The United Kingdom, in the month of February 2020, faced various challenges, spanning from the aftereffects of the Brexit to some friction with the UK on potential trade talks. The markets fell, as the investors remained wary during the period. The cautiousness heightened due to the outbreak of the Novel Coronavirus and its spread across the globe. Another factor that dampened the sentiments of the UK economic climate was the declaration of flat GDP for the last quarter of 2019. Though there were some positives as well, which included employment in the country showing some signs of improvement, but the mood mostly remained grim during the month. The following is a brief overview of the UK economy for the month of February 2020.

Performance of the FTSE 100 Index for February 2020

(Source: Thomson Reuters) Daily Chart as on 28-February-20, after the closing of the LSE Market

The FTSE 100 Index of the London Stock Exchange was already reeling under the pressure of the after- effects of the Brexit as well as the geopolitical environment, but showed some signs of recovery in the middle of January 2020, but later in a sell-off lost around 3.40 per cent or 256.43 points for the month of January, following the early stages of the coronavirus outbreak. The index again displayed some positive signs in the first week of February 2020, as it gained around 2.48 per cent or 180.69 points by the end of the first week, as it closed at a value of 7466.70 points on 7th February 2020. This positivity, however, was short-lived, as the index started falling steeply after the Covid-19 virus was declared a global epidemic by the World Health Organisation (WHO). The index followed other global indices, such as the Dow Jones Industrial Average, which had lost approximately 10.32 per cent, while the NASDAQ 100 index lost around 7.20 per cent in value during the same period. Throughout the month of February 2020, the two major issues, that had a significant impact on the performance of the FTSE 100 were the beginning of transition period for the United Kingdom for exiting the European Union and the Coronavirus outbreak. By the end of the month, the weak geopolitical climate on the back of the epidemic, also caused massive losses to the benchmark index FTSE 100, as the index lost 9.68 per cent, or 705.40 points, and was reportedly closed at a 52-week low value of 6580.61 points.

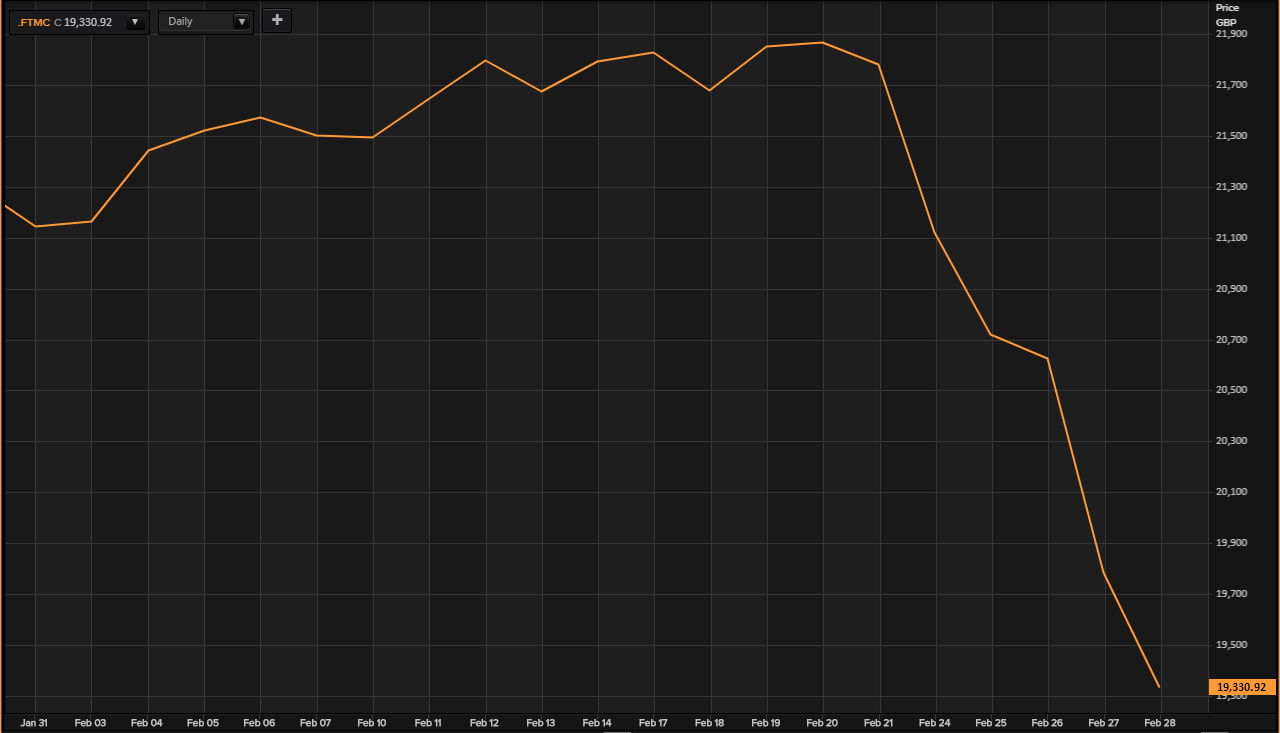

Performance of the FTSE 250 Index for February 2020

(Source: Thomson Reuters) Daily Chart as on 28-February-20, after the closing of the LSE Market

The FTSE 250 Index of the London Stock exchange, which mainly constitutes the mid-cap stocks in the London market, also followed the suit of the FTSE 100 Index for the month of February. The index value rose for the first week, and in fact, surged during the second week. The companies that are a part of the FTSE 250 index, generally have major trading activity either locally, or only in the European Union. Hence, the outbreak of the coronavirus in the first two weeks did not impact the index much. As soon as the news of the outbreak spreading to Italy came through, by the beginning of the third week of the month, thatâs when the index started falling, and eventually, as on 28th February 2020, at the time of the close of the market, the index slipped to a 52-week low value of 19330.92 points, a loss of 8.57 per cent or 1812.48 points in the month of February 2020.

Latest UK GDP Data

On 11th February 2020, the Office for National Statistics (ONS) released its first quarterly estimate of the Gross Domestic Product of UK for the month of October to December 2019. The announcement came with an important notice that following the withdrawal from the European Union, the ONS would continue to use the same methodology as previously used, to calculate the GDP and other economic measures for the United Kingdom.

As per the research presented in the ONS data, it was reported that UKâs Gross Domestic Product for the fourth quarter 2019, remained flat, as compared to the third quarter in terms of volume, after a revised growth of 0.5 per cent in the country during the third quarter. An increase of 1.1 per cent year on year was reported for Q4 2019, as compared to 1.2 per cent year on year growth in the GDP reported during Q4 2018. The ONS data also pointed that the UK GDP growth was unpredictable in the entire year in 2019, in part, reflecting changes in the planning of action in regard to the UKâs previous deadline for leaving the European Union. In spite of the fact that there is some proof, both, presented by external factors as well in the current data points, a lot of stockpiling has taken place during the later period of 2019 just prior to the second planned exit from the EU in the month of October; initial estimates suggest that this was to a lesser degree than that occurring before the first planned EU exit date, which was scheduled in the month of March.

Employment Data Springs a Surprise

On 18th February 2020, the Office for National Statistics reported the latest data for UK employment. The ONS highlighted that the Employment rate in the country had reached a record high of 76.5 per cent, around 0.6 per cent year on year increase and a quarter on quarter growth of 0.4 per cent. The unemployment in the country had also marginally declined, as the unemployment rate was reported at a year on year decline of 0.2 per cent and a quarter on quarter decline of 0.1 per cent to 3.8 per cent for the period. One of the biggest surprises came from the number of women in employment during the period, as the data suggested for the full time and part-time employment that the number of woman in full-time employment has increased faster in the past five years and at a much faster pace than men in full-time employment during the period.