Summary

- There was an increase in the monthly growth rate for volume sales and value sales in August 2020 by 0.8 per cent and 0.7 per cent

- A sharp drop in total sales at minus 85.7 per cent was recorded for the textile, clothing, and footwear stores

- The Treasury Department had made an announcement in early September 2020 that the retail system allowing non-EU visitors to reclaim the VAT paid on their purchases would finish by the end of December 2020

- Removing tax-free shopping for international tourists would put 70,000 jobs in danger warn the UK retailers, hoteliers, and airport chiefs

The Office for National Statistics, United Kingdom recently released the data of retail sales of Great Britain for the month of August 2020.

As a background, the growth in the volume of retail sales was moderate up to the beginning of 2019 but flattened out throughout the year and into 2020. The total sales plunged in mid-March 2020 because the effects of the Covid-19 pandemic hit the retail stores. Many stores, especially the non-essential reduced or paused their operations. Hence, the decline continued during the whole of April 2020, but the stores began to recover from the low levels in May 2020.

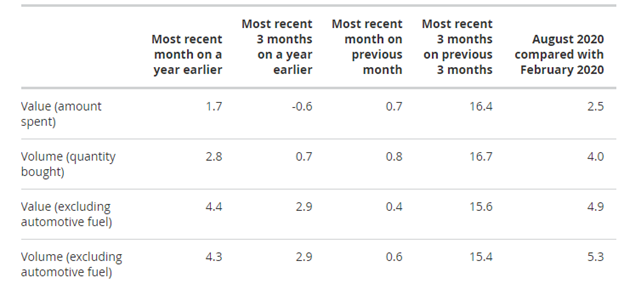

There was an increase in the monthly growth rate for volume sales and value sales in August 2020 by 0.8 per cent and 0.7 per cent respectively, as compared to the earlier month of July 2020. This was the fourth consecutive month of growth following record declines during the past months March and April 2020.

While comparing the figures for the three months to August 2020 with the previous three months, a healthy rate of growth was seen in August 2020 with 16.4 per cent in the value sales and 16.7 per cent in the total volume of sales. A sizeable monthly increase in August and July 2020 led to this trend.

Only value sales measure represented a decline of negative 0.6 per cent in the three months to August 2020 when compared with the corresponding quarter in 2019.

UK retail sales for August 2020

(Seasonally adjusted, percentage change)

(Source: Office for National Statistics, United Kingdom)

Retail sales: segment-wise

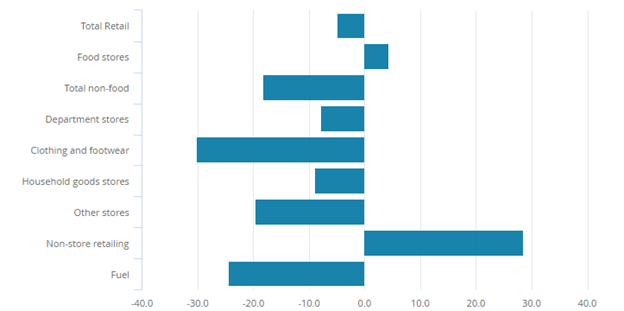

The total retail sales continued to increase in order to reach similar levels as the pre-pandemic period, with a fall of 4.8 per cent in August. 2020 Though the total sales level revived in August, a mixed picture for the different retail store types was seen, depicting that not all sectors have performed in a similar manner.

Food stores - An increase in volume sales by 4.4 per cent was seen during January to August 2020 as compared with that during January to August 2019.

Non-store retailing- Continued growth during the pandemic led to a 28.6 per cent increase in volume sales in case of non-store retailing for Jan-Aug 2020 as compared to the same period in 2019.

Fuel- Restriction in movement and shift in the work pattern, i.e., work from home led to reduction in travel. Hence, the volume sales fell by 24.3 per cent during Jan-Aug 2020 on an annual basis.

Non-food stores- Lockdown restrictions resulted in temporary store closures of many non-food retailers, with volume sales falling by 18.2 per cent for Jan - Aug 2020 on a y-o-y basis.

Clothing stores- Shift in consumer pattern towards essential food led to a strong decline of 30.1 per cent for clothing stores for Jan-Aug 2020 as compared to the same period a year ago.

Textile, clothing and footwear stores- A sharp drop in total sales at negative 85.7 per cent was recorded for the textile, clothing and footwear stores for the first eight months of 2020 on an annual basis.

Hardware, paint and glass stores- Hardware stores recovered in May 2020 with a growth rate of 58.6 per cent in comparison with April 2020. This resulted in the sales for August 2020 being 12.9 per cent higher than during February 2020.

Music stores- Though sales for this segment continued to recover in August 2020, but were still 14.3 per cent below the corresponding volume sales in February 2020.

Online Sales- The proportion of online spending was at 28.1 per cent in August, witnessing a slight fall from the 28.9 per cent reported in July. The value of online retail sales also fell in comparison with July, at negative 2.5 per cent.

Though the month of August 2020 saw declines, online sales were at significantly higher levels than the previous year.

A faster rate of recovery was seen in the furniture stores and electrical household appliances segments.

Year to date retail volume sales for Jan – Aug 2020: segment wise

(percentage)

(Source: Office for National Statistics, United Kingdom)

Withdrawal of tax-free shopping for global tourists

The Treasury Department had made an announcement in early September 2020 that the retail system allowing non-EU visitors to reclaim the VAT paid on their purchases would finish by the end of December 2020. This has led to a chaos in the retail and tourism sectors across the nation.

Removing tax-free shopping for international tourists would put 70,000 jobs in danger, warn the UK retailers, hoteliers and airport chiefs. Marks & Spencer, Selfridges and the owners of high-end designer outlet mall Bicester Village have signed a letter urging the chancellor to re-think over this policy decision as it is detrimental to the growth of the sectors.

The British economy is still recovering from the pandemic, and the retailers are continuing to face hardships, which is impacting the job market adversely. Online sales continue to dominate despite the fall, as evident from the above data. People are avoiding shopping from the high street, and if VAT duty benefit is also removed, the most likely impact could be on the brick & mortar stores, resulting in further job loss, warn the market experts.

Impact on Retail Stocks

The retail industry, which is considered to be a vital sector of the UK economy, is going through an elongated period of disruption. The ongoing pandemic, change in consumer behaviour, and increased online shopping have impacted the operations of the high street retailers.

Let us have a look at the stock performance of some of the British retail stocks.

Marks and Spenser Group PLC (LON: MKS) – is a UK retailer selling clothing, food, and home products through its website and stores. The stocks of MKS were trading at GBX 103.85 on 21 September 2020, at 12:40 PM, down by 6.23 per cent from its previous close of GBX 110.75. The 52-week low/high price was GBX 85.04/228.90. It was having a market capitalisation (Mcap) of £2,163.38 million.

Tesco PLC (LON: TSCO) – is a leading supermarket providing consumer services. The stocks of TSCO were trading at GBX 222.00 on 21 September 2020, at 12:42 PM, up by 1.09 per cent from its previous close of GBX 219.60. The 52-week low/high price was GBX 211.20/258.90. It was having a market capitalisation (Mcap) of £21,506.52 million.

Dixons Carphone PLC (LON: DC.)- is a retail company dealing in electrical and telecommunications product and services. The stocks of DC. were trading at GBX 85.75 on 21 September 2020, at 12:44 PM, down by 8.63 per cent from its previous close of GBX 93.85. The 52-week low/high price was GBX 60.00/152.45. It was having a market capitalisation (Mcap) of £1,094.72 million.