US Markets: Broader indices in the United States traded in green - particularly, the S&P 500 index traded 63.04 points or 1.47 per cent higher at 4,363.50, Dow Jones Industrial Average Index surged by 466.71 points or 1.37 per cent higher at 34,469.63, and the technology benchmark index Nasdaq Composite traded higher at 14,474.80, up by 219.30 points or 1.54 per cent against the previous day close (at the time of writing – 11:45 AM ET).

US Market News: The major indices of Wall Street traded in a green zone ahead of the government's September labour market releasing this Friday. Among the gaining stocks, PepsiCo (PEP) shares grew by around 0.37% after the Company’s quarterly revenue came out to be more than the consensus estimates and raised the full-year revenue guidance. Among the declining stocks, Albertsons Companies (ACI) shares dropped by around 2.66% after BMO Capital downgraded the Company to “underperform”. Veoneer (VNE) shares went down by around 1.22% after the Company got agreed to be acquired by investment firm SSW Partners. Duckhorn Portfolio (NAPA) shares went down by around 0.55%, even after the Company provided a better-than-expected full-year earnings outlook.

UK Market News: The London markets traded in a green zone after the release of UK services PMI data. According to the recently available data from IHS Markit/CIPS, the UK services PMI stood at ~55.4 during September 2021, slightly up from the six-month low of ~55 recorded in August 2021.

Greggs shares climbed by about 10.20% after the Company’s two-year like-for-like sales grew by around 3.5% during the third quarter despite staffing and supply chain disruption. Moreover, the Company had anticipated a full-year outcome to remain ahead of the previous expectations.

How did global markets perform yesterday?

Hotel Chocolat Group shares surged by around 10.49% after the Company’s top-line revenue increased by around 21% during FY21. Moreover, the trading performance for the first 13 weeks of FY22 remained in line with the management expectations.

ScS Group had shown decent growth in top-line revenue and witnessed a favourable turnaround into profitability during FY21. Furthermore, the shares grew by around 0.38%.

FTSE 100 listed Melrose Industries shares dropped by around 1.19% after the Company had highlighted the adverse impact of supply constraints in the automotive industry.

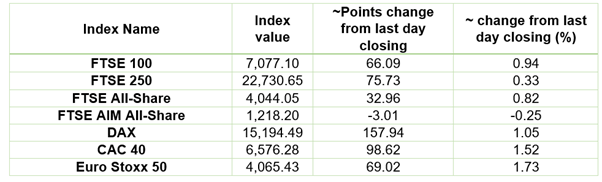

European Indices Performance (at the time of writing):

FTSE 100 Index One Year Performance (as of 05 October 2021)

1 Year FTSE 100 Chart (Source: EODHD/Others)

Top 3 sectors traded in green*: Financials (1.70%), Energy (1.66%), Consumer Cyclicals (1.03%).

Top 3 sectors traded in red*: Basic Materials (-0.53%), Consumer Non-Cyclicals (-0.17%).

Top 3 gainers on FTSE All-Share index*: Greggs PLC (10.27%), River and Mercantile Group (7.69%), Motorpoint Group PLC (6.86%).

Top 3 losers on FTSE All-Share index*: Endeavour Mining PLC (-3.85%), Elementis PLC (-3.24%), Lamprell PLC (-2.89%).

Crude Oil Future Prices*: Brent future crude oil (future) price and WTI crude oil (future) price were hovering at $82.59/barrel and $79.00/barrel, respectively.

Gold Price*: Gold price was quoting at US$ 1,762.55 per ounce, down by 0.29% against the prior day closing.

Currency Rates*: GBP to USD: 1.3639; EUR to USD: 1.1604.

Bond Yields*: US 10-Year Treasury yield: 1.522%; UK 10-Year Government Bond yield: 1.0960%.

*At the time of writing