UK Market: The UK stock market was trading in the red on Thursday, with the blue-chip FTSE100 index losing over half a per cent. The index was extending losses from a day earlier, when it was reported that the UK inflation levels have hit a new 40-year high of 9.4% in June. As per the latest ONS updates, CPI surged by 0.8% in June on a monthly basis, as compared to a 0.5% hike in June last year. Rising food and fuel prices have been the major reason for the soaring inflation. Attention has also turned to the ECB and Fed with the expectation of interest rate hikes lined up.

Harbour Energy plc (LON: HBR): The shares of the greatest North Sea operator, Harbour Energy plc, were down by 4.65%, with a day’s low of GBX 333.90. The company’s biggest shareholder, EIG Asset Management, has recently distributed some of its stake to the existing investors, leading to dilution in its holding.

Dechra Pharmaceuticals plc (LON: DPH): The shares of the specialist veterinary pharma company, Dechra Pharmaceuticals plc, were down by 4.18%, with a day’s low of GBX 156.00. A sum of £184m has been raised by the company for its acquisition pipeline.

Glencore PLC (LON: GLEN): The shares of the commodity trading and mining firm, Glencore plc, were down by 2.58%, with a day’s low of GBX 415.05. The company is being investigated for bribery claims as per Cameroon's anti-corruption agency.

US Markets: The US market is likely to get a sluggish start, as indicated by the futures indices. S&P 500 future was down by 11.25 points or 0.28% at 3,956.50, while the Dow Jones 30 future was down by 0.29% or 92 points at 31,768.00. However, the technology-heavy index Nasdaq Composite future was up by 0.06% or 8 points, at 12,473.00. (At the time of writing – 8:45 AM ET).

The shares of the American telecom business, AT&T (T), slid by 1.8% in the premarket trading session. This happened even after the company beat its Q2 estimates for both top and bottom lines as it slashed its full-year guidance.

The shares of the US-based home builder, DR Horton (DHI), dropped by 1.4% in the premarket trading session. Due to moderating demand, the company slashed its annual sales guidance despite reporting higher-than-expected earnings in Q2.

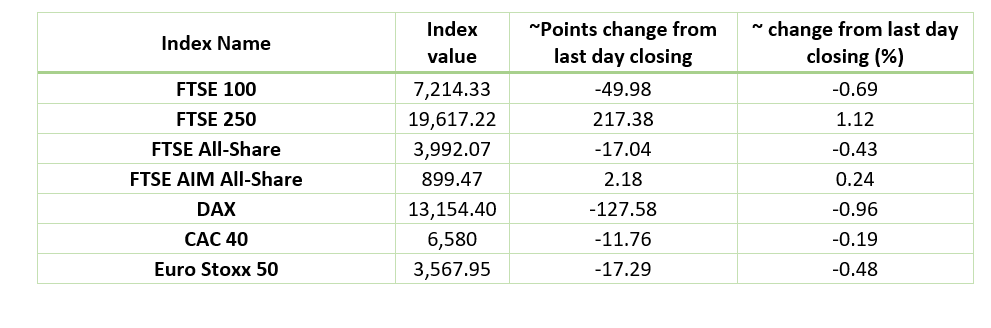

European Indices Performance (at the time of writing):

FTSE 100 Index One Year Performance (as on 21 July)

(Source: EODHD/Others)

Top 3 Volume Stocks in FTSE 100*: Lloyds Banking Group plc (LLOY), Barclays plc (BARC), Vodafone Group plc (VOD)

Top 3 sectors traded in red*: Utilities (-2.07%), Healthcare (-1.97%), Energy (-1.73%)

Top 3 sectors traded in green*: Industrials (0.59%), Consumer Cyclicals (0.58%), Technology (0.49%)

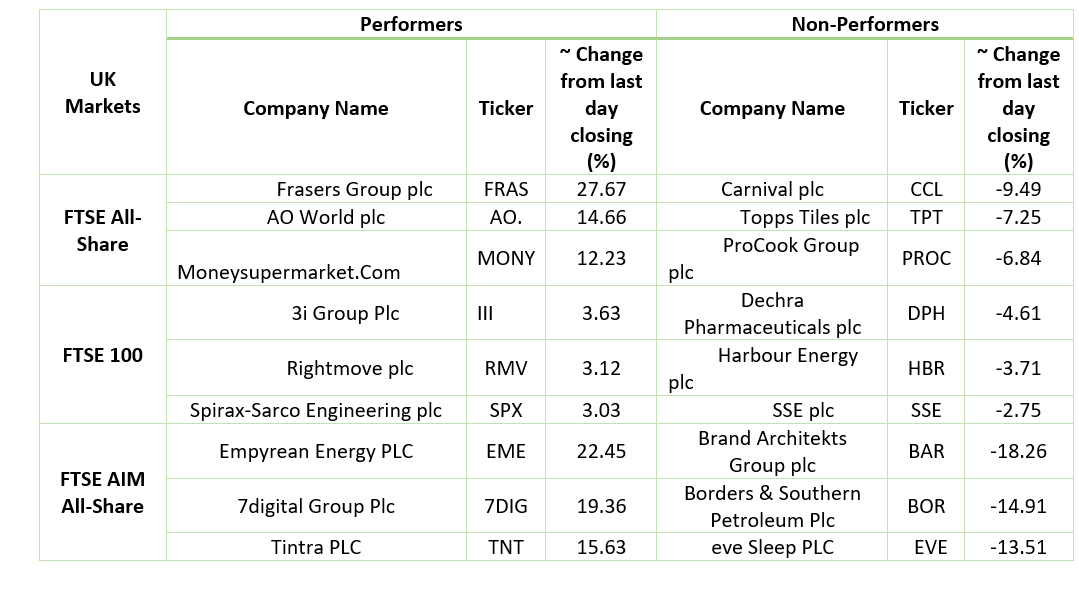

London Stock Exchange: Stocks Performance (at the time of writing):

Crude Oil Future Prices*: Brent future crude oil (future) price and WTI crude oil (future) price were hovering at $103.78/barrel and $96.47/barrel, respectively.

Gold Price*: Gold price was quoting at US$ 1,700.65 per ounce, up by 0.03% against the prior day closing.

Currency Rates*: GBP to USD: 1.1907; EUR to USD: 1.0976.

Bond Yields*: US 10-Year Treasury yield: 2.982%; UK 10-Year Government Bond yield: 2.1400%.

*At the time of writing