Summary

- VIX is constructed to gauge the volatility in the market. It is also a proxy to check the pulse of greed and fear.

- Index was developed by Dr Robert Whaley in 1993.

- VIX holds an inverse correlation with the underlying index. The demand for put options during a downturn pushes the implied volatility for both put and call contracts higher; this happens due to the Put-Call Parity.

The volatility index or the VIX is considered by many to be a proxy to gauge the fear and greed in the market. The index was originally developed by Dr Robert Whaley in 1993, which was based on the pricing of S&P 100 (OEX) options and it originally used eight option contracts to determine a volatility measure.

On a large scale, market participants and large institutions track the Cboe Volatility Index, which utilises the options of the S&P 500 to determine the 30-day implied volatility of the market.

However, the general calculation of VIX could be applied to any major equity index to determine the 30-day implied volatility of the market, and many such VIX exists for many markets. For example, in Australia, the A-VIX, which is a real-time volatility index that tracks S&P/ASX 200 index option prices as a means of monitoring anticipated levels of near-term volatility in the domestic market.

How To Calculate VIX?

The VIX is an indicator of 30-day implied volatility determined through option prices of an underlying index, and the option price used to determine in the VIX is basically the mid-point of the option bid-ask spread of relevant at and out of the money actively traded options of an underlying index.

- In case of the Cboe VIX, the option contracts used to determine the VIX are those that trade to the next two standard contracts with at least eight days to expiry.

- When a series reaches this eight-day point, it is dropped from the calculation, and the option that expires farther in the future then start to contribute to the VIX calculation.

- All of these S&P 500 options are then used to create a synthetic at the money option that expires exactly 30 days from the very moment of calculation, and the time variable formula is constantly being updated to weight the balance of the two expiration series in the formula.

While the calculation of VIX could be troublesome for a novice trader, the understanding of its application could be useful in tackling the market better, and the right implementation of the relationship between VIX and an underlying major equity index should be the first priority to weather the storm.

VIX Holds Inverse Relationship with the Underlying Index

One direct relationship between VIX and the underlying index is that they move opposite in direction with occasional convergence, and the nitty-gritty of the relationship could be better understood in terms of VIX and the Put-Call Parity.

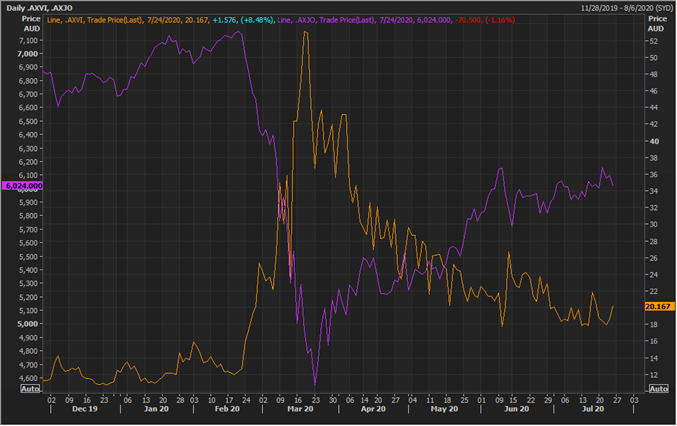

S&P/ASX 200 and S&P/ASX 200 VIX (Source: EODHD/Others Eikon Thomson Reuters)

When the market is under pressure, there is a net buying of put options, which results in higher implied volatility. The rapid demand for put options during a downturn pushes the implied volatility for both put and call contracts higher; the reason behind which is the Put-Call Parity.

What is Put-Call Parity?

Put-Call Parity states that the prices of put and call options that have the same expiration and strike price are related, and this relationship exists due to the ability to create synthetic positions in one option through combining the other option with the underlying asset.

- With this possibility, if the value of an option fluctuates enough from that of the another other, an arbitrage unfolds.

- For instance, in a zero-interest environment, a put and call price should have the same value provided that the stock is trading at the strike price, and as the options are related in price, the implied volatility of these options is also related.

So, what happens when a put-call parity breaks down and what it has to do with VIX?

Well, it is always possible to replicate the payout of a long call through combining a put option and a stock position, i.e., a long stock position along with owning a put will result in the similar payout setup as being buying a call option.

- So, if the same payout may be created in two methods, the pricing of two should be equivalent, and if they are not, the lower-priced one may be bought while the higher-priced one is simultaneously sold.

When the put-call parity gets out of line relative to each other, arbitrageurs usually take advantage of such mispricing and push markets back into line and eliminate such a riskless profit, which only includes the cost of capital and transaction costs.

The relationship between put-call parity with the VIX Index is that the VIX is based on the implied volatility of a variety of both put and call options, which falls and rises based on market forces, and this market force that impacts the implied volatility is the net buying or selling of options.

- Thus, the increase in demand is not necessarily purchasing of either all call or all put options, but just net buying of option contracts, and since, strong demand for call options will result in higher put prices and high demand for put will result in higher call prices, higher demand for either type of contract results in higher implied volatility for both put and call contracts.

Historically, VIX and the underlying index usually hold an inverse relationship, which normally relates to the type of option activity that occurs during a bullish market versus a bearish market.

As per general psychology, when the market rallies, the rush to purchase call options is not as strong, thanks to option geeks such as Alpha, Delta, and the time value of money.

- On the other hand, when the market comes under pressure, especially in very turbulent times, there is often a panic-like demand for put options, leading to increased purchasing of put options, which further results in a fast move in implied volatility.

Furthermore, general psychology says that panic is always greater than greed, which is the whole logic behind the opposite move of implied volatility against the underlying index and seldom same directional move in a market uptrend.