Summary

- The continuous business performance has been reflected in several small-cap or mid-cap telco stocks with many of them faring better than the ASX200.

- amaysim, with a market capitalisation of A$213.96 million on 24 August 2020, has been giving a return of more than 100% in the last three and six months.

- The price rally has been backed by acquiring two businesses that increased its recurring customer base significantly, a part of its business strategy to boost growth.

- amaysim currently serves more than a million subscribers in Australia.

The telecommunication industry has been able to weather COVID-19 pandemic storm better than many. With limited opportunity to meet or socialise with people during the lockdown, the interaction between the populations has been mostly dependent on telecom industry, whether calls were made through online or sim. The continuous business performance has been reflected in several small-cap or mid-cap telco stocks with many of them faring better than the ASX200.

amaysim, with a market capitalisation of A$213.96 million on 24 August 2020, has been giving a return of 113% and 116.42% in the last three and six months, respectively. On 24 august 2020, AYS closed its trading session at A$0.700, down by 3.448% from its previous close.

Let’s deep dive to understand the growth behind the amaysim’s share price leap.

amaysim Australia Limited (ASX:AYS)

Launched in 2010, amaysim is operating as an asset light subscription utility provider and intends to provide the best mobile and energy plans to its customers. The Company claims to be Australia’s fourth largest mobile service provider catering to more than one million subscribers.

52-week high on 21 August

The Company recently hit its 52-week high on 21 August at A$0.750 but closed the day at A$0.725. The price rally was experienced two days after the Company announced that the Management was expecting to publish a good set of results that too as per the prior guidance.

The Company also announced that the FY2020 results that were scheduled to be released on 24 August 2020 will now be published seven days later on 31 August 2020.

Also Read: Can this ASX 200 listed company make a new 52-week high: carsales?

Acquisition of OVO subscribers

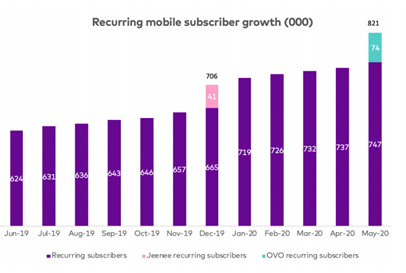

On 3 June 2020, amaysim Australia Limited communicated its intention to acquire ~77,000 mobile subscribers from OVO Mobile (or My Mobile Data Pty Ltd), a mobile virtual network operator for a consideration of A$15.8 million.

The acquisition of OVO subscribers is expected to increase the Company’s recurring mobile subscriber base significantly. More than 74,000 of OVO’s acquired subscribers are recurring and its acquisition will bring amaysim's recurring mobile subscriber base to over 820,000 and a total subscriber base of 1.17m, strengthening its position as the largest mobile virtual network operator (MVNO) in Australia.

The acquisition of OVO customers is in line with the Company’s strategy to grow its mobile subscriber base both organically and inorganically, with a prime focus on increasing annual recurring revenue.

Source: ASX Update, dated 3 June 2020

The acquisition is expected to add to the earnings in FY2021. From FY 2022, the acquisition is anticipated to contribute to the revenue growth in an increasing manner.

amaysim expects migration of subscribers to be completed within four months. The Company recently completed migration of ~41,000 Jeenee subscribers within three months, successfully.

Funding for the OVO customer Acquisition

amaysim has secured commitments through increasing its debt facility by $6 million from its banking syndicate to back the acquisition. The increase in debt facility came after a $14 million Senior Debt Facility C was increased in December 2019 that was utilised to fund the Jeenee acquisition and potential future acquisitions, maturing in March 2023.

The Company drew $7.8 million from the Facility C to fund the Jeenee acquisition, while $6.2 million remained as headroom in the debt facility C. The remaining balance coupled with $6 million from the new Facility D along with $3.6 million from amaysim's cash balance, will be used to fund $15.8 million acquisition.

EBITDA Guidance update

On 3 June 2020, the Company reiterated to close its FY2020 underlying EBITDA guidance in the range of A$33–A$39 million, as communicated earlier. The guidance is backed by an organic growth of the mobile subscriber base that has continued along with the inorganic acquisition such as Jeenee and OVO subscribers.

The performance of the energy business also had been good with energy subscribers rising to 209,000 as at 31 May 2020, versus 201,000 subscribers from 1H2020.

amaysium’s NPAT grew by 178% during H1 FY20

The Company experienced a 178% surge in NPAT during its H1 FY20 to A$3.7 million, with EPS up by 155% to 1.3 CPS, when compared to previous corresponding period (pcp). However, net revenue decreased by 7.1% to $244.4 million, with underlying EBITDA recorded at A$24.0 million, a decrease of 17.9% pcp.

amaysium recorded a 15.4% decline YoY to A$22.34 as ARPU (average revenue per subscriber) stemming from the recurring mobile subscribers base during the H1 FY20.

The decline was due to a competitive mobile environment in last two years, 2018 and 2019, with a rising trend towards plans with higher inclusions. Also, ARPU decreased to A$125.31 in energy sources mainly due to lower energy usage across the customer base.

At the end of H1 FY20, cash and cash equivalent totalled A$39.7, an increase of A$9.0 million from H2 FY19 ending 30 June 2019.

Also read: amaysim Australia’s share price: the best bet for the day with a new vision in Energy Space