Highlights:

- Definition of Open-Market Rates: Open-market rates refer to interest rates that are established through the natural forces of supply and demand in the financial market, rather than being directly set by central authorities such as the Federal Reserve.

- Market Influences: These rates fluctuate based on various factors, including economic conditions, investor sentiment, inflation expectations, and the overall availability of credit and liquidity in the market.

- Impact on Economy: Open-market rates influence borrowing and lending decisions, affecting consumer spending, business investments, and economic growth by determining the cost of credit in the economy.

Interest rates play a critical role in shaping economic activities by influencing borrowing, spending, and investment decisions. Among the various types of interest rates that exist, open-market rates are particularly important as they are determined by the natural interaction of market forces. Unlike benchmark rates set by central banks, open-market rates fluctuate based on the principles of supply and demand in financial markets.

In this article, we will explore the concept of open-market rates, how they are determined, the factors influencing their movement, their impact on the economy, and how they compare to other interest rate mechanisms.

What Are Open-Market Rates?

Open-market rates refer to interest rates that are determined organically by market participants—such as banks, investors, and corporations—based on the supply and demand for money and credit. These rates are not directly set by monetary authorities like the Federal Reserve or other central banks, although central bank policies can indirectly influence them.

The open market, consisting of banks, financial institutions, and private investors, constantly assesses risk, economic conditions, and future expectations to determine appropriate interest rates for borrowing and lending activities. As a result, open-market rates fluctuate frequently in response to changes in the economy.

For example, if there is high demand for credit in the market, interest rates may rise due to increased competition among borrowers. Conversely, if there is an oversupply of available funds and fewer borrowers, interest rates tend to decrease.

How Open-Market Rates Are Determined

The determination of open-market rates is primarily driven by the principles of supply and demand within the financial markets. Several key factors contribute to the setting of these rates, including:

Supply of Credit:

- When financial institutions and investors have an excess of funds available for lending, interest rates tend to decrease as they compete to attract borrowers. A higher supply of credit leads to lower borrowing costs.

- Demand for Credit:

- Increased borrowing from businesses, consumers, and governments can drive interest rates higher, as lenders adjust rates to manage the rising demand for funds.

- Inflation Expectations:

- Market participants consider inflation trends when setting interest rates. If inflation is expected to rise, lenders demand higher interest rates to maintain their purchasing power. Conversely, low inflation expectations can result in lower interest rates.

- Economic Conditions:

- A growing economy with high consumer and business activity often results in increased demand for credit, pushing interest rates higher. In contrast, during periods of economic downturns, rates tend to fall due to weaker demand for loans.

- Central Bank Policies:

- Although open-market rates are not directly set by central banks, monetary policies, such as open-market operations (buying or selling government securities), can influence the supply of money in the system, indirectly affecting market interest rates.

- Investor Sentiment:

- The overall confidence of investors in the financial system, geopolitical stability, and market risks also impact interest rates as lenders adjust rates based on perceived levels of risk and uncertainty.

Impact of Open-Market Rates on the Economy

Open-market rates have a profound impact on various aspects of the economy, affecting everything from individual consumers to large corporations. Some of the major ways in which these rates influence economic activity include:

- Borrowing and Lending Costs

The fluctuation of open-market rates directly affects the cost of borrowing for consumers and businesses. Lower rates encourage borrowing for home purchases, business expansions, and investments, while higher rates can slow borrowing activity, impacting economic growth.

- Consumer Spending

Interest rates influence consumer behavior, particularly when it comes to purchasing big-ticket items such as homes, cars, and appliances. Lower open-market rates often stimulate spending, whereas higher rates may deter consumers from taking on new debt.

- Business Investments

For businesses, the cost of financing operations and capital projects is closely tied to interest rates. Lower rates encourage companies to expand operations, invest in new technologies, and hire more employees. Higher rates, however, can result in reduced investments and slower economic growth.

- Inflation Control

Open-market rates play a crucial role in controlling inflation. Higher rates can help slow down excessive economic growth and inflation by making borrowing more expensive, while lower rates can stimulate demand and economic activity during deflationary periods.

- Exchange Rates and International Trade

Interest rates in the open market can impact the value of a country's currency. Higher interest rates generally attract foreign investment, strengthening the currency, while lower rates may weaken the currency, making exports more competitive.

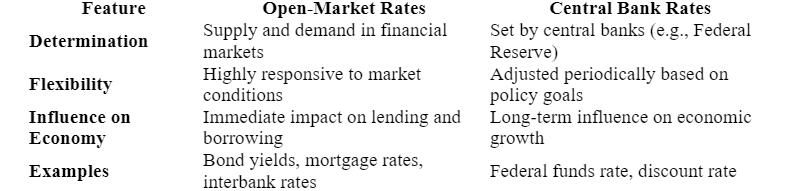

Open-Market Rates vs. Central Bank Rates

While open-market rates are determined by market forces, central banks set benchmark interest rates to guide overall monetary policy. Understanding the differences between these two types of rates is essential for evaluating their respective influences on the economy.

Central bank rates serve as a guideline for the economy, while open-market rates provide real-time insights into financial market conditions.

Advantages and Disadvantages of Open-Market Rates

Advantages:

- Market Efficiency: Rates are set based on real-time supply and demand conditions, ensuring fair pricing of credit.

- Flexibility: Open-market rates adjust quickly to changing economic conditions, making them a reliable indicator of financial market health.

- Encourages Competition: A market-driven approach fosters competition among lenders, potentially leading to better terms for borrowers.

Disadvantages:

- Volatility: Open-market rates can be highly volatile, fluctuating due to economic uncertainties and investor sentiment.

- Influence of Speculation: Speculative trading and market manipulation can impact rates, creating artificial pricing distortions.

- Dependence on Economic Factors: Rates are influenced by external economic factors that may be unpredictable, such as global financial crises or sudden policy changes.

Conclusion

Open-market rates are an essential component of the financial system, providing a transparent and dynamic mechanism for determining interest rates based on market conditions. Unlike fixed rates set by central banks, open-market rates fluctuate in response to economic trends, investor behavior, and monetary policy actions.

Understanding the role of open-market rates helps individuals, businesses, and policymakers make informed financial decisions, adapt to changing market conditions, and navigate the complexities of borrowing and investing in a constantly evolving economy.