Global Markets*: Stocks in the United States were hovering in red in the Wednesdayâs trading session (September 18, 2019), with Dow Jones Industrial Average Index fell by 74.88 points or 0.28% to 27,035.92, the broader S&P 500 index declined 11.04 points or 0.37% to 2,994.64 and the technology benchmark index Nasdaq Composite declined by 57.44 points or 0.70% to 8,128.58, respectively.

Global News: Amid an unexpected jump in repo rates, constant pressure from President Donald Trump for steep interest rate cuts and conflicting economic data, along with political developments, the Federal Reserve will announce its results from the latest policy meeting on Wednesday. For the second time this year, a quarter of a percentage point cut is widely expected by the market, bringing target policy rate to a range of between 1.75% and 2.00%. After repeatedly asserted that Iran was behind the attack on the oil facilities of Saudi Arabia, an increase in sanctions on Iran was ordered by the President. Giving an indication that a boost to the struggling housing market was provided by lower mortgage rates, a boost to the struggling housing market showed that homebuilding surged to more than a 12-year high in August. As investors waited for the decision of Fed on interest rates, stocks edged lower at open on Wednesday, and Treasury yields fell.

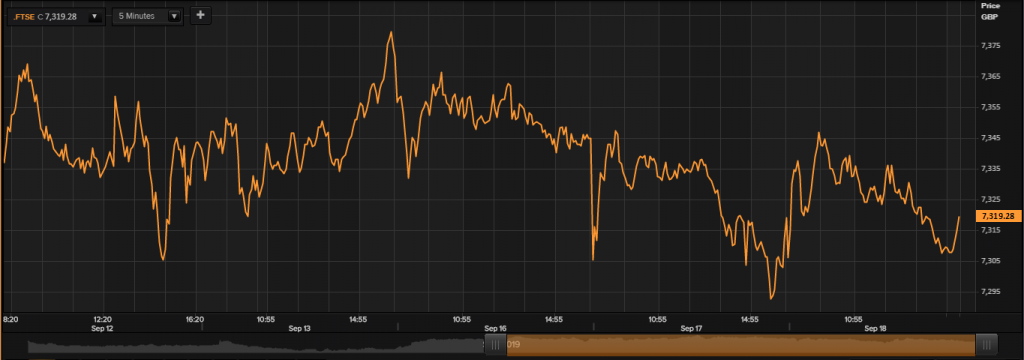

European Markets: The Londonâs broader equity benchmark index FTSE 100 traded at 6.35 points or 0.09% lower at 7,314.05, the FTSE 250 index snapped 13.89 points higher or 0.07% at 20,054.43, and the FTSE All-Share Index ended 2.46 points or 0.06% lower at 4,024.85 respectively. Another European equity benchmark index STOXX 600 ended at 389.41, up by 0.08 points or 0.02 per cent.

European News: The European Commission President Jean-Claude Juncker warned that as the contentious issue of the Irish border still unlikely to be resolved before the deadline, Britain was headed for a damaging no-deal Brexit. As government lawyers tried to persuade the British Supreme Court that the five-week shutdown was within the law, a lawyer for the prime minister said on Wednesday that the decision by the Prime Minister to prorogue the parliament is a political issue and not a matter for the court. Giving a boost to the real earnings of Britishers, the Office for National Statistics (ONS) said on Wednesday that the prices of goods and services paid by consumers increased at a yearly rate of 1.7% in August, the slowest rate since December 2016.

London Stock Exchange

Top Performers*: PETRA DIAMONDS LD (PDL), OXFORD BIOMEDICA PLC (OXB) and RDI REIT P.L.C. (RDI) are top gainers and increased by 19.48%, 6.55% and 5.34% respectively.

Worst Performers*: NOSTRUM OIL & GAS PLC (NOG), PENDRAGON PLC (PDG) and SIRIUS MINERALS PLC (SXX) are the top three laggards and decreased by 9.64%, 8.88% and 7.63% respectively.

FTSE 100 Index

Five days Price Performance (September-18-2019), before the market closed; Source: Thomson Reuters

Top Gainers*: HALMA PLC (HLMA), TUI AG (TUI) and EVRAZ PLC (EVR) are top gainers at the FTSE 100 index and climbed by 1.46%, 1.43% and 1.02% respectively.

Top Laggards*: TAYLOR WIMPEY PLC (TW.), KINGFISHER PLC (KGF) and PERSIMMON PLC (PSN) are top three laggards in todayâs session and reduced by 2.66%, 2.21% and 1.71% respectively.

Volume Leaders*: (LLOY) LLOYDS BANKING GROUP PLC; (VOD) VODAFONE GROUP PLC; (LGEN) LEGAL & GENERAL GROUP PLC.

Top Performing Sectors*: Utilities (up 0.55%), Technology (up 0.37%) and Healthcare (up 0.29%).

Worst Performing Sectors*: Telecommunications Services (down 0.40%), Consumer Cyclicals (down 0.36%) and Basic Materials (down 0.18%).

Currency Exchange Rates*: GBP/USD and EUR/GBP were quoting at 1.2471 and 0.8864.

US and UK 10-Year Bond Yields*: The US 10-year and the UK 10-year Bond yields were quoting at 1.760% and 0.646% respectively.Â

Â

*At the time of writing