Major Banks Losing the Ground: Value Still Intact

Possibly the jewels in the Australian capital marketsâ crown â major banks are now up and running in the new financial years. Best known for resilient income and stability, the major banksâ basket includes â Australia and New Zealand Banking Group Limited (ASX: ANZ), National Australia Bank Limited (ASX: NAB), Westpac Banking Corporation (ASX: WBC) and Commonwealth Bank of Australia (ASX: CBA).

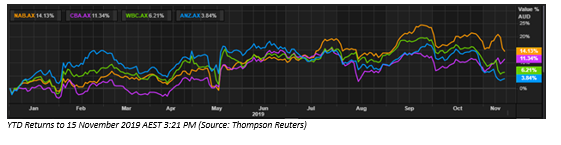

Value Proposition

At an aggregate market capitalisation of approximately $390 billion, as on 15 November 2019, the major banks also possess prowess to move the benchmark indices significantly.

Presently, the major banks are having annual dividend yields of over 5% with ANZ now yielding 6.32%, WBC yielding 6.55%, NAB yielding 5.97%, and CBA yielding 5.4%, as of 15 November 2019 (AEST 02:12 PM), according to data available at ASX.

Such opportunities provide the investors with an option to potentially lock these attractive dividend yields at the prevailing price, or increase the yield-to-cost. Moreover, buying equities at a relatively lower price than normal, allows investors to have higher dividend yield, as stock prices and annual dividend yields are inversely correlated.

Among the major banks, CBA closed the financial year 2019 on 30 June 2019, while the rest had closed the financial year 2019 on 30 September 2019.

Despite the major headwinds discussed later in this article, the major banks had done a reasonably steady job with near consistent dividends, and profit.

In FY 2019, NAB declared total dividends of 166 cents per share to shareholders and posted a statutory net profit after tax of 4,798 million.

ANZ had declared total dividends of 160 cents per share to the shareholders and delivered a statutory net profit after tax of $5,953 million.

CBA had declared total dividends of 431 cents per share to the shareholders and recorded a statutory net profit after tax of $8,360 million.

WBC had declared total dividends of 174 cents per share to the shareholders and delivered a net profit for the year of $6,790 million.

Royal Commission, Lower Rates and Sluggish Economic Growth

The Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry arrived as an inflection point for the major banks as well as for the broader financial services industry in the country.

NAB has over 950 people dedicated to customer remediation, following the findings of Royal Commission, and in FY2019, the bank incurred additional charges on $1,100 million after tax for customer related remediation.

For NAB, these charges along with an alteration in its software capitalisation policy were the major reasons for the 10.6% fall in cash earnings in FY2019 over FY2018. The bankâs provisions for customer-related remediation as at 30 September 2019 totalled $2,092 million.

More importantly, the actual final costs of such remediation would be available once all of the customer remediations are completed, stated NAB.

In FY 2019, ANZ had announced an additional charge of $682 million due to an increase in provisions for remediation work. The bank was resolving identified fee or interest discrepancies for over 3.4 million Australian retail and commercial customers and had remediated over one million accounts.

In its Q1 Update, CBA mentioned its commitment to address remediation issues impacting its customer base quickly. CBAâs $2.2 billion in program spend and provisions includes $1.2 billion for customer refunds, out of which $600 million was refunded to customers of banking and wealth management, excluding aligned advice.

In addition, the bank is also progressing with the remediation of customers from other parts of business including salaried adviser and aligned advice.

In FY 2019, WBC mentioned that cash earnings were impacted by $849 million due to higher costs associated with customer remediation and costs associated with exiting financial planning business.

The major banks have incurred significant costs and provisions, following the Royal Commission enquiry. However, it should be noted that as major banks have kept provisions, the actual cost is yet to be realised.

Record low interest rate could have an impact on net interest margins of the banks; however, it is also equally important to note that the impact to every bank is idiosyncratic, depending upon the revenue streams. In addition, the sluggish economic growth is not a good sign for banks, as economic activity falls, it could have impact on the businesses of the major banks.

In FY 2019, NAB mentioned that net interest margin decreased by 7 basis points over FY 2018, out of which 2 basis points impact was due to lower net interest income and 3 basis point decrease in lending margin was due to lower housing lending margins on the back of competition, among other reasons.

The bank also acknowledges the slowdown in the economic growth and expects it to remain below trend in 2020 and 2021. It was reported that key adverse dynamics for Australia continue to be weak growth in consumption and a decline in dwelling investment.

ANZ expects challenging trading conditions in the foreseeable future, while record low interest rates in the country and global trade tensions would continue to pressurise earnings capability of the bank.

In its Q1 update, Commonwealth Bank of Australia stated that it is well positioned in an operating environment that is challenged by factors like global macroeconomic uncertainty and historically low interest rates.

It was also reported that CBA would remain disciplined in a low interest rate environment to deliver value for its customers, and 800k retail shareholders, including many retirees relying on CBAâs dividends.

WBC mentions that the economic outlook for Australia remains challenging, and the bank expects credit growth to lift slightly in 2020 to 3% overall. It was also stated that the environment for banks remains challenging due to lower rates.

In addition, the regulators from Australia and New Zealand have several ongoing reviews related to home loan pricing, remuneration, and capital/ risk weighted asset methodologies across the sector. It expects that additional information about the reviews would arrive in the year ahead.

Stock Prices, as on 15 November 2019 (AEST 03:09 PM)

NAB was trading at $27.465, down by 1.205% relative to the previous close.

ANZ was trading at $25.385, up by 0.257% relative to the previous close.

CBA was trading at $80.570, up by 1.003% relative to the previous close.

WBC was trading at $26.575, up by 0.019% by relative to the previous close.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.