Europe Lowers Rate & Stimulus

Lately, on 12 September 2019, European Central Bank had declared its mammoth asset purchase program, which would see the bank buying debt at a monthly pace of 20 billion euros per month starting on 1 November 2019. In addition, the deposit rate was cut by 10 basis points to a record low of -0.5%, and measures were introduced to curb losses of the banking companies in the eurozone due to prolonged negative interest rates.

Previously, the bank had conducted a similar program to tackle the sovereign debt crisis in Europe, which was triggered after Greece defaulted on its debt. European Central Bank intends to operate in this accommodative stance until the inflation outlook reaches close to 2% or below.

Policymakers in the US had expressed concerns over the exchange rate that witnessed a sharp appreciation of USD against EUR, following the stimulus program announced by the European Central Bank.

Nevertheless, the policymakers do not weigh in, when it comes to monetary policy administration in the country. The United States Federal Reserve (Fed) will be starting its two-day monetary policy review on 17 September 2019.

Letâs look at the possible factors weighing on the policy decision of the Fed:

Short Term â Long Term Rates

The existing lower rates and the heightened uncertainty have accelerated the contraction between short term rates & long-term yields. A lower spread in the short term & long-term rates indicate less profitable business for the banks. It is believed that lower rates would encourage more spending, but that is just a demand-side rationale.

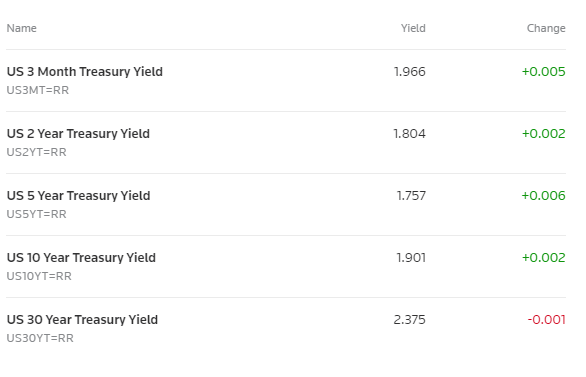

Sovereign Debt Yields (Source: Reuters)

The supply side of the monetary policy has been comparatively stronger. The lower yields, and even negative yields have been prevailing in some of the developed countries, across the globe. As a matter of fact, lower rates are the primary reason driving the yields to comparatively lower or negative territory.

Status quo in the rates has witnessed some of the US banks laying off staffs, to cut on costs in order to maintain profitability. Lowering the rate again would lead towards further fall in yields, which is not favourable for the retirees.

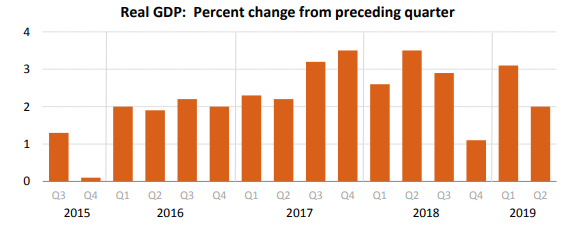

Where does the GDP stand?

According to the Bureau of Economic Analysis (U.S.), the US economy grew by 2% in the June quarter at a seasonally adjusted annual rate. The figures were lower in the second estimate by BEA, which trimmed the GDP growth to 2% from 2.1% in the advance estimate.

During the first quarter period in 2019, the economy rose up 3.1%. The second quarter GDP has witnessed improvements in the personal consumption expenditure, which grew at a rate of 4.7%, and expenditure by federal and state government was better.

Source: U.S. Bureau of Economic Analysis

Negative contributors in the second quarter were private inventory investment, exports, non-residential fixed investments and residential fixed investment. A pick up in personal consumption expenditure appears to be a good sign in a consumption-driven economy like the USA.

In the second quarter, the exports of the USA have witnessed a slump over the preceding period. Gross private domestic investments were also in negative territory in terms of per cent change from the preceding period.

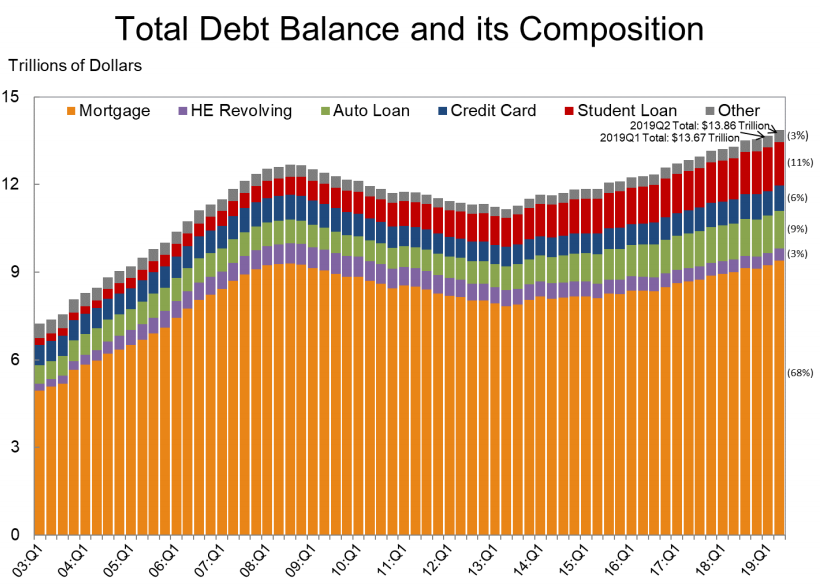

Household Debt

Debt has grown significantly; the below figure in the image form justifies that the numbers have increased from the previous peaks in nominal terms. This data is taken from Federal Reserve New Yorkâs Quarterly Report on Household Debt & Credit.

Source: Federal Reserve New York

According to Quarterly Report on Household Debt & Credit, the aggregate household debt balances increased by $192 billion in the second quarter of 2019. Mortgage balances on consumer credit reports were $162 billion higher compared to the Q1 2019, and non-housing debt balances increased by $37 billion in the second quarter.

Interestingly, the mortgage delinquency has improved, 1% mortgage balance became 90 or more days delinquent in the second quarter compared to 1.1% in the first quarter. This equates another low in the history of data.

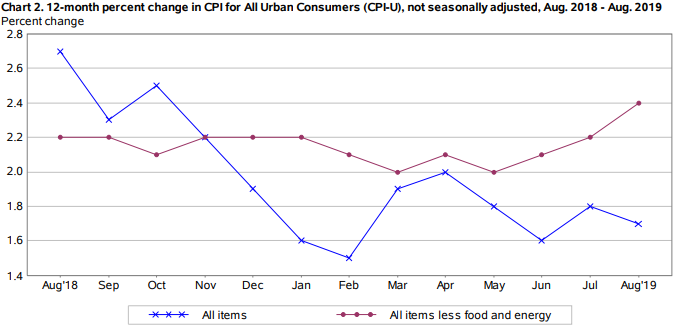

Inflation

According to Bureau of Labor Statistics, the Consumer Price Index for All Urban Consumers (CPI-U) increased by 0.1% in August (seasonally adjusted). In July, it increased by 0.3%, and over the past twelve, all items have seen an increase of 1.7% (non-seasonally adjusted).

Food inflation for the month of August was unchanged, and the index for food at home has been on a declining trend for three months in a row now. Index for fresh fruits, the index for cereals and bakery products also declined.

Source: Bureau of Labor Statistics

Energy Inflation was down 4.4% over the past twelve months, and it decreased by 1.9% in August. All of the major components in index has declined with gasoline down 3.5% in August, the electricity index was down 0.3% after rising in July, and natural gas rose by 0.1% after falling in seven preceding months.

Source: Bureau of Labor Statistics

The index for all items except energy & food increased by 0.3% in August. Medical care index rose by 0.7%, the index for hospital services rose by 1.4%, the index for prescription drugs increased by 1.6%. Recreation index rose by 0.5% in August, and index for airline fares kept on increasing.

More importantly, all items less food and energy increased 2.4% across one-year period with major indices rising.

Unemployment

According to Bureau of Labor Statistics, the unemployment rate for the August 2019 period was unchanged at 3.7% or 6 million. The number of people with long term unemployment (jobless over 27 weeks) was little changed at 1.2 million in August.

In August 2019, the total nonfarm payroll employment increased by 130k, having averaged 158k per month so far this year, this was also below the monthly average gain of 223k in 2018. The federal government had hired 28k largely due to the upcoming census.

Establishment Survey Data

According to the Bureau of Labor Statistics, health care added 24k jobs over the month with 392k jobs over the past 12 months, and financial services employment rose by 15k with 111k jobs over the year. Besides, employment in professional and business services continued to upscale with over 37k jobs in August, and monthly job gain in professional services has averaged 34k in 2019, which is below the average monthly gain of 47k in 2018.

Employment in the mining activities declined by 6k in August. Retail trade jobs have been sluggish with 80k job loss over the year. While comparing the job growth against 2019, the rate has moderated in manufacturing, transportation, construction, leisure and hospitality.

Over the past twelve months, the average hourly earnings have seen a growth of 3.2%, and in August, it increased by 11 cents to $28.11. In addition, the data was revised for the June & July figures, which is now 20k less than (combined months) as previously reported.

Conclusion

It is likely that the US Federal Reserve would cut the federal funds rate in the upcoming meeting. Considering the major underlying factors, including GDP, inflation & unemployment. In the GDP, household consumption has risen firmly in the second quarter, and growth in fixed investments, exports were subdued.

In December 2018, the Fed raised the rates by a quarter of a percentage point for the fourth time during the year, this led to a rate of maximum 2.5%. In March 2018, the federal funds rate increased by 25 bps to a maximum of 1.75 percent. Currently, the Fed funds rate is in the range of 2 to 2.25%.

Mortgage delinquency has been historically low at 1% of the mortgage balances. GDP growth engine is not firing at all cylinders, and positive contributions from gross private domestic investment and exports appear desirable.

Nevertheless, the divergence that appeared in the latest inflation numbers in the all items index and all items excluding food & energy could be a point to consider. Collectively the all items index was comparatively lower than July, and well below the 2% range.

Job gains have slowed comparatively on an average basis in some areas measured under Establishment Survey Data. Previous yearâs average monthly gains have been lower than the current monthly gains. Whether the possible rate cut would underpin the recovery in fixed investment, and exports could be debated topic.

A possible rate cut will push the yields to a lower end, which might trigger a bond market sell-off. It would be interesting to note whether the bond market sell-off might have impacts on the equity markets or not.

Uncertainties in the trading environment will again pose a substantial weight when the Fed decides on the upcoming monetary policy. Policymakers in the US have postponed the tariffs on $250 billion worth of the Chinese goods, until mid-October this year which was earlier planned to be levied by 1 October 2019.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.