Summary

- Almost 5 per cent of eligible workers in the UK are being treated unfairly on pensions: the Resolution Foundation

- Britain’s PPF scheme for company pensions could get into trouble with rising number of firms filing for bankruptcies across the nation

- Despite stringent government regulations, the pension scammers are on the rise to encash on people’s growing fears about their future income security

A new research by the Resolution Foundation, a leading think tank in the UK, found out that close to one in twenty eligible employees are either not receiving full compensation or have not enrolled for the employer pension schemes across the nation. The total number of such employees is calculated to be 0.8 million which includes 2.9 per cent of the total permanent staff, 7.4 per cent of temporary workers, and 6.6 per cent of total part-timers in the country.

These are the same employers, who would in all probability, not be paying minimum wages, or paid holidays to their staff, thereby breaching government rules, revealed the Foundation’s findings. According to the research, such a practice is more prevalent across the industries of administration, hospitality, and personal services.

The thinktank has suggested a more proactive government enforcement to eliminate such gaps.

These figures have come out at a time when many otherwise sound companies are also going bust, as a result of the coronavirus pandemic crisis, and might not be able to meet their commitment of paying pension benefits to their employees who are registered under their pension scheme. According to the UK government’s directive, such a case calls for a rescue from the PPF.

What is PPF?

PPF or the pension protection fund is a public corporation in the UK that comes around as a safety net for any employer that becomes insolvent. It protects the defined benefit pension for employees of such insolvent companies who are unable to pay their members the promised benefits, by paying an equivalent compensation to the affected staff of such firms.

The pension incomes are at risk

According to latest estimates by LCP, an actuaries consulting firm, the government’s PPF fund is under pressure from an enormous rise in the total number of company redundancies across the UK. As a worst-case scenario, these expert estimates suggest that it could lead to a 10 per cent reduction in the pension payouts to existing pensioners, which would require a parliamentary nod for execution at the ground level. This would be a result of a more than £20 billion hit to the British pension protection fund, as per the LCP calculations.

As of now, close to 0.23 million people are already banking on the PPF for their pension payments. These include former staff of Kodak and Carillion, which collectively have a £2.3 billion shortfall in their collective pension payouts.

Steve Webb, former pensions minister suspects that such a grave scenario could eat into the entire surplus available to the PPF. He further added that such a situation could also call for a drastic rise in levies on existing employers, many of which are already facing a liquidity crunch.

In fact, there have been instances where struggling firms have been pushed into administration, where one of the compelling reasons was levies to be paid to the PPF. For instance, one such case was that of the Norville Group, whose profits got wiped out by paying PPF charges, leading to its bankruptcy.

Also Read: UK Firms Stop Pension Top Ups as Coronavirus Fears Continue

Also Read: UK Universities See Rise in Pension Deficit Due to Coronavirus-led Crisis

Retirement scams

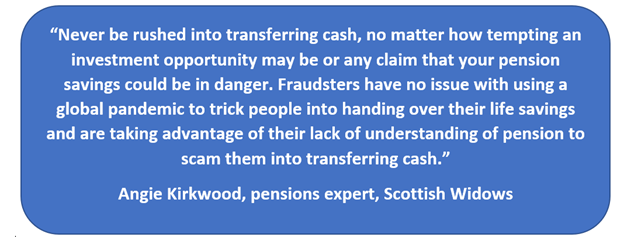

As if all this was not enough, pension savings of many simpleton Britons are also falling prey to the polished scams being rolled out by pension fraudsters.

According to government data, people have lost close to 30 million pounds to the pension scammers since the year 2017. Whether big or small, pension amounts of all sizes, as low as £1,000 and as high as £50,000, continue to being susceptible to such scams.

These fraudsters use sophisticated methods to convince people into buying their false schemes. Most of the victims have been found to be British men in their 50s.

Since the data about these pension scams is widely scattered and hard to gather, experts suggest that the actual size of the pension scam market could be much higher than what is being reported. They also feel that this fraud might have increased during the pandemic times, as the criminals got a chance to play with the tender and scared minds of naïve Britishers, who were fearful about their future income, as a result of the prevailing uncertainties surrounding the coronavirus pandemic.

Concerned over the rising pension frauds, UK government regulators have stepped in to curb the cheating practice, by implementing advanced anti-fraud practices. Government advisory has also issued warning to people suggesting that if they get a suspicious call regarding pensions savings, they should immediately call up or write to the Pensions Advisory Service to report the same and seek any clarification they might have. They can also call the government’s Action Fraud service, to report any suspected pension-related crime.

Also Read: 5 Dividend Stocks to Look at For Retirement Planning

Also Read: Some Stocks to Ponder on in The Current Market for Early Retirement

To summarise, the poor state of the British economy, largely worsened due to the prevailing coronavirus pandemic is playing havoc on the future pension income streams of the common masses. On the one hand fraudsters are rising, despite government strengthening its regulations around checking the same, because they are hard to detect since they use sophisticated technologies. On the other hand, with rising number of bankruptcies across a range of sectors in the country, the UK pension protection fund (PPF) is under pressure and this could eventually lead to a probable reduction in pension payouts to existing pensioners, which will not be a desirable scenario for sure.