On 7th August 2019, one of Australiaâs leading banking group, Commonwealth Bank of Australia (ASX: CBA) revealed its full year results for FY19. During the year, the bankâs cash NPAT dropped by 4.7% to $8,492 million, mainly impacted by remediation, fee removals, risk and compliance. Alongside, the bankâs statutory profit declined 8.1% to $8,571 million.

The total operating income of the bank declined by 2% over the year, reaching to $24,407 million in FY19 from $24,914 million in FY18, mainly impacted by the decline in the net interest margin, customer fee removals and reductions as well as the impact of weather events.

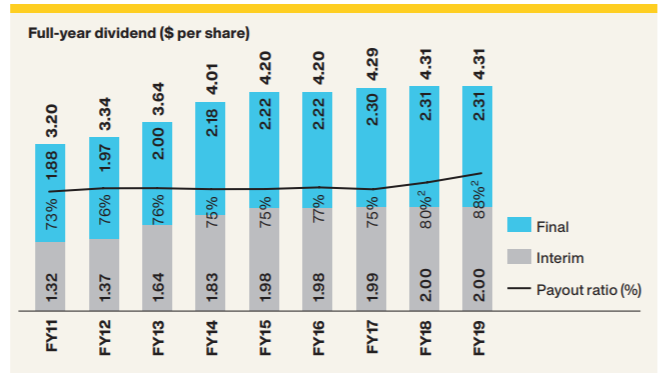

As at 30th June 2019, the bank had deposit funding ratio of 69%, the liquidity coverage ratio of 132% and a net stable funding ratio of 112%. The bank has determined a final dividend of $2.31 per share, taking the total dividend for FY19 to $4.31 per share, in line with the last yearâs total dividend.

Full Year Dividend Snapshot (Source: Company Reports)

CBA is becoming a simpler bank by focusing on its core banking businesses and simplifying its organisational structure to reduce costs and create the capacity to invest while also reducing risk and making it easier for its customers and people to get things done. To support the implementation of its strategy, CBA is investing in four critical capabilities; operational risk and compliance, cost reduction, data and analytics and innovation.

Progressing on its strategy of simplifying portfolio of businesses, the bank sold various businesses during the year, which includes Sovereign and TymeDigital. Recently, in August 2019, the bank also sold Colonial First State Global Asset Management and is now progressing to divest its other life insurance businesses â CommInsure Life in Australia and its interests in BoCommLife in China and PT Commonwealth Life in Indonesia. Reducing the complexity of its business and processes is helping to improve the customer and risk outcomes.

One of the benefits of simplification is that it allows the bank to reduce costs. While FY19 costs have been significantly higher due to remediation and risk and compliance expenses, the bank is optimistic about the benefits of business simplification.

This year, the bank removed various fees and took action on remediation to deliver better outcomes for its customers. To strengthen its leadership position in the digital space, the bank is bringing together the best technology with the best service to deliver enhanced customer experiences.

While this yearâs headline results were impacted by several reasons like customer remediation costs, compliance expenses and elevated risk, the bankâs core business performed well during the year, majorly supported by the growth in the business lending, home lending and deposits.

Although the bank is operating in a lower growth environment as mentioned by CEO, Matt Comyn while providing an outlook, CBA is expecting some relief from the improving housing market, which includes improved clearance rates, stabilisation of prices in Melbourne and Sydney, and somewhat higher housing credit growth. The bank is also relying on the support of population growth and commodity prices to drive a strong trade performance.

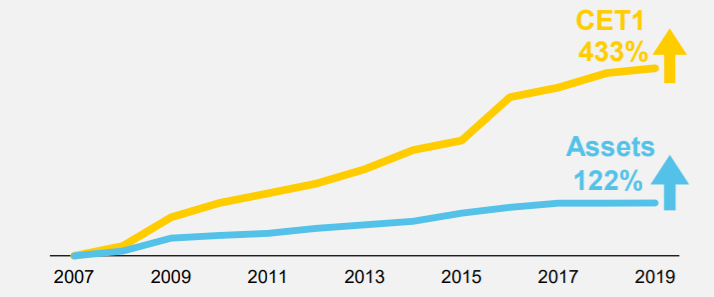

At the end of FY19, the bankâs CET1 ratio was above APRAâs âunquestionably strongâ target of 10.5%, with the CET1 ratio increasing 60 basis points to 10.7%, primarily driven by the organic capital generation of 55 basis points.

Strong Capital position maintained over time by CBA (Source: Company Reports)

In its Business & Private Banking business (B&PM), CBA reported NPAT of $2,658 million, down by 7% on pcp, impacted by home loans margins, remediation expenses and increased LIE. CBA is committed to invest in its business digital and analytics platforms, including the extension of the Customer Engagement Engine (CEE). CBA has hired more corporate bankers and created a new team of relationship managers to support its small business customers. Along with this, CBA has launched Apple Pay for Business and BizExpress to provide same day decisions on the small business loans.

In Institutional Banking and Markets (IB&M), CBA reported income of $2,444 million and NPAT of $1,071 million, both down by 8% on pcp, mainly driven by lower lending volumes and markets income as well as lower collective and individual provisions.

ASB, a bank owned by Commonwealth Bank of Australia, has reported a statutory net profit after taxation (NPAT) of $1,274 million in FY19, representing a growth of 8% on pcp. During FY19, ASBâs cash NPAT decreased by 4% on pcp and cash net interest margin decreased by 3 bps on pcp.

In February 2019, the Royal Commission released its final report, following which, CBA committed to working with government and regulators to implement the recommendations of the Final Report. Till now, out of the 76 recommendations of the Royal Commission, CBA has taken actions on 23.

The Royal Commission highlighted various shortcomings of the bank, which impacted its relationship with its customers. In 2019 Annual Report, CBA has assured that it is committed to providing exceptional service across all the channels, which its customers use to do their banking, including maintaining the largest branch network in Australia and CBAâs Australia-based call centres.

CBAâs mobile banking app was recently rated number 1 in Australia for the third year in a row by Forrester, and CBA has also been rated the best online bank for 10 years in a row by Canstar.

During FY19, CBA welcomed seven new appointments, bringing a strong mix of local and global experience across banking, risk, digital transformation, and leadership of cultural change. CBA believes that securing the best executive talent and capability is critical to the execution of the groupâs strategy. For FY2020, the bank has assured that it will monitor and adjust its remuneration policy and frameworks for all employees so that they can meet both the spirit and the requirements of revised regulatory standards and reflect evolving community expectations.

On 7th August 2019, CBA also provided an update on its aligned advice businesses, confirming that it will commence the assisted closure of Financial Wisdom Limited. Recently, CBA received approval from its shareholders for the sale of Count Financial Limited to CountPlus Limited. It is expected that the sale will be completed in October 2019, following which CBA will sell its 35.9% shareholding in CountPlus in an orderly manner subject to market conditions.

Stock Performance: In the past six months, CBAâs stock has provided a return of 9.92% as on 6th August 2019. At market close on 7th August 2019, CBAâs stock was trading a price of $78.700, down by 1.378% intraday, with a market capitalization of circa $141.27 billion. CBA has a 52 weeks high price of $83.990 and 52 weeks low price of $65.230, with an average volume of ~3,203,811. CBAâs stock has provided a YTD return of 12.44%.

One of CBAâs close peers, Australia and New Zealand Banking Group Limited (ASX: ANZ) has witnessed an increase of 1.17% in the past six months. On a year-to-date basis, the stock has provided a return of 11.99% as on 6th August 2019. At market close on 7th August 2019, the stock was trading at a price of $26.930, with a market capitalization of circa $75.74 billion.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.