Highlights:

- REA Group announces results for nine months ended 31 March 2022.

- Continued high demand for property and record take-up of premium products gave strong results.

- REA anticipates growth in Q4 based on positive residential property markets, rate hikes and low unemployment.

Property advertising business REA Group Limited (ASX:REA) announced its results for the nine months ended 31 March 2022. The group claims to have delivered strong results for Q3-FY22. It has also recorded a 23% YoY (year-on-year) revenue growth. It also anticipates growth in its residential properties business in Q4-FY22, alongside a slowdown anticipated in other lines of business.

Meanwhile, on the ASX, REA Group Limited’s share price has slumped by more than 7.81%, to trade at AU$112.47 a share early morning (10:33 AM AEST). As of date, the group stands at a market capitalisation of AU$16.11 billion, at a 52-week price range of AU$110.680 to AU$180.670.

Key financial highlights of REA Group Limited’s results

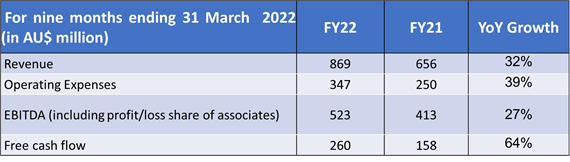

The financial information for REA Group and its subsidiaries is for a period of nine months ending 31 March 2022, of which Q3-FY22 is the latest.

Image source: © 2022 Kalkine Media ®

The group revenue from core operations for the nine months ended 31 March 2022 stood at AU$869 million, and EBITDA (earnings before interest, taxes, depreciation and amortisation) was about AU$523 million.

Talking about its latest quarter, the REA group delivered a strong result, with a 23% YoY revenue growth. It was mainly driven by the group’s Australian residential business and the inclusion of its Mortgage Choice business. The group EBITDA, including that of all associates, also remained up by 27%.

- Rental revenue benefitted from increased penetration and rising prices; however, offset by a decline in rental listings. The Commercial and developer revenue remained flat, mainly impacted by the decline in project commencements.

- REA Group’s Media, data & other revenues saw strong YoY growth, especially in data. Its financial services segment delivered strong growth in operating revenues.

- Rebranding and full integration of its Smartline brokers business to Mortgage Choice began in Q3-FY22 and remains on track for completion by Q3-FY23.

- The group’s REA India segment also delivered strong revenue growth driven by Housing.com’s property advertising business, having an audience growth of 31% YoY.

REA Group’s core operating costs were also up 6% YoY (excluding acquisitions), pushed by higher employee costs and increased marketing and revenue-related costs. REA Group’s combined share of associate profits contributed an AU$0.5 million loss to its core EBITDA, mainly because of an equity accounted loss from PropertyGuru, not recorded in the prior period.

REA’s outlook for Q4-FY22 and forward

REA group believes that the fundamentals of the residential property market remain positive. It also anticipates interest rate hikes, strong bank liquidity, low unemployment, and rising immigration to affect the Australian property market.

REA group believes that the residential listings and financial services settlements growth are likely to slow in Q4-FY22. It expects the ongoing trend of increased mortgage run-off rates to negatively impact the valuation of future trail commissions. Also, the developer project commencements are anticipated to be down on a YoY basis in Q4 due to the impact of rising construction costs.

Bottom line

While REA Group delivered a strong Q3-FY22 result, it is anticipating a slowdown in its business segments except for residential properties. The demand-supply dynamics in its businesses are influenced by various micro and macro factors. However, how far the group’s future predictions remain true will only be known with time.

More from ASX- CRN, CGF, AMC: Why These ASX 300 Shares Hit 52-Week Highs Yesterday