.jpg)

Summary

- Myer Holdings has reported significantly lower profits compared to the previous year, largely due to non-cash impairments to intangible assets.

- With an accelerated trend towards online shopping, it has also adjusted its transition strategy to incorporate structural changes driven by the pandemic.

Myer Holdings released full-year number this morning for the period ended 25 July 2020.

Retail print by the Australian Bureau of Statistics (ABS) indicated normalisation in the clothing and footwear market in July. The pandemic impacted this class of retailers significantly.

Today MYR shares opened lower over a tenth of previous close after a stupendous ride over the last couple of months.

Myer posted $2.5 billion in total sales, of which $445.2 million were concession sales.

It is amidst a transition phase driven by new leadership. Over the last couple of years, the company has appointed new Board members.

A transition was essentially the need because of disruptions in the apparel retailing industry.

Australian apparel market has seen some consolidation after weaker players had been weeded out of the markets.

With the pandemic impact, there can be more casualty in this space, which would pave the way for established players.

Myer’s bottom line numbers did not meet street expectations after it incurred implementation costs, staff redundancies, impairments to brand names and lease right-of-use assets.

All of these items contributed to a net loss after tax of $172.4 million. In the second half, Myer stores were closed for eight weeks.

Even though stores were re-opened, there was subdued traffic in CBD stores. In line with most other retailers, it also catered online customer needs during the period.

At the peak of lockdown, there was a significant surge in online sales, but Myer continues to expect subdued foot traffic at CBD stores. Total group online sales clocked $422.5 million.

It was understood that there were market share gains, especially in beauty and homewares. Government wage subsidy allowed to lower operational costs along with rental concessions.

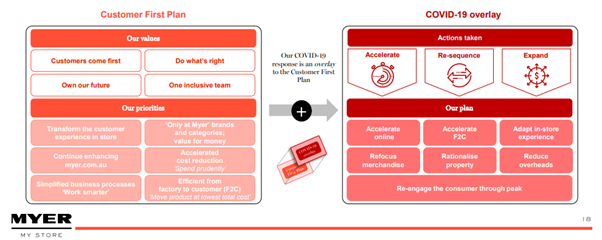

F2C strategy and re-positioning

Over the last couple of years, Myer has been telling its story: Customer First Plan. It has now revamped the plan by incorporating further long term trends into consideration.

Source: MYR Full Year Presentation. September 2020

It is quite clear that now the leadership intends to emphasise on digital capability, which could deliver long term benefits at the expense of near term investments.

Factory to the customer (F2C) will be crucial for its growth over the medium term. Myer Holdings also penned a multi-year agreement with Australia Post for warehousing and online fulfilment services.

It has also recently announced a collaboration with Amazon Hub, a parcel pick-up service which was launched in 21 stores.

Moreover, through the F2C approach, the management is looking to target a lean cost structure, with a focus on making Myer an agile business.

Similar to most retailers, it is also looking at the property and overheads – a major expense for retailers. Myer is optimising the portfolio, revising rental deals, and targeting space reduction in the future.

Liquidity & balance sheet

Although bottom-line numbers disappointed market participants, the cash flow position was better compared to previous year. It recorded a net increase in cash and cash equivalents of $39.1 million.

Trade and other payables were also lower to $354.2 million compared to $372.6 million in the previous year. Inventories were lower significantly compared to the previous year.

Inventories came down to $256 million compared to $346.9 million in the previous year, while debtors and prepayments only increased to $57.7 million from $31.2 million.

At the end of FY20, it had current borrowings of $78.6 million and current lease liabilities of $167.5 million. Although there are no non-current borrowings, Myer has around $1.63 billion in lease liabilities, which is because it is a retailer.

It has also refinanced its debt with the bankers. Now the $340 million facilities expire in August 2022. The debt includes $80 million term loan and revolving working capital facility of $260 million.

After a significant mark-down in intangible assets due to the impairment of brand names, the carrying value of intangible assets was $319.5 million compared to $467.6 million.

Out of its $319.5 million in intangible assets, the $240.2 million carrying value is attached to brand names. Should the operating conditions deteriorate over the near-term, further impairments are probable.

On 10 September 2020, MYR closed at $0.210, down by 17.65% from the previous close.