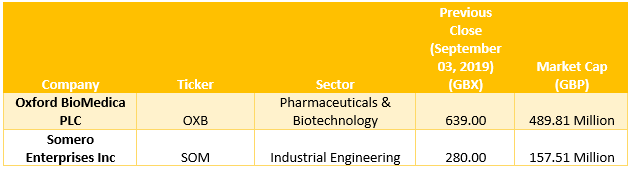

Stock Comparison of Oxford BioMedica PLC and Somero Enterprises IncÂ

(Source: Thomson Reuters)

Oxford BioMedica PLC

Oxford BioMedica PLC (OXB) is a United Kingdom (Oxford) based biopharmaceutical company. The group provides research, development and bioprocessing services of gene and cell therapy. The Group has also entered into several partnerships through which it has long-term economic interests in other potential gene and cell therapy products and has created a valuable proprietary portfolio of gene and cell therapy products in diverse areas.

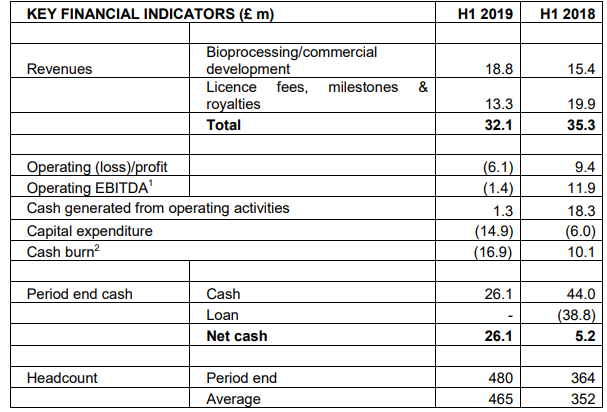

Financial Highlights (H1 FY2019, £ million)

(Source: Interim Reports, Company Website)

In H1 FY2019, the companyâs revenues stood at £32.1 million, a decrease of 9 per cent as compared with the corresponding period of the last year. This reflects the significant licence income received in the first half of the financial year 2018. However, bioprocessing/commercial development revenues surged by 23 per cent to £18.8 million against the £15.4 million in H1 FY18. Licence fees, milestone & royalties revenues reduced to £13.3 million as compared with the same period in 2018. Operating loss and an operating EBITDA loss of £6.1 million and £1.4 million against the profit of £9.4 million and £11.9 million respectively, driven by the lower revenues and increased expenditure to strengthen the companyâs strategic and operational capacity in preparation for additional volume progress in bioprocessing volumes.

In H1 2019, £11.5 million of Axovant milestone was attained with the adulterate of the 1st patient in the 2nd cohort of the AXO-Lenti-PD Parkinsonâs disease clinical trial. £53.5 million were invested by Novo Holdings A/S in the company, in lieu of 10.1 per cent of the outstanding shares after the rise in the capital. The transaction proceeds were used to wholly repay the £43.6 million of debt facility with Oaktree Capital Management.

Cash generated from operations stood at £1.3 million, a decrease from the previous year same period data, reflecting the Axovant and Sanofi licence fees received in the first half of the financial year 2018. On 30th June 2019, Cash was £26.1 million, a decline from the £32.2 million in FY18.

Its bioprocessing facility construction was progressing in tandem with the companyâs capital expenditure surging to £14.9 million in H1 FY19 as compared with the first half of 2018 of £6.0 million, the cost of which was partially offset by Innovate grant funding of £2.0 million received to support the United Kindomâs efforts to harvest viral vectors and also ensure adequate supply to services subsequent demand.

Outlook

Over the past 12 months, the company announced the new partnership, and it will continue to help to bolster revenues from commercial development and bioprocessing activities. H1 FY19 also reflects the change of another GMP suite from adherent processing to bioreactors. The Board hopes the company would have a robust second half of the financial year 2019 as expected earlier.

In the second half of 2019, the capex will continue at a high rate from the FY18 through the on-going build and fit-out of the innovative OxBox bioprocessing activities. Operating expenses will rise, due to the increase in the total number of employees to 600 in the financial year 2019.

The companyâs commercial success will depend on acceptance of gene and cell therapy by the community and the regulatory and commercial environment several years into the future. This may impact the time and cost to develop gene and cell therapy products successfully. The success of a product candidate can be impacted by the emergence of new or unexpected competitor products and technologies, or the willingness of physicians and/or healthcare systems to adopt new treatment regimes.

A material impact on the future growth of the pharmaceutical and biotechnology industries might be felt by the decision of Britain to leave the European Union, as the post-Brexit fiscal, monetary and regulatory landscape in the UK is not clear. However, the companyâs commercial pipeline remains robust, and its customer base continues to diversify, enhancing its revenue expectations.

Share Price Performance

Daily Chart as on September-04-19, before the market close (Source: Thomson Reuters)

On September 04, 2019, at the time of writing (before the market close, at 1:45 PM GMT), Oxford BioMedica PLC shares were trading at GBX 622, down by 2.66 per cent against the previous day closing price. Stock's 52 weeks High and Low are GBX 930/GBX 575.32. At the time of writing, the share was trading 33.12 per cent lower than its 52w High and 8.11 per cent higher than its 52w low. Stockâs average traded volume for 5 days was 54,952.40; 30 days â 46,780.70 and 90 days â 56,573.02. The average traded volume for 5 days was up by 17.47 per cent as compared to 30 days average traded volume. The outstanding market capitalisation was around £489.81 million.

Somero Enterprises Inc

Somero Enterprises Inc (SOM) is a manufacturer and distributor of laser-guided equipment. The group's equipment automates the method of spreading and levelling volumes of concrete for business flooring and additional horizontal surfaces, like paved parking lots in North America. The group's products comprise S-15R, STS-11M, S-485, Mini Screed C, 3-D Profiler, S-15M, S-22E, S-840, SiteShape, PowerRake 3.0, and CopperHead XD 3.0. The SXP (Somero eXtreme Platform) allows users to use their Laser Screed equipment.

Financial Highlights (H1 FY2019, US$ million)

(Source: Interim Results, Company Fillings, LSE)

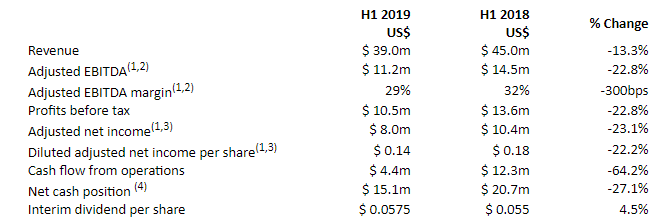

In the first half of the financial year 2019, the companyâs revenue declined by 13.3 per cent to $39 million as compared with the corresponding period of the last year, due to a decrease in North America trading driven by the extraordinarily poor weather leading to delays. Sales of the SP-16 product family surged to $1.1 million in the current period, reflecting the positive effect of the January 2019 Line Dragon® acquisition. SkyScreed® 25 contributed $ 0.2 million in the first half of the financial year 2019 revenues which is evident in the first sale of this new product. In spite of being against the effect of decreased volume and ramp-up in material costs, the gross margin remains widely in line with the previous period, at 56 per cent as compared to 57.5 per cent in H1 FY18. Partly offsetting the volume and gross margin effect, cost management efforts led to a $0.7 million reduction in operating costs against the H1 FY18. In H1 FY19, the companyâs adjusted EBITDA decreased by 22.8 per cent to $11.2 million as compared with the same period in 2018. Adjusted EBITDA margin reduced to 29 per cent against the 32 per cent in H1 FY18.

In H1 FY2019, profit before tax stood at $10.5 million, a decrease of 22.8 per cent from the previous year same period. Adjusted net income reduced by 23.1 per cent to $8 million as compared to $10.4 million in H1 FY18. Diluted adjusted net income per share was $0.14, a decrease of 22.2 per cent against the $0.18 in H1 FY18.

Cash flow from operations declined by 64.2 per cent to $4.4 million in H1 FY19 against the $12.3 million in H1 FY18. Net cash positions reduced by 27.1 per cent to $15.1 million as compared with the corresponding period of the last year. The board had declared an interim dividend per share of $0.0575, an increase of 4.5 per cent as compared to $0.055 in H1 FY18.

Outlook

In H1 FY19, the company performed in a disappointing manner in North America, driven by the extraordinary poor weather conditions. Though, the company expects to deliver full-year 2019 results widely in line with market expectations. The companyâs outlook is based on the active non-residential construction market, the anticipation that as the weather improves in the United States the clients are expected to return to more typical levels of productivity, healthy, and the high-level of confidence displayed by the clients. The company is also encouraged by the interest in the new products, which they expect will be a positive contributor in the second half of the financial year 2019.

In Europe, the company expects a solid rise in interest over the region, due to the demand for replacement equipment and technology upgrades, and also in new products. However, the company anticipates the second half of 2019 trading in the area to decrease mildly and remain below the comparable previous year period driven by the concerns across longer-term economic uncertainty in the Europe region that they believe may affect purchasing decisions by the clients. Across Europe, the company will continue to closely and carefully monitor the effect of these economic conditions on the markets.

In China, the company had decent growth in H1 FY19, reflecting the stabilising effect of local leadership of the China corporations. The long-term prospect in China hinges on the acceptance of and demand for quality by the market that has progressed at a slower pace than the initially expected. The company will continue to closely monitor the effects of US and China tariff disputes and activity in the low-end productivity segment of the market going forward.

In the Middle East and Latin America, the company expect meaningful prospects and strong performance in the second half of 2019. However, it anticipates continued uncertainty in the Middle East region and does not expect the whole recovery of the H1 FY19 shortfall before the end of the current year. In the Rest of World territories, the company looks to continue the strong H1 FY19 performance with the remainder of the current year and is also expecting the profit traction to continue in India.

Share Price Performance

Daily Chart as at September-04-19, before the market close (Source: Thomson Reuters)

On September 04, 2019, at the time of writing (before the market close, at 1:45 PM GMT), Somero Enterprises Inc shares were trading at GBX 215.10, down by 23.18 per cent against the previous day closing price. Stock's 52 weeks High was GBX 430, and it has touched a fresh 52 week low on September 4, 2019. At the time of writing, the share was trading 33.12 per cent lower than its 52w High. Stockâs average traded volume for 5 days was 15,941.20; 30 days â 40,936.80 and 90 days â 92,239.12. The average traded volume for 5 days was down by 61.06 per cent as compared to 30 days average traded volume. The companyâs stock beta was 0.23, reflecting low volatility as compared to the benchmark index. The outstanding market capitalisation was around £157.51 million, with a dividend yield of 8.38 per cent.