Estate planning rarely makes the investor's reading list. The asset side gets the attention; the transfer side does not. The pattern only changes when a will is contested. The family then finds out, often years after the testator's death, that the plan does not survive contact with the law.

Investor estates carry a higher dispute risk than the median household estate. The mix of business interests, trust structures, blended-family obligations, and second-marriage assets concentrates litigation triggers in one place. Australian estate-litigation specialists like Empower Will Contest Lawyers are a Sydney-based practice focused on contesting and defending wills across New South Wales. Their casework points to a small number of patterns that repeat in investor-heavy estates. Knowing those patterns shapes how the will should be drafted.

Why Do Will Disputes Hit Investor Estates More Often?

Three structural factors concentrate dispute risk in investor estates.

The first is asset complexity. A balance sheet that includes private company shares, trust interests, self-managed super fund holdings, and offshore assets carries more valuation disputes. The family-provision conversation gets harder when the assets are hard to liquidate.

The second is the blended-family pattern. Second marriages, step-children, and adult children from prior relationships drive a meaningful share of NSW family-provision claims. The testator who treats all children equally on paper but distinguishes between biological and step-children in practice creates the exact mismatch that ends up litigated.

The third is the documentation gap. Investors often update their portfolio without updating their will. The same probate discipline applied to assets should run on the estate plan. Wills pre-dating a major business sale, divorce, or marriage land in court more often than wills updated within the past three to five years.

What Are the Main Grounds for Contesting a Will in NSW?

A short list of the recurring grounds in NSW estate-litigation practice.

- Family provision claims. Under the Succession Act 2006 (NSW), eligible persons can apply for greater provision from an estate. Spouses, de facto partners, children, and former spouses in some cases qualify as eligible persons.

- Lack of testamentary capacity. A challenge claims the testator did not understand the nature of the will or the extent of their property when signing.

- Undue influence. A claim that another person pressured the testator into a will that did not reflect their genuine intention.

- Fraud or forgery. A challenge to the authenticity of the document or the testator's signature.

- Improper execution. A will signed without the required witnesses or formalities can be challenged on procedural grounds.

- Construction disputes. Ambiguous language in a valid will can lead to a court application about how to interpret the wishes.

How Do Family Provision Claims Work for High-Asset Estates?

Family provision claims are the most common NSW will-dispute route. An eligible person applies to the Supreme Court of NSW for further provision. The court then considers whether adequate provision was made, taking into account the applicant's needs, the estate's size, the relationships involved, and the testator's reasons for the original distribution.

For high-asset estates, the court's discretion creates real uncertainty. A multi-million-dollar estate may face a claim for additional provision even when the will is otherwise valid and clearly drafted. The Australian Taxation Office's deceased estates information covers the tax-and-administration framework that runs alongside any provision claim.

The timing matters. A family provision claim must generally be filed within 12 months of the date of death, although the court can extend this in limited circumstances. Estates that close early sometimes still face late claims, which complicates administration further.

The Australian Securities and Investments Commission's Moneysmart estate-planning guidance covers the procedural framework worth reading before any application is filed.

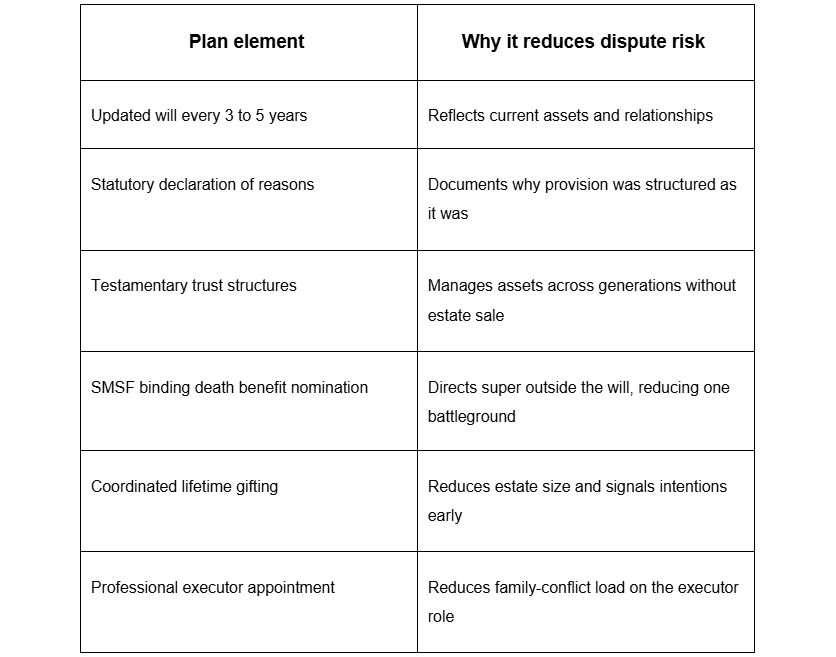

What Should Investors Build Into Their Estate Plan to Reduce Dispute Risk?

A clear estate plan addresses the dispute triggers before they arise.

Each element above is a discrete decision an investor can make during the planning phase. The cost of putting them in place is small compared to the cost of contested probate.

A Quick Estate-Planning Reality Check for NSW Investors

- Review the will after any major business sale, divorce, or new marriage

- Document the reasons for non-equal distributions, in writing

- Separate super and life-insurance from the will via binding nominations

- Use testamentary trusts for minor or vulnerable beneficiaries

- Brief the executor on the assets and the family dynamics before the event

The Investor's Bottom Line on NSW Will Disputes

Will disputes in NSW are not rare events for high-asset estates. They are a predictable function of asset complexity, family structure, and documentation gaps. Investors who treat estate planning as part of the portfolio review cycle, not a one-time legal task, almost always face fewer disputes than those who set and forget. The discipline is in updating the plan at the same cadence as the portfolio itself.

Frequently Asked Questions

How Long Does NSW Will Contest Take?

Most NSW family-provision claims take 12 to 24 months from filing to resolution. Complex high-asset matters can take longer, especially when company valuations or trust interests are in dispute. Settlement before trial is common.

Can a Will Be Made Contest-Proof in NSW?

No will is fully contest-proof under NSW law. The court retains discretion to vary provision for eligible persons. A clearly drafted will, supported by documented reasons and updated executor briefings, materially reduces the dispute risk but does not eliminate it.

Are Family Provision Claims Heard in Open Court?

Most family provision claims are filed in the Supreme Court of NSW and proceed through pre-trial mediation. Many settle before reaching open court. Hearings that do proceed are generally open to the public.

What Does It Cost to Contest a Will in NSW?

Costs vary widely. Many estate-litigation practices offer no-win, no-fee arrangements for eligible persons with strong claims. The estate typically funds the executor's defense costs in the first instance. Final cost allocation is decided by the court.

The content has been authored in collaboration with our guest contributor, Mary Jane.