The National Electricity Market (NEM) largely remained under pressure during the March 2020 quarter with average spot prices falling across all NEM regions. The decline in electricity prices was mainly led by the decrease in demand for daytime cooling and the falling gas prices due to a decline in international gas prices, lower NEM spot and contract prices amid reduced demand, and increased gas production from Queensland.

To Know More, Do Read: NEM Prices Average At Multi-year Low As Demand Dazes And Gas Price Declines in Q12020

Gas prices, especially wholesale gas prices across the continent remained under pressure for quite some time; however, the demand had a minimal impact on the decline, as it remained largely in line with the previous quarter.

As per the data from the Australian Energy Market Operator (or AEMO), the east coast gas demand across the continent stood slightly higher in the March 2020 quarter against the previous corresponding period to stand at 429 petajoules as compared to 428 petajoules.

However, as compared to the previous quarter, the demand plunged ~ 5.0 per cent, but the overall demand scenario against the previous corresponding period (or pcp) remained steady in March 2020 quarter.

The slight increase in demand against pcp was mainly due to the higher LNG exports from Curtis Island and a marginal increase in the residential, commercial, and industrial demand. However, there was a considerable decline in the demand for energy generation or GPG demand.

The total pipeline deliveries surged by 8.9 petajoules against pcp but declined by 10.1 petajoules against the previous quarter to mark the second-highest quarter on record despite a decline in international oil and gas prices.

Cargoes from Australia Pacific LNG (or APLNG) and Queensland Curtis LNG declined during the period, while cargoes from Gladstone LNG surged by five petajoules to stand at 27 petajoules during the period, leading to a total of 85 exported cargoes, reflecting higher GLNG flows to Curtis Island and lower flow to APLLNG and QCLNG.

To Know More, Do Read: Is LNG Sector Primed Against Oil Bloodbath? Santos LNG Sales Surges By 15.62 Per cent in 1QFY20

The hardest hit in the gas sector was the GPG demand, which plunged by 17 per cent during the March 2020 quarter against pcp, with fell across all NEM regions and considerably in South Australia and Victoria due to lower NEM demand in the wake of mild weather conditions during February and mid-March, leading to the lower daytime cooling requirements.

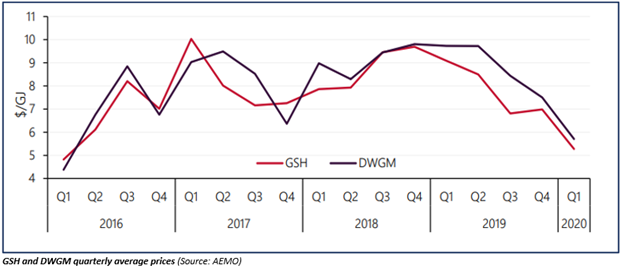

Wholesale Gas Market and Price- Trend & Present

The wholesale gas price trended further downward during the quarter with an average of 42 per cent against pcp and reached the lowest level since the first quarter of the year 2016 with largest decrease in the Brisbane Short-Term Trading Markets (or STTM), Sydney STTM, and the Gas Supply Hub of 45 per cent, 44 per cent 42 per cent, respectively.

Likewise, the price at the Declared Wholesale Gas Market and Adelaide STTM plunged by 41 per cent and 39 per cent, respectively.

GSH and DWGM quarterly average prices (Source: AEMO)

Despite a moderate increase in demand against pcp, gas prices descended further during the quarter in the wake of more gas being offered at lower prices, and as per the data from AEMO, 50 per cent of bids in the DWGM circulated near $8 per gigajoule during the March 2020 quarter, following on the decline in international oil and gas prices, lower NEM offer, and higher production in Queensland during the period.

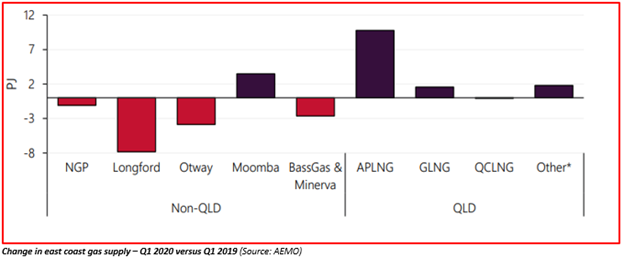

Over the supply counter, the east coast gas production increased marginally by 0.4 per cent against pcp; however, remained lower against the previous quarter, and AMEO assesses that the production from Queensland surged by 13.1 petajoules during the period against pcp, while production from Moomba surged by 3.5 petajoules; however, production from Longford decreased by 7.8 petajoules against pcp while production from Bass Gas and Minerva declined by 2.6 petajoules. ‘

The snippet of the change in March 2020 quarterly production against pcp is below:

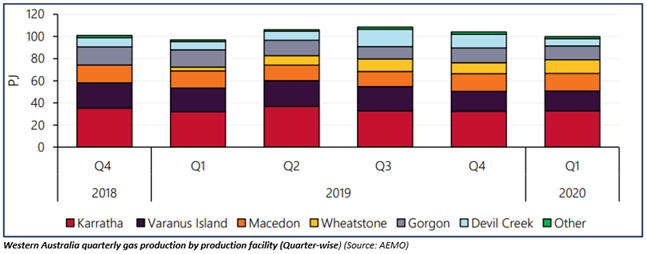

Western Australian Gas Dynamics

The gas consumption across WA stood at 91.7 petajoules during the March 2020 quarter, reflecting a 3 per cent decline against the previous quarter amid lower consumption by both Large Users, for whom, the consumption declined by 1.8 petajoules and other users, for whom, the consumption declined by 0.4 petajoules during the period against the previous quarter.

Among the large users of gas, the demand from industrial consumers tumbled by 37 per cent and form mining and mineral processing, it declined by 1 per cent and 2 per cent, respectively; however, amid its large dependency on gas for energy generation, the GPG demand across WA surged by 6 per cent during the March 2020 quarter against the previous quarter.

However, across WA the production remained in line with the demand with a total production of 100 petajoules during the March 2020 quarter, down by 4 per cent against the previous quarter.

The gas production across the region was largely hampered by the Tropical Cyclone Damien (category 3 cyclone), leading to extreme wind and rain in the Karratha and Dampier region, leading to a production shutdown in the Karratha Gas Plant and Devil Creek.

While the Karratha Gas Plant and Devil Creek remained shut due to the impact of the Tropical Cyclone Damien, the Xyris Production Facility was under maintenance and expansion during the period, leading to a further 0.2 petajoules decline in the WA production.

Devil Creek remained the largest contributor towards the fall in WA gas production with a reduction of 5.6 petajoules during the period; however, a 2.6 petajoule increase in the production from the Wheatstone indemnified the fall.