sales by lesser consumption. Households have not been able to buy regularly amid lockdowns, and as a precautionary measure, while businesses have been under pressure and worried about their existence.

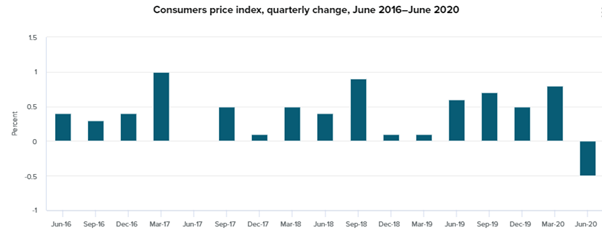

Coronavirus has given a jolt to demand and supply and has triggered disinflationary concerns. As per NZ Stats, consumer prices fell 0.5% in the June quarter compared to March quarter of 2020, taking the yearly inflation rate to 1.5% from 2.5% in previous quarter, which was just above the RBNZ’s inflation target range of 1-3%.

Source: Stats NZ

Mr Orr stated that if such deteriorating conditions persists for long, they can result in continued low inflation and higher unemployment. This sparked the need for more expansionary policies globally and in NZ. Hence, RBNZ’s monetary policy committee (MPC) decided that a ‘least regrets’ policy response was essential, and a significant easing of monetary policy was required.

ALSO READ: RBNZ's Balance Sheet To Expand Further In Response to COVID-19 | NZ Market Update

Hence, after the speech, investors have raised their bets on RBNZ, taking the official cash rate to negative. On 9 September, the 2023 New Zealand Government bond transacted at a negative yield of 0.025%, with the 2 and 3-year swap rates also falling below 0.

To know more, do read: New Zealand’s 2-year bond yield enters negative territory for the first time: Impact on the larger economy

Big Banks view on NZ’s move to negative interest rates

As per RBNZ’s Monetary Policy Statement of 20th August, MPC (Monetary Policy Committee) maintained OCR (Official Cash rate) at 0.25% and increased its Large Scale Asset Purchase (LSAP) programme up to NZ$100 billion.

The Committee expressed a preference to consider a package of negative interest rates and a Funding for Lending Programme (FLP) in addition to the LSAP programme.

Nick Tuffley, Chief Economist, ASB has stated that the economic activity would be confronting episodes of interruption until the spread of coronavirus is contained. He stated that RBNZ is expected to drop the OCR to below 0 by the next year.

ASB has predicted a fall to -0.5% from the present 0.25% for the first time to lift economic activity. The first interest rate hike is projected for early 2023, but the timing remains highly uncertain.

Westpac also believes that the OCR will drop to 0.5% in April 2021 stating that the cut will have the same effect as a conventional OCR cut. It stated that when OCR is already low, further cuts only reduce a part of the overall funding costs of the banks. Further, ANZ and BNZ also believes that there is a possibility for OCR to go negative.

ALSO READ: Are There Any Green Shoots Sprouting in the NZ Economy?

However, economists at the Kiwibank are not convinced of the negative OCR and think that the FLP programme of RBNZ is enough to reduce retail rates. They stated that the present economic conditions would not warrant negative rates and believes that negative OCR would not stimulate the demand for credit. Further, rates falling below 0 will also result in a drop in the profitability of the banking sector.

Further, RBNZ will declare its next update on 11 November.