With over 2,000 employees across Australia, China and Indonesia, Elders Limited (ASX: ELD) has been providing products, marketing options and specialist technical advice across the retail, agency and financial product and service categories.

Today, the company reported a decline of 41% in its Profit from continuing operations (After- tax) for the half year ended 31 March 2019 (H1 FY19). The Statutory net profit of the company was recorded at $27.4 million for H1 FY19 which was way lesser than $41.4 million profit recorded in the prior corresponding period (pcp).

Further, the company reported Underlying earnings before interest and tax (EBIT) of $33.5 million, around $12.3 million lower than pcp, mainly due to lower wool volumes, increases in costs associated with footprint growth, and continued investment in digital and technology areas. Due to investment in Titan, including working capital, and other bolt on acquisitions, and increased retail balances carried due to the seasonal conditions, the companyâs year to date average net debt increased by $81 million to $224 million at March 2019.

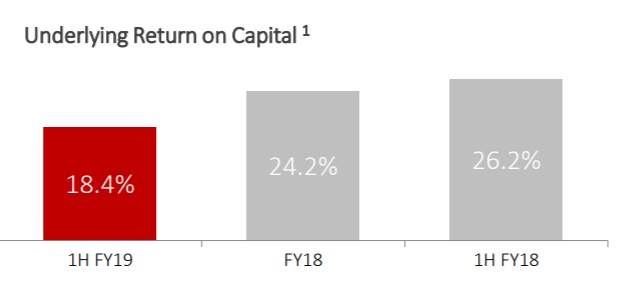

Due to recent investment activity performance impeded by unfavourable seasonal conditions and investment in digital and technical areas, the companyâs underlying Return on Capital reduced to 18.4% as compared to 26.2% in pcp.

Underlying Return on Capital (Source: Company Reports)

In the half-year period, the companyâs retail margin decreased by $1.2 million (2%) on last year, mainly due to dry conditions particularly across key areas in New South Wales. This resulted in reduced summer crop plantings and production, which has adversely impacted the demand for fertiliser and crop protection products.

During the year, the companyâs Agency margin declined by $3.1 million (5%) on last year, mainly due to Wool activity, with reduced bales sold across all geographies. However, the livestock margin benefitted from increased volumes for both cattle and sheep, due to dry conditions and lack of feed.

Besides this, the Real Estate margin during the period increased by $0.1 million, with water broking services providing the majority of the upside.

In line with the Eight Point Plan and the three-year goal to FY20, the company is targeting 5-10% EBIT growth, from 2017, through the agricultural cycle to 2020, while maintaining a return on capital at or above 20%. The company is expecting this EBIT improvement will be delivered from organic and acquisition growth and continued focus on controlling base costs to offset inflationary increases.

The company believes that it is on track to deliver its FY19 guidance. For FY19 the company is expecting its Underlying EBIT to be in between $72 to $75 million (as per FY19 Update published on 14 March 2019) and its Underlying NPAT in the range of $61 to $64 million. For the remainder of FY19, the company will continue to pursue organic growth initiatives and acquisitions.

In the last six months, the share price of the company decreased by 15.53% as on 17 May 2019. At the time of writing, i.e., on 20 May 2019 AEST 12:43 PM, the stock of the company was trading at a price of A$6.580, with the market capitalisation of ~A$768.13 Mn.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.