Summary

- Many of the UK’s retail firms have availed government’s stimulus support such as furlough schemes or soft loans to protect their businesses in the wake of the COVID-19 outbreak

- Recently various retail firms have started announcing dividends, even when they are considering laying off people

- One of the primary reasons why these companies may be unwilling to expedite their loan repayments is the number of tax benefits they can avail from it

The UK’s retail sector is one of the most affected industries in the wake of the coronavirus pandemic, with many small and medium-sized retail firms going into bankruptcy. Some of the companies that managed to survive the economic shock were due to the government’s furlough and stimulus soft loan scheme.

Several large and medium companies in the sector like Tesco plc, J Sainsbury plc and B&M have announced dividends in the second half of the year, despite the sector continuing to reel under the pandemic induced duress.

This has raised questions about the sincerity of the management of these companies towards their important stakeholders like employees, government and shareholders. Many of these firms are in the process of laying off employees and shutting down stores to streamline their businesses. Having extra cash in their banks under such circumstances would only give them a stronger footing.

It is also being speculated that these companies may have a deliberate strategy to go slow on repayment of the stimulus soft loans as they bring them significant tax advantages, which they would like to avail for as long as they can.

Paying dividends during difficult times

During times of economic distress like the current one, which is marred by the pandemic, the ability of the businesses to churn out revenues is severely impacted. Under such circumstances having extra cash, balances help them to stay afloat and pay for the salaries of employees and other essential expenditures.

Paying dividends under such condition amounts to putting on risk these essential expenditures and pulling down the company deeper into distress. It also defeats the very purpose of the government extending these stimulus schemes, costing billions of pounds in taxpayers' money.

Most of these companies have also laid off thousands of workers, which has raised the unemployment levels in the country. The retail sector is one of the largest employer industries in the country; there move is having a deeply damaging effect on the economy.

The retailing industry also needs a significant amount of capital investment, as it tries to transform itself to adapt to the changing business environment in the aftermath of the pandemic. By not paying dividends, the companies can fund these capital expenditures with internal accruals, which would result in a minimal rise in their overall required internal rates of return (IRR). Keeping the required IRR of a company under check is critical for its long-term growth prospects.

A smokescreen for investors

Paying dividends when a company is not doing good is traditionally seen as an attempt by the management to create a smokescreen to conceal the weakness of a company. It also helps the company to artificially jack up its stock prices when they should be going down.

These concealed weaknesses would inadvertently harm the company in the long term and result in investors capital erosion, which is more than proportionate to the value of dividends they have received.

The argument put forward by many companies that they pay regular dividends to reward investors for sticking with them through difficult times, should not be taken at its face value. When a company is paying dividends despite not making profits, it is paying it out of the company's capital base, which the shareholders of the company already own and does not represent any benefit.

The tax angles

Many market observers believe that retail companies are not paying back their loans when they have the money, and instead paying dividends, which could be a deliberate strategy to save on taxes. When a company can get soft loans, like the ones rolled out by the government during the first half of this year, it helps the companies who avail of these loans to reduce their overall cost of capital.

The interest paid by a company on the debt it owns is an allowable expenditure under income tax laws, which indirectly helps the company lower its tax liability. When a company has availed a loan when it is paying a lower rate of interest, combining it with its proportionate tax benefit, might create a possibility when its cost of debt might be lower than its cost of capital. Under such circumstances, the company would try to hold on to that debt for as long as it can. It is believed that many such possibilities have emerged in the UK in the past few months after the government stimulus packages were rolled out.

Let us see how the major retail stocks of the UK are performing-

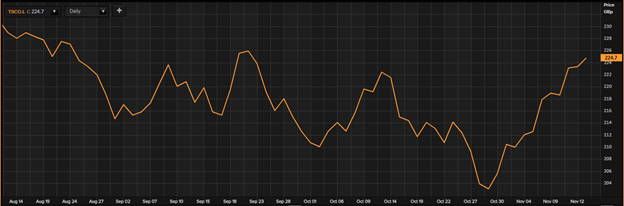

The share price movement of Tesco plc (LON:TSCO)

Three- months performance (Source- Thomson Reuters)

As on 13 November 2020, the share of Tesco plc was trading at GBX 224.70 (10.53 AM GMT+1), gaining 0.67 per cent over the previous day’s close.

The share price movement of J Sainsbury plc ( LON: SBRY)

Three- months performance (Source- Thomson Reuters)

As on 13 November 2020, the share of J Sainsbury group plc was trading at GBX 204.80 (10.52 AM GMT+1), gaining 1.09 per cent over the previous day’s close.

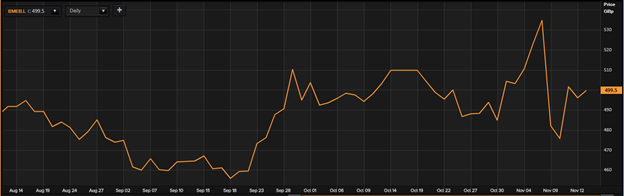

The share price movement of B&M European Value Retail SA (LON:BME)

Three- months performance (Source- Thomson Reuters)

As on 13 November 2020, the share of B&M European Value Retail SA was trading at GBX 499.30 per share (10.36 AM GMT+1), gaining 0.67 per cent over the previous day's close.