_03_12_2026_20_44_50_714103.jpg)

When you first compare a merchant account with a payment gateway, they appear to be similar. In reality, they play very different roles. Understanding how money moves from a cardholder to your business helps you design a setup that supports growth, keeps costs predictable, and avoids surprises when something goes wrong.

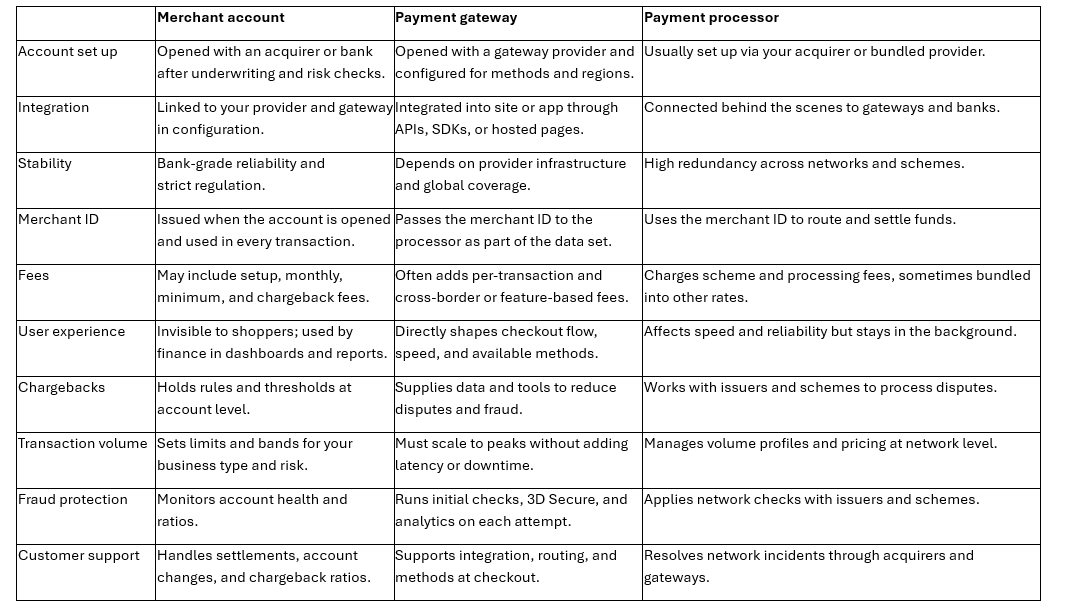

What is a merchant account?

Definition and role

A merchant account is a dedicated account that sits between the card networks and your main business bank account. It holds funds while authorisation, risk checks, and settlement is completed. Once the issuer and schemes approve the transaction, the money moves from the cardholder’s bank into your standard business account. Without this step, card and alternative payments would not reach your business in a controlled way..

Who needs a merchant account?

Any business that accepts card or electronic payments needs a merchant account . That includes ecommerce brands, marketplaces, in-store retailers, restaurants, hospitality venues, and subscription or membership companies. Even if a provider bundles services for you, there’s still a merchant account behind the scenes that identifies your business to banks and schemes.

What is a payment gateway?

Definition and role

A payment gateway is the technology layer that sends transaction data from your checkout to processors and banks and returns approvals or declines in real time. It connects your website, app, or POS to the wider payments network and keeps sensitive data secure in transit.

Who needs a payment gateway?

Any business that accepts online or in-app payments needs this layer. That includes ecommerce shops, SaaS platforms, travel companies, online service providers, and B2B companies with digital pay links. It’s also useful to think about payment gateway vs internet merchant account when you sell only online and don’t need in-store acquiring. For many digital merchants, the ecommerce payment gateway vs merchant account balance shapes how fast they launch and how easily they expand.

Why understanding the difference matters

Clear roles reduce confusion when you add new markets, methods, or channels. They also help your finance and risk teams see who makes key decisions and where fees apply. If you treat the whole stack as a black box, it’s harder to improve approval rates, manage chargebacks, or negotiate better terms.

Key differences

This is where choosing between a payment gateway, a payment processor, or a merchant account becomes most practical. You’re deciding who does what and how they connect.

How to choose the right setup for your business

Start by mapping where and how you accept payments today. List your channels, payment methods, volumes, and the tools that touch each step. Decide whether you want a single gateway layer or a mix of different providers. With payabl.checkout, you connect your online channels to your acquiring setup through one integration instead of stitching together separate tools. Then review your risk profile, regions, and roadmap to see whether that unified approach or a more fragmented mix gives you better control. This is where payment gateway vs internet merchant account choices become clearer, especially if you plan to add new channels or enter new markets.

Summary & what you should do next

The right mix of services depends on your size, industry, and growth plans. A good structure keeps funds flowing, reduces friction at checkout, and gives finance a clear view of performance. If you’re already clear on your needs, contact us for a payment gateway that supports modern methods, strong security, and clean reporting.

If you’re still mapping things out, contact us for a consultation to find out which setup fits you best. A payabl. expert can review your current stack, highlight gaps, and help you move toward a model that supports the way you operate now and how you plan to grow.

The content has been authored in collaboration with our guest contributor, Payabl.