Highlights

- Australian housing credit growth is running ahead of household income growth.

- APRA has raised the minimum interest rate buffer from 1 November.

- APRA's objective is to ensure that home and mortgage lending remains prudent.

The Australian Prudential Regulation Authority (APRA) has increased the minimum interest rate buffer for banks to use while assessing the serviceability of home loans and mortgages. The rules are effective from Monday, 1 November 2021. New rules are introduced, keeping in mind the chances of housing credit growth running ahead of household income growth in Australia in the coming periods. With the economy expected to bounce back as lockdowns get lifted, strong serviceability norms shall help balance risks.

What changed for home loans and mortgages?

Under these rules, banks offering home loans and mortgages will now check whether borrowers will repay if interest rates increase.

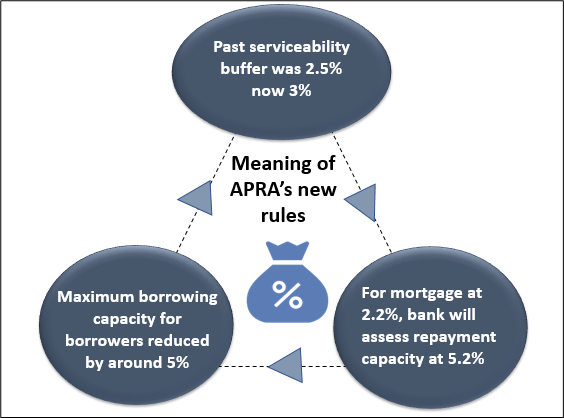

APRA has told lenders banks to assess new borrowers' ability to repay loans at an interest rate that is minimum 3 percentage points over the actual loan product rate.

A limit on the extent of high debt-to-income borrowing targets highly indebted borrowers. The increase in buffer rate applies to all new borrowers.

What is the impact on home loan borrowing?

Amongst the borrower brigade, the most impacted would be the investors than the owner-occupiers. It is because, on average, investors tend to borrow at higher levels of leverage. They may also have other existing debts on which the buffer would also be applied.

In the case of first home buyers, not many borrow at a high multiple of their income and tend to be more constrained by the size of their deposit. A 50 basis points increase in the serviceability buffer will therefore reduce maximum borrowing capacity for the typical borrower by around 5 per cent.

Given some borrowers are already constrained by the floor rates used by lenders and that many borrowers do not borrow at their maximum capacity, the overall impact on aggregate housing credit growth is expected to be reasonably modest. APRA is not seeking to target the level of housing prices. Instead, APRA's objective is to ensure that mortgage lending is prudent, and borrowers are well-equipped to service debts under various unknown scenarios.

Image showing impact of APRA’s new rules, Source: © 2021 Kalkine Media

What is the impact on mortgages?

Banks will still process borrowers waiting for their mortgage to settle under the 2.5 per cent rule. The same goes for those with pre-approval. However, they will need to buy and make a complete loan application within 90 days for some lenders.

While buyers who aren't borrowing at or near capacity are unlikely to be deterred, this new change could be the last straw for some first home buyers trying to stretch themselves to get into the market.

A new higher mortgage stress test may seem frustrating for some people; this move is designed to protect borrowers when rates undoubtedly rise.

Related Read: What to expect from RBA policy meet

What does the future home loans and mortgages hold?

The change in repayment assessment comes after a year of Australian house prices touching peaks not seen after 1989. While the banking system is well capitalised and lending standards align, increases in the share of heavily indebted borrowers and leverage in the household sector pose medium-term risks to financial stability.

In the June quarter, more than one in five new loans approved were six times more than the borrowers' income. APRA expects this scenario to continue. Although APRA has additional tools to curb lending if the situation worsens, the current change is believed to be apt. APRA thinks the move to lower borrower risk is necessary to maintain the health of the Australian economy.

An economic downturn could worsen from high house prices when people who lost jobs reduce their spending to meet increased mortgage payments. On the flip side, a fall in house prices could also cut spending. Hence being prudent and taking timely corrective actions is APRA's future strategy. APRA is also to release its framework for implementing the macro-prudential policy in the next couple of months.

Bottom line

APRA's new lending rules are targeted, judicious actions for reinforcing financial stability in Australia. However, the increase in heavily indebted borrowers and leverage in the household sector pose medium-term risks to economic stability.

Also Read - Is Evergrande bond default anxiety over?