Highlights

- Definition of One-Factor APT: One-factor Arbitrage Pricing Theory (APT) is a simplified version of the general APT model, which assumes that the expected return on a risky asset is linearly dependent on a single underlying factor, such as interest rates or inflation.

- Key Concept: The model leverages diversification and arbitrage to explain asset pricing, highlighting that systematic risk can be captured using one dominant economic or financial variable affecting all securities in the market.

- Practical Implications: The One-factor APT is useful for investors and portfolio managers to estimate asset returns and make informed investment decisions by analyzing the impact of the chosen factor on the asset’s performance.

In financial economics, the pricing of assets is crucial to both investors and financial institutions. The Arbitrage Pricing Theory (APT) is a well-known model that explains how the expected return of a financial asset is determined by various risk factors. A special and simplified version of this model is the One-Factor APT, which focuses on a single dominant factor that influences asset prices. This model offers a straightforward and practical approach to asset pricing by assuming that the expected return on any risky security is linearly related to one primary market factor.

The One-Factor APT serves as an alternative to the Capital Asset Pricing Model (CAPM), offering more flexibility in factor selection while maintaining the fundamental principles of risk-return relationships in finance.

What is One-Factor APT?

The One-Factor Arbitrage Pricing Theory is a specialized form of the broader APT model, which assumes that the return on an asset is driven by a single macroeconomic or financial factor, such as interest rates, inflation, or market index performance. In contrast to the general APT, which considers multiple factors influencing asset returns, the One-Factor APT simplifies the model by focusing on just one key driver of systematic risk.

Key Assumptions of One-Factor APT:

Linear Relationship: Asset returns are linearly dependent on one primary factor.

Diversification: Investors hold diversified portfolios to minimize unsystematic risk.

No Arbitrage Opportunities: The market corrects any pricing inefficiencies, ensuring no risk-free profit can be made.

Factor Sensitivity: Each asset has a different sensitivity (beta) to the chosen factor.

The core equation representing the One-Factor APT is:

E(Ri)=Rf+βiF+ϵiE(R_i) = R_f + \beta_i F + \epsilon_iE(Ri)=Rf+βiF+ϵi

Where:

- E(Ri)E(R_i)E(Ri) = Expected return of asset iii

- RfR_fRf = Risk-free rate

- βi\beta_iβi = Sensitivity of the asset to the chosen factor

- FFF = Value of the single factor

- ϵi\epsilon_iϵi = Idiosyncratic (unsystematic) risk component

How One-Factor APT Works

The One-Factor APT assumes that market movements and asset price changes can be attributed to a single underlying force that influences all securities. This factor could be an economic variable, such as interest rates, or a financial indicator, such as the overall market return.

Step-by-Step Breakdown:

Factor Selection: Identify the most relevant factor that influences asset prices (e.g., GDP growth, inflation, or bond yields).

Determine Factor Sensitivity: Calculate the beta (sensitivity) of each asset concerning the chosen factor.

Estimate Expected Return: Using the APT formula, calculate the expected return based on the risk-free rate and factor impact.

Portfolio Diversification: Construct portfolios to reduce idiosyncratic risks, ensuring the factor drives overall portfolio performance.

For example, if interest rates are chosen as the single factor, an investor would analyze how an asset's return reacts to changes in interest rates. Assets with high sensitivity would exhibit greater volatility based on rate fluctuations.

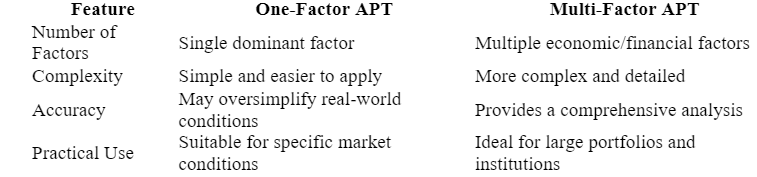

Key Differences Between One-Factor APT and Multi-Factor APT

While the general Arbitrage Pricing Theory incorporates multiple factors influencing an asset's return, the One-Factor APT narrows down the focus to a single dominant factor.

The simplicity of One-Factor APT makes it appealing for investors who wish to focus on a primary market driver without getting overwhelmed by multiple variables.

Advantages of One-Factor APT

Simplicity and Clarity:

- Since it considers only one factor, the model is easy to understand and apply compared to multi-factor models.

- Efficient Decision-Making:

- Investors can quickly assess how the chosen factor affects asset returns and adjust their portfolios accordingly.

- Reduced Data Requirements:

- Unlike complex multi-factor models, the One-Factor APT requires fewer data points, making it easier to implement with limited resources.

- Useful for Niche Investments:

- It works well in markets where a single factor is known to dominate, such as commodities driven by oil prices.

Limitations of One-Factor APT

Oversimplification of Market Dynamics:

- Financial markets are influenced by multiple factors, and relying on just one may lead to inaccurate predictions.

- Factor Selection Challenges:

- Identifying the most influential factor is subjective and can lead to incorrect assumptions.

- Limited Applicability:

- The model may not perform well in highly volatile or complex markets where multiple forces interact simultaneously.

- Potential for Mispricing:

- Ignoring secondary factors may result in asset mispricing, leading to suboptimal investment decisions.

Practical Applications of One-Factor APT

The One-Factor APT is widely used in:

Fixed-Income Securities:

- Evaluating how bond prices respond to changes in interest rates, which are often the primary risk factor in fixed-income markets.

- Equity Investment Strategies:

- Assessing stock performance in relation to a broad market index, such as the S&P 500.

- Hedging Strategies:

- Investors can hedge against risks by choosing assets with low sensitivity to the identified factor.

- Performance Attribution:

- Fund managers use the model to understand how much of a portfolio’s return can be attributed to a single market driver.

Conclusion

The One-Factor APT is a simplified yet powerful tool for understanding how a single key factor drives asset returns. By assuming a linear relationship between returns and one chosen factor, it offers an efficient way to estimate expected returns and manage risk. However, investors must recognize its limitations and ensure they choose the most relevant factor for their analysis.

Despite its simplicity, the model remains a valuable tool for portfolio managers, traders, and financial analysts who seek to balance risk and return while focusing on the most influential market driver.