Source: Picture industry, Shutterstock

Summary

- Bodycote PLC had registered a decline of 16.9% in revenue during FY20.

- BOY had a robust free cash flow of £106.1 million during FY20.

- Return on Capital Employed stood at 9.8% during FY20.

- BOY will pay the final FY20 dividend of 13.4 pence per share on 04 June 2021.

Bodycote PLC (LON:BOY) is the LSE listed industrial stock. BOY’s shares have generated a return of approximately 48.09% in the last 12 months. It is listed on the FTSE 250 Index. BOY was incorporated in 1953.

Business Model

Bodycote Plc is the FTSE 250 listed Company, which is the world's leading provider of heat treatment and specialist thermal processing services. Moreover, Bodycote operates across two major business division – ADE (aerospace, defence, & energy) and AGI (automotive & general industrial). Overall, BOY had 165 facilities around the globe across both business segments.

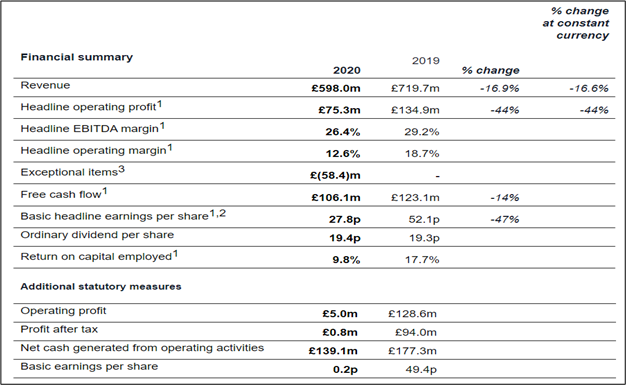

Financial Highlights (for twelve months ended 31 December 2020, as of 12 March 2021)

(Source: Company result)

- The revenues dropped by 16.9% from £719.7 million during FY19 to £598.0 million during FY20 with a heavy drop in revenue during Q2 FY20, which was even worse than the lowest points touched during the global financial crisis during 2008 and 2009. However, the acquisition of Ellison had benefitted the revenue of BOY during the year.

- BOY had reported a headline EBITDA margin of 26.4% during FY20, which remained 280 basis points lower than the levels achieved during FY19. Nevertheless, it was higher than the FY16 and FY17 levels.

- The basic headline earnings per share remained at 27.8 pence per share during FY20.

- BOY had a robust free cash flow of £106.1 million during FY20. The free cash flow conversion remained strong at around 141% during the year. Moreover, it had generated a net operating cash inflow of £139.1 million during FY20.

- BOY had declared a final dividend of 13.4 pence per share, taking the total FY20 dividend to 19.4 pence per share. The interim dividend was paid on 12 February 2021, and the final dividend will be paid on 04 June 2021.

- Moreover, the return on capital employed had declined to 9.8% due to lower profitability achieved during the period.

Divisional review

ADE Business - BOY had reported a 17% decline in revenue to £249.2 million during the period. Moreover, it was benefitted from the acquisition of Ellison. The full-year FY20 revenue decline was 25% on an organic basis. Also, the return on capital employed remained at 10.3% for the period.

AGI Business– The revenue went down by 16% to £348.8 million during FY20. Similarly, the headline operating profit and the headline operating margin was also reduced to £41.0 million and 11.8%, respectively, during the period. The return on capital employed was reduced to 8.8% during FY20.

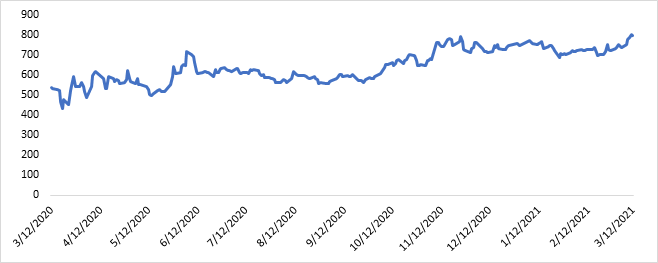

Share Price Performance Analysis of Bodycote PLC

(Source: EODHD/Others, chart created by Kalkine group)

BOY’s shares were trading at GBX 796.00 and were down by close to 0.75% against the previous closing price as of 12 March 2021 (before the market close at 09:55 AM GMT). BOY's 52-week Low and High were GBX 378.40 and GBX 802.50, respectively. Bodycote PLC had a market capitalization of around £1.54 billion.

Business Outlook

The Company had managed to produce resilient financial performance during FY20 despite facing several operational challenges. Moreover, BOY remained cautious regarding the recovery in the civil aerospace market as the duration of Covid-19 cannot be determined. Nevertheless, BOY had completed various restructuring activities during the year to achieve more effective results aligned with the strategic growth opportunities. Moreover, the Company is well-positioned to accelerate its progress on the growth trajectory and grab upcoming market opportunities. The expansion in eastern Europe would strengthen the electric vehicle supply chains. Overall, the Company is focused on repositioning to capitalize on lucrative market opportunities.