Highlights

- Measures Borrowing Risk – LTV determines the risk level of a mortgage or loan.

- Impacts Loan Terms – Higher LTV ratios lead to stricter lending conditions and higher costs.

- Key Factor in Property Financing – Lenders use LTV to assess loan eligibility and interest rates.

Understanding Loan-to-Value Ratio (LTV)

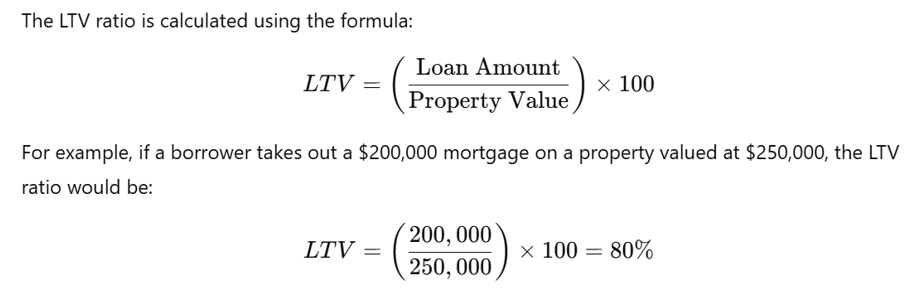

The loan-to-value (LTV) ratio is a critical financial metric used in real estate and lending to evaluate the risk associated with a mortgage or property loan. It represents the proportion of the loan amount compared to the fair market value of the property. Lenders rely on this ratio to determine the level of risk they undertake when financing a property purchase.

LTV and Its Impact on Borrowing

A lower LTV ratio indicates that the borrower has made a substantial down payment, reducing the lender's risk. In contrast, a higher LTV suggests that the borrower has less equity in the property, making the loan riskier for the lender.

Lenders generally impose stricter terms on high-LTV loans. Borrowers with an LTV above 80% may be required to pay for private mortgage insurance (PMI) to protect the lender in case of default. Additionally, higher LTV ratios often lead to increased interest rates, stricter eligibility criteria, and larger down payment requirements.

Financial institutions also use LTV to assess a borrower's ability to refinance or secure home equity loans. A lower LTV increases the chances of approval for favorable loan terms, while a high LTV can limit borrowing options.

Conclusion

The loan-to-value ratio is a fundamental tool in property financing that helps lenders assess risk and determine loan conditions. A lower LTV ratio provides better borrowing terms, while a higher LTV can lead to increased costs and additional requirements. Understanding LTV is essential for borrowers looking to secure favorable mortgage terms and manage their financial commitments effectively.