S&P/ASX200 indices closed the dayâs trading session at 6570 points (as on 18 June 2019), up by 0.6%. Letâs look at the two stocks with recent updates.

Macmahon Holdings Limited (ASX: MAH)

Macmahon Holdings Limited (ASX: MAH) is a Metals & Mining company. On 18 June 2019, MAH announced that a binding agreement had been executed to acquire GF Holdings (WA) Pty Ltd & its subsidiaries, referred as GBF Underground Mining Group (GBF).

In accordance with the series of the announcement made public today, the consideration price would comprise an upfront component depicting an enterprise value of approximately $48 million along with two earn-out based payments; however, earn-out payments would be subject to GBF achieving agreed performance in the next two financial years. Also, the payment of $48 million would be funded by cash along with the assumption of GBFâs finance lease debt. Importantly, the upfront payment represents an FY20 EV/EBITDA of 2.4x and a small premium to GBFâs net tangible asset value.

It is reported that the two earn-out payments in two financial years would be 3x the earnings above audited EBITDA target, less any increase in the net debt required to fund that earnings growth; also, the payment could be made through Macmahon shares (up to 20%), subject to overall cap at of $53.5 million (in aggregate) and partially subject to voluntary escrow.

The release read that Macmahon would have economic exposure to GBF business from 1 December 2018 under the agreement, which includes a locked-box mechanism. It also read that the completion of the agreement is subject to conditions applied for an acquisition, and a new executive service agreement with a term of at least 3 years for Mr Michael Foulds and Mr Ross Graham.

Strategic Basis

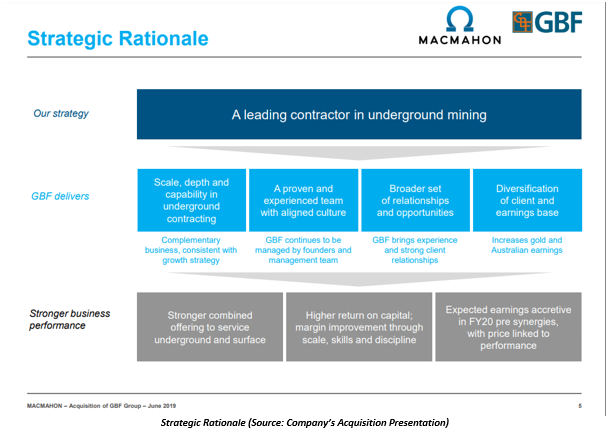

MAH believes that the acquisition is in line with the companyâs strategy to improve the capability and scale in its underground division to take advantage of the substantial level of underground opportunities visible to Macmahon Holdings along with its current & potential clients.

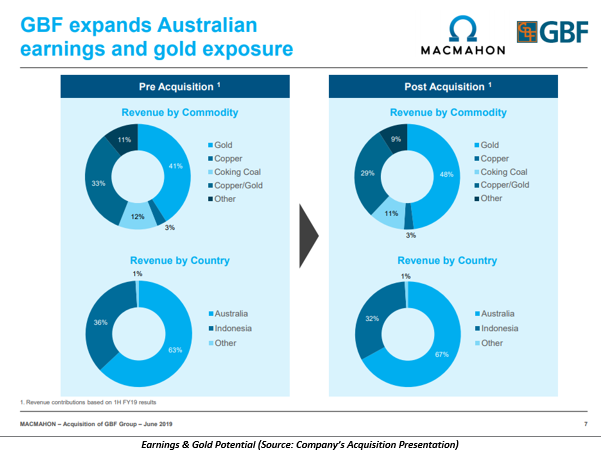

As per the announcement, the acquisition would be EPS accretive in FY20 while the existing underground mining scale, capability of Macmahon Holdings is expected to increase. Also, it would improve MAHâs capability in providing surface, underground services while increasing the client diversification and earnings from Australia. Lastly, MAH would be joined by GBFâs experienced management team with strong client relationships, and the acquisition would provide a pipeline of existing contracts and tender opportunities to MAH.

Mr Michael Finnegan, CEO of Macmahon Holdings Limited, stated that the acquisition is financially, and strategically attractive and it is also consistent with the companyâs strategy to achieve meaningful scale in the underground contracting business, in order to achieve the status of a leading mining operator, which can serve clients through the life cycle of their mining operations. He also mentioned that the acquisition would lead to growth while GBFâs key personnel, capabilities and client relationships would be integrated with MAH to maximise the ability to acquire new work.

Founded in 1988, GBF is specialist underground mining contractor with a promising track record in the goldfields of Western Australia, and it employs around 450 people. It is reported that GBF is expecting to generate FY20 revenue of ~ $180 million and EBITDA of ~$20 million.

Macmahon Holdings also forwarded the announcement by Orminex Ltd (ASX:ONX) wherein, it is reported that strategic alliance with GBF would continue after the acquisition by Macmahon Holdings and Michael Foulds and Ross Graham would be appointed to the Board of Orminex.

By the closure of the trading session, on 18 June 2019, the stock of Macmahon Holdings was at a price of A$0.195, unchanged from the previous close. Its year-to-date return stands at -9.3% while the three-month return is at -11.36%.

GDI Property Group (ASX:GDI)

Founded in 1993, GDI Property Group () operates in property and funds management. On 18 June 2019, GDI announced a fully unfranked dividend of AUD 0.03875 to be paid on 30 August 2019.

As per the release, GDI announced an estimated dividend of 3.875 cents on its fully paid ordinary stapled securities. Also, the Ex-Date for the dividend is 27 June 2019, the Record Date for the dividend is 28 June 2019 while payment date is 30 August 2019. Moreover, the dividend distribution pertains to the financial reporting/payment period ending for 30 June 2019.

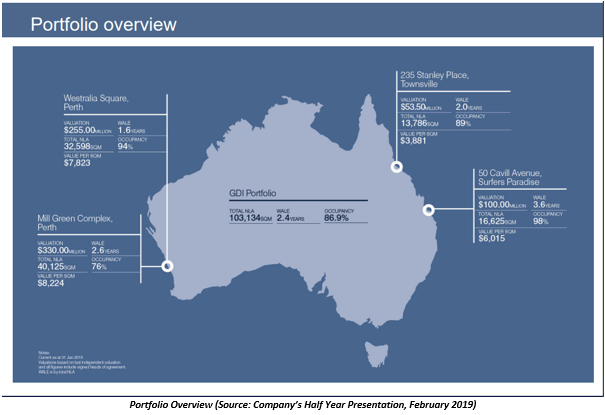

GDI is a property owner and fund manager, with a demonstrated history of strong returns to investors for over 25 years. In February 2019, the company released its half-year results for the period ended 31 December 2018. It was reported that Net Tangible Asset (NTA) per security of $1.21, up by $0.03 against the NTA on 30 June 2018.

It was reported that the property division FFO stood at ~$26.52 million in December 2018 against $23.25 million in December 2017 backed by the Westralia Square, which returned over 12% p.a. on its acquisition price with no expiries in CY19. Meanwhile, a couple of properties benefitted from high occupancy rates, and the property FFO did not include return from the assets held by GDI No. 42 Office Trust.

It was also reported that the Funds management FFO was at ~$2.57 million in December 2018 against $2.41 million in December 2017, due to higher distribution from GDI No. 42 Office Trust and greater asset under management while no meaningful transactional fees charged during the period.

As per the release, GDI extended the on-market buyback of up to 5% of its securities for a further twelve months, which had been originally announced in February 2017. Also, the strong balance sheet position allows GDI to extend the buyback. Importantly, loan to value ratio (LVR) on the Principal Facility of ~8.7% was below the Boardâs maximum LVR of 40% and the bankâs covenant of 50%, depicting a strong balance sheet position.

It was reported that under Funds Management division sold 223 ? 237 Liverpool Road, Ashfield (GDI No. 42 Office Trust) for $46.0 million, which had been purchased for $35 million in December 2015; representing an IRR in excess of 13%.

GDI asserted that the portfolio was heavily weighted to Perth along with assets, with visible capital and upside potential. The Group believes outstanding results would continue irrespective of the conservative balance sheet while the Eastern State markets weaken; GDI would capitalise on the acquisitions through the utilisation of balance sheet and investor base.

GDI chose not to provide guidance due to the groupâs constantly evolving property portfolio, funds management business and capital business along with the possibilities of asset disposals and acquisitions at GDI Property Trust and the Funds Business. Importantly, GDI confirmed the forecast of FY19 distribution of 7.75 cents per stapled security with 3.875 cents per stapled security (declared for HY 31 December 2018).

The stock of GDI Property Group last traded at A$1.435 (as on 18 June 2019), up by 0.35% from its prior close. Its year-to-date return stands at +7.52 while the past one-year return is +10.42%. The performance of the stock in the period of three months and one-month is -1.04% and +5.15%, respectively. The annual dividend of the GDIâs stapled securities is 5.42% as of today.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.