Media & Entertainment Industry is currently in a transition phase, wherein it is witnessing a decline in the print media advertising and a rise in digital advertising. In the light of this scenario, letâs take a quick look at three 3 Media & Entertainment Stocks currently trading on ASX.

Nine Entertainment Co. Holdings Limited (ASX:NEC)

A media and entertainment company, Nine Entertainment Co. Holdings Limited (ASX: NEC) has now completed the sale of Australian Community Media & Printing business (ACM), a move which is in line with the companyâs strategy to exit non-core businesses and focus on Nineâs portfolio of high-growth, digital assets. In an announcement made on 1st July 2019, the company has informed that the completion of the sale on 30th June 2019, is consistent with the companyâs expectations.

NECâs stock was up 3.573% during the intraday session on 1st July 2019 (AEST 3:30 PM).

The sale was initially announced on 30th April 2019, wherein the companyâs Chief Executive Officer, Hugh Marks advised that the company will retain a commercial relationship with ACM and is looking forward to work in the areas, where both parties can reap the benefits.

The consideration for the sale was valued at $115 million, from which, the company has already received cash proceeds of $105 million (subject to the usual post-completion adjustments to be made in the coming months) and will receive further $10 million in 12 months. It is expected that the proceeds received from the sale will be utilised to decrease the companyâs indebtedness.

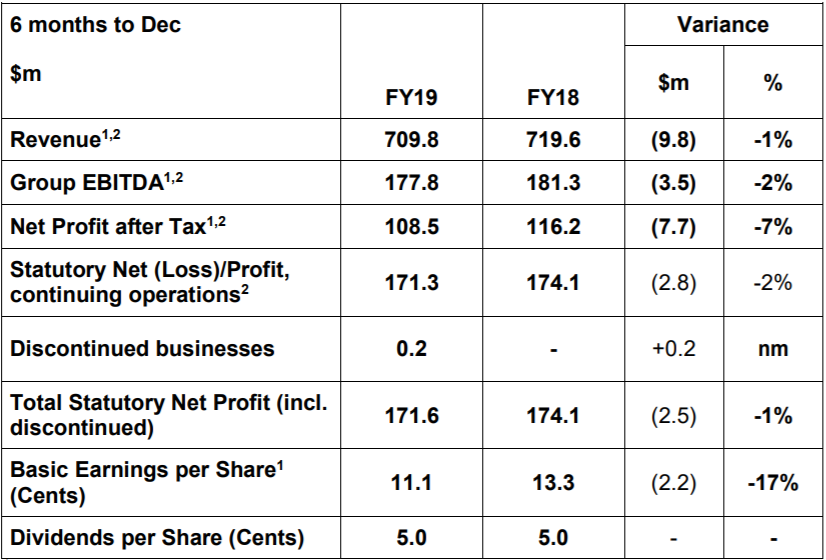

For the first half of FY19, the companyâs Net Profit After Tax amounted to $172 million, which was slightly lower (1%) than the previous corresponding period (pcp). On a pro forma basis, the company earned a revenue of $709.8 million and group EBITDA of $177.8 million.

Group Results on a Pro Forma basis (Source: Company Reports)

Group Results on a Pro Forma basis (Source: Company Reports)

In Broadcasting division, the company reported EBITDA of $177 million in H1 FY19, which was 6% lower than pcp. Further, the company reported revenues of $632 million. The companyâs Digital & Publishing segment posted revenues of $328 million, with a combined EBITDA of $60 million. The groupâs cash flow generated from operations for half year period was $81.44 million. As at 31st December 2018, the company recorded current assets of $1,297.6 million and current liabilities of $727.16 million.

In the month of December 2018, the company was merged with Fairfax by acquiring all of the outstanding shares in Fairfax and post-merger, the company now has four key pillars: Broadcasting, Digital & Publishing, Stan and Domain. In FY19, the company expects to earn Pro Forma Group EBITDA of around $420 million, representing a growth of around 10% on the FY18 like-basis results of $385 million.

On the stock performance front, the companyâs stock has been performing strongly, rising by 33.93% in the last six months and by 11.61% in the last three months. The stock is trading at a PE multiple of 8.710x, with an annual dividend yield of 5.33%. At the time of writing i.e., 1 July 2019 (AEST 03:45) NECâs stock was trading at a price of $1.942, with a market capitalisation of circa $3.2 billion.

Southern Cross Media Group Limited (ASX:SXL)

Australiaâs leading entertainment company, Southern Cross Media Group Limited (ASX: SXL) provides media solutions to Australian multimedia brands. The companyâs strategy has four key pillars: Content, Distribution, Monetisation and New Growth.

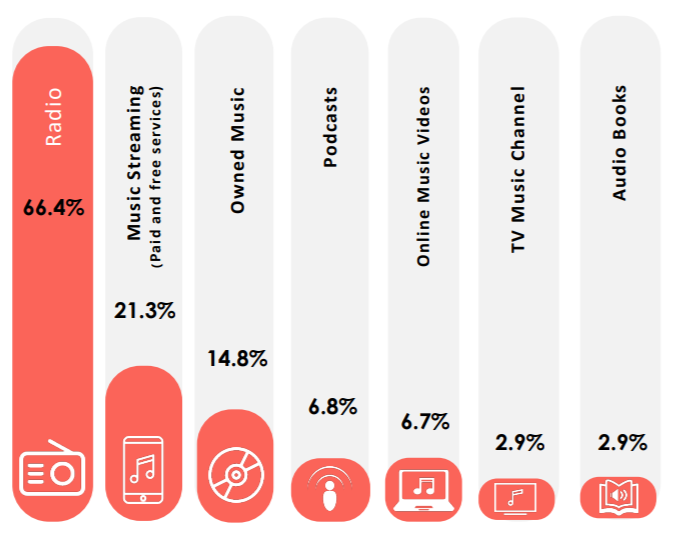

In a presentation released on 30th April 2019, the company provided information about the industry trends. As per which, 66% of all Daily audio LISTENING radio has 3 times more listeners than the streaming services combined, as depicted in the figure below.

Industry Trends (Source: Company Reports)

Industry Trends (Source: Company Reports)

While streaming music is growing, it still represents a much smaller proportion of LISTENING than radio. Radio has over 78% of all âCommercialâ Audio Listening, well ahead of the 7.8% of Ad Supported streaming. Podcasting has a 6.4% share and about 68% of the streaming music today is paid and Ad-Free subscription services. Radio audience growth is supported by population increases, portability of radio (home, car, work, mobile) and is underpinned by targeted investments in local content. The companyâs national investment regional radio markets have grown 12% and 14%, respectively over the last two years.

In an announcement made on 17th June 2019, the company announced that its Chairman, Peter Bush, is taking a leave of absence to assist in his recovery following recent hospital treatment. It is expected that he will be on leave of absence for around two months and in his absence the companyâs Deputy Chairman, Leon Pasternak, is acting as a Chairman in accordance with the Board Charter.

In the first half of FY19, the company reported a growth of 6.7% in metro radio revenue and strong cost control, which resulted in EBITDA of $82.0 million, up 2.5% on pcp.

In the half year period, the companyâs Underlying EBITDA increased 6.1% to $82.9 million and underlying NPAT increased 10.6% to $42.2 million. The group revenues were up 0.2% at $335.7 million in H1 FY19. Due to revenue growth and lower expenses, the group EBITDA margins improved from 23.9% to 24.4% in H1 FY19.

The companyâs audio segment delivered 3.8% growth in revenue and 7.3% growth in EBITDA in H1 FY19 as compared to pcp. The companyâs metro radio revenue increased by 6.7% to $123.6 million while its regional radio revenues increased by 0.7% in the half year period. The companyâs television revenue was down $8.0 million or 7.1% to $104 million. For the half year period, the company declared a fully franked dividend of 3.75 cents per share.

On the stock performance front, the companyâs stock has been performing strongly, rose 25.00% in the last six months and 10.13% in the last three months. At the time of writing, i.e. on 1st July 2019 (AEST 3:45 PM) SXLâs stock was trading at a price of $1.277, up 2.16% during the intraday trade, with a market capitalisation of circa $961.27 million.

Seven West Media Limited (ASX:SWM)

Australiaâs leading integrated media company, Seven West Media Limited (ASX: SWM) recently advised that it is expecting its FY19 underlying Group EBIT to be in between $210 million to $220 million while its FY19 group net cost reduction will be at the top end of the $30 million to $40 million range. Further, the company has assured that it will reduce its net debt by around $75 million in FY19.

The companyâs strategy is built on three pillars: First, a focus on the core, meaning that the company is focused on improving its ratings and revenue performance while growing returns on its content investment. Second, the ongoing transformation of its operating model, under which, the company is focusing on driving efficiencies, delivering cost savings and improving profitability. And third, growing new revenue streams, which is self-explanatory.

In the year 2018, the company not only had the highest commercial share of viewership in history, but also led all the key demographics with its highest ever shares of each. Channel 7 was the numero uno among all and 7mate was the number one multichannel.

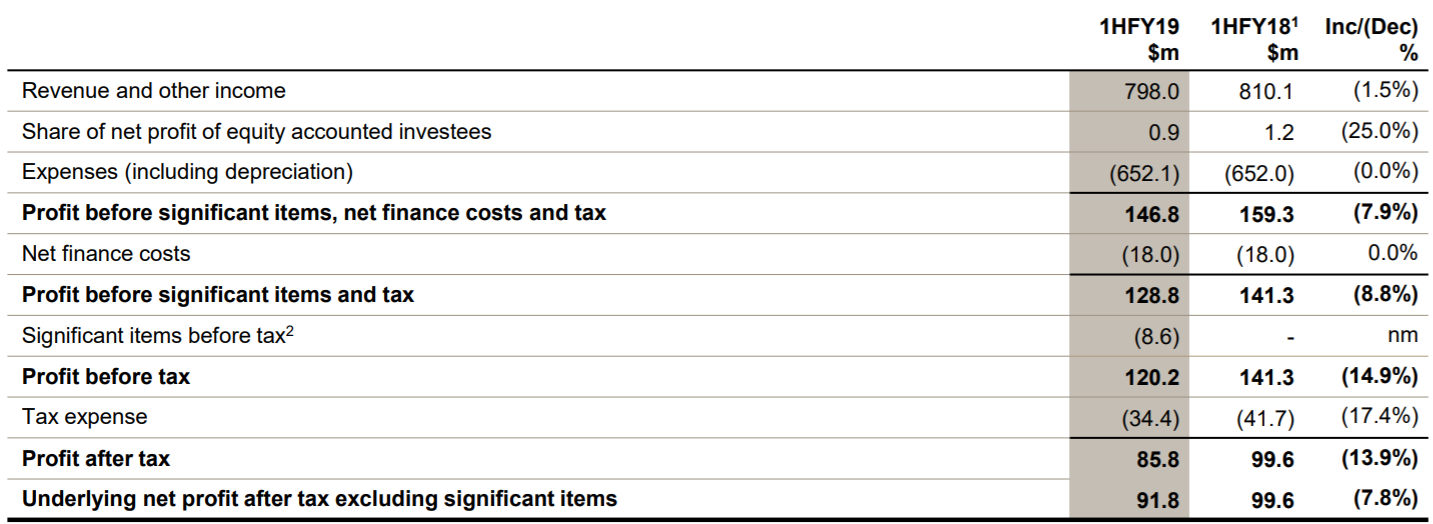

In the first half of FY19, the company delivered significantly better performance as compared to the pcp. The companyâs underlying EBIT for the half year period was $147 million while its underlying net profit after tax was $91.8 million. In October, the company refinanced its remaining debt through to 2021/22, with no change in covenants and a beneficial price outcome.

The company reported total group revenues and other income of $798 million, which was down just 1.5% on pcp. The group operating costs were flat at $652.1 million with its full year savings skewed towards the second half. The group delivered EBIT of $146.8 million, a decline of 7.9% on pcp. The prior period included a 27th week, with an average weekly EBIT of $6 million. Therefore, on a like-for-like basis, EBIT is down 4%.

Income Statement (Source: Company Reports)

Income Statement (Source: Company Reports)

The company reported a statutory profit after tax of $85.8 million, a 13.9% decrease on the prior year results. The companyâs basic earnings per share for the half year period was 5.7 cents and 6.1 cents per share, excluding significant items. For the half year period, the company recorded operating cash flow of $84.8 million. At the end of half year period, the company had net debt of $589 million.

On the stock performance front, the companyâs stock declined 15.60% in the last six months and by 7.07% in the last three months. The stock is trading at a PE multiple of 5.890x. At the time of writing, i.e. on 1st July 2019 (AEST 03:50 PM) SWMâS stock was trading at a price of $0.455, down 2.151% during the dayâs trade, with a market capitalisation of circa $701.24 million.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.