Highlights

- Experts suggest that the RBA is likely to raise interest rates by June, which can be detrimental to households.

- Potential interest rate hikes can affect households holding a variable rate mortgage adversely.

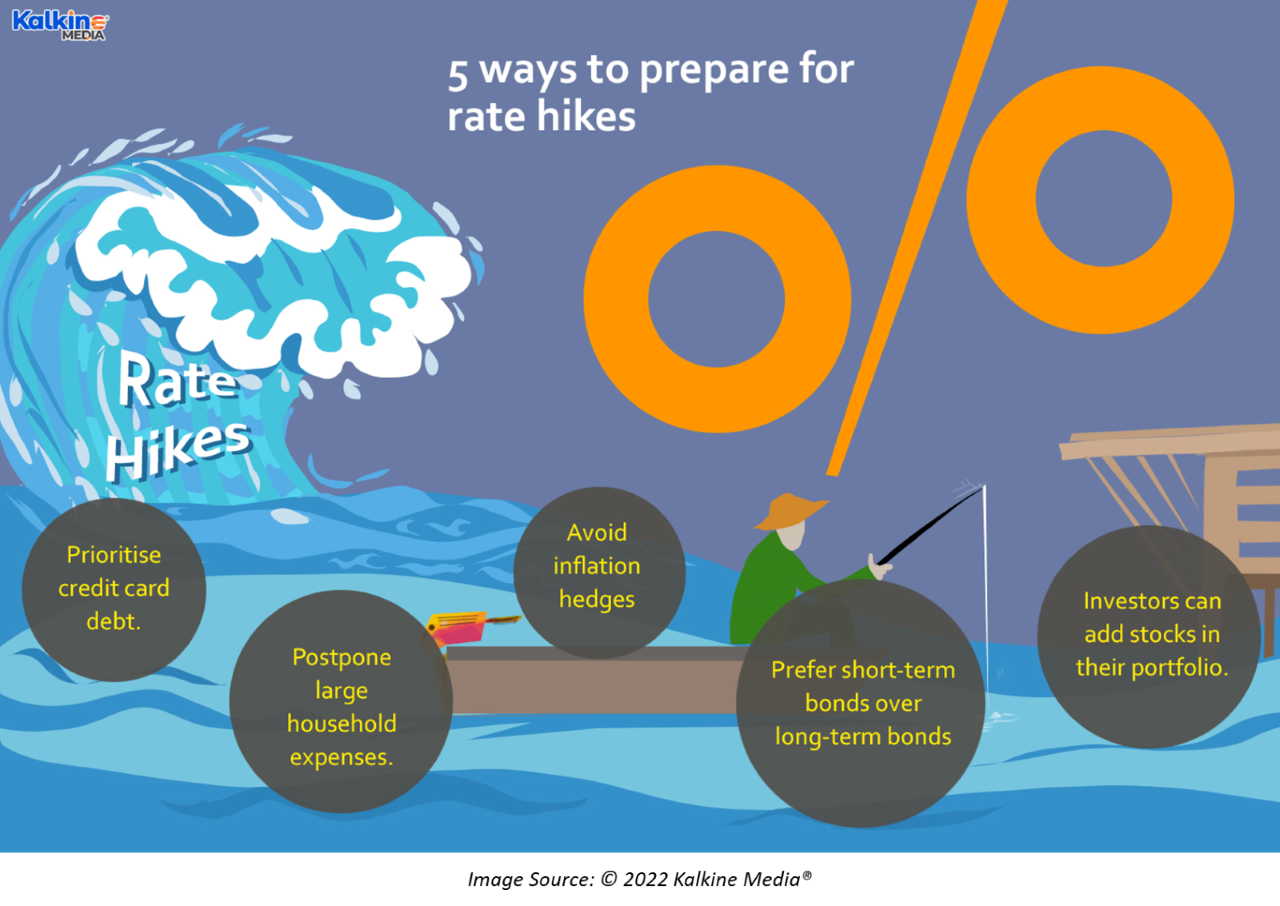

- Prioritising credit card debt, rescheduling expensive purchases and avoiding inflation hedges are some methods that can help sail through rate hikes.

As an interest rate hike decision by the Reserve Bank of Australia (RBA) approaches closer, loan holders need to be prepared to part ways from a considerable share of their income. Most financial markets expect the RBA to raise interest rates as soon as June after the wages data is released in May. However, the latest March quarter inflation numbers have fuelled speculations of an early rate hike in May. Once the interest rates are raised, multiple rate hikes are expected to follow suit this year.

Must Read: Three takeaways from Australia's March 2022 quarter inflation data

With inflationary pressures rising in the backdrop, consumers might be facing tougher choices ahead. Most mortgage owners in Australia hold a variable rate mortgage, under which the market rate applies once the fixed-rate period is over.

As interest rates keep rising, the interest amount would keep on piling up for mortgage holders. Managing household finances in such a scenario might become a challenging task for consumers. However, there are some methods to secure oneself from interest rate hikes.

Here are a few ways in which Australians can prepare for an interest rate hike in the coming days:

ALSO READ: Australia’s manufacturing PMI improves in April

Prioritise credit card debt

As interest rates rise, credit card debt becomes more and more difficult to manage. Banks generally charge a high interest rate on credit cards, which can soon demand hefty payments each month. Thus, it is crucial to take into account one’s credit card payments and tighten expenses on other items. Additionally, credit card holders can move away from minimum monthly installments toward higher installments.

Thus, the main goal is to do away with credit card debt as early as possible. Another alternative to paying credit card debt is to use the money sitting in a low-interest savings account. This money could be better utilised to pay high interest rate debt rather than being used as savings.

Reschedule large purchases

It goes without saying that rising interest rates are a sign of higher financing costs. Therefore, consumers can put off hefty purchases such as buying a car or a house. It is going to cost more to buy these items in a high interest rate environment.

Moreover, due to raging inflation, the prices of most household investment items are also increasing. This is especially visible in the housing sector, where housing prices have skyrocketed to record-high levels during the pandemic.

ALSO READ: Can Russia-Ukraine war derail Australia's economic recovery?

Steer clear of inflation hedges

During a low-interest rate and high inflation environment, hedges against inflation tend to perform well. These include commodities such as gold, and even real estate, which do not lose value even as inflationary pressures build. However, the scenario changes completely when interest rates are high, as these rates tend to ease inflation.

It will be enticing to see if prices of oil will also take a hit from a rise in interest rates. A decline in oil prices would be highly favourable in the current environment, where fuel prices have rapidly risen. Nevertheless, interest rate hikes might have little to no effect on fuel prices as supply-side pressures have mostly pushed the current inflation in oil prices.

Reduce bond duration

Investors can choose short- and medium-term bonds and reduce their holdings of long-term bonds while preparing for rate hikes. Short- and medium-term bonds are believed to be less sensitive to rate increases than longer-maturity bonds. Moreover, short-term bonds provide less income earning potential than longer-term bonds.

Investors can also pair shorter-term bonds with other instruments such as floating-rate debt, which includes bank loans.

Ponder on stocks

Companies that are major purchasers of raw materials also tend to perform well during high interest rate environment. Prices of raw materials may decline or remain stable when interest rates rise. Thus, companies involved in purchasing these materials tend to profit.

As a result, companies’ profit margins rise, benefitting their stock market performance. So, investors can also ponder on adding equities to their portfolios to obtain higher returns. However, proper fundamental and technical research must be conducted before adding a specific stock to the portfolio.

ALSO READ: How is higher cost of living impacting first home buyers in Australia?