About Global LIC

Investments in global Listed Investment Companies (LICs) most commonly exhibit the investor to a bag of underlying shares with a difference in investment techniques and operational characteristics from one company to the other.

The diverse range of investments options available for the investor through global LICs can suit various types of investors with differing objectives.

LICs enable an investor to make an investment in a varied and competently managed set of assets like shares, property and interest-bearing deposits.

In Australia, the LICs largely invest in Aussie or global shares while exposing investors to assets that can be accessed via several unlisted managed funds.

Characteristics of Global LIC

Close-Ended Structure

One of the characteristics of a global listed investment company is the close-ended structure of its funds. Listed investment companies do not ideally issue fresh shares or cancel them regularly as investors tend to enlist and leave the fund from time to time. The process of buying and selling the shares in a LIC is executed on a stock exchange where the funds are listed.

The closed-ended structure gives the fund manager an advantage to focus on choosing investments without worrying about the instability caused due to money added into or taken out of the fund while opting for a long-term approach to investing.

Exposure to Globally Listed Securities

A global listed investment company provides the investor with exposure to the diverse and globally listed securities. The choice of the global listed investment company is at the investorâs discretion as per his investment needs. Moreover, markets with different economic, political and demographic profiles can be accessed by the investor. Global listed investment companies also put forward the opportunity to invest in the companies operating in countries that have faster growth than the domestic Australian economy.

Net Tangible Assets (NTA)

Another characteristic of the global listed investment company is the value of the underlying assets held by a LIC on a per-share basis or otherwise the Net Tangible Assets (NTA). The LICs are required to report their NTA regularly, which further assists in determining the performance of a LIC (whether a LIC is trading at a premium or a discount to its NTA).

The data about current and historical LIC premiums or discounts to NTA is imperative for the investors while making the decision to purchase or sell the investment.

We shall now discuss the characteristics of a global listed investment company, Ellerston Global Investments Limited (ASX: EGI), which announced to its shareholders an update regarding its strategy to close the discount to NTA.

EGI Paid 12.5 Cents Per Share of Dividend

Ellerston specialises in equity and alternative strategies with over $5 billion in funds under management currently. Since its incorporation till 7 November 2019, the Company has paid a dividend (fully franked) of 12.5 cents per share to investors.

Moreover, EGI has retained a strategy for the payment of sustainable dividends in future with a current dividend profit reserve of 5 cents (fully franked).

Discount to Net Tangible Assets

EGI has one of the lowest management fee structures as compared to its global equity peer companies. The Company is of the view that

- There are structural issues in the marketplace inherent to a listed company structure with insufficient scale that creates a dislocation between the portfolio return and shareholder returns.

- It is important to note that the discount, while unacceptable, is an industry wide phenomena, with the listed global equity sector trading at an average discount of over 17% as at 30 September 2019, and is often a reflection of overall market sentiment, volatility and other events which can reduce investor demand.

The Company Board views the discount between the NTA and the share price to be unacceptable and earlier committed to its shareholders an intent to carry out a strategy to close it.

With a focus on opportunities overlooked by the market, the Company portfolio has reported strong results. The underlying cumulative net performance of the strategy in the five years till 31 October 2019 was recorded at 56.9% as compared to the target return of 50.4%.

However, the shares continued to trade at a discount like most of their listed peer groups.

As an effect of persistent discounts and in advance of the 2019 AGM, EGIâs Chairman, Ashok Jacob mentioned the Boardâs proposed strategy.

Transition to a Trust Structure

With specialisation in equity and alternative strategies, the Company Board determined to eradicate the discount and to provide to those shareholders who seek for liquidity at a price more closely approximate to underlying asset value with a clear pathway to redeem at NTA.

Most of the shareholders want a structure that provides this choice and flexibility, while others look for the option to remain invested in the strategy.

In the absence of a better alternative, at this juncture, the Board believes that an orderly conversion of the Company's investment portfolio to a trust structure is the most appropriate path to liquidity while enabling a return closer to NTA.

By pursuing an orderly transition to a trust structure, the Company believes it avoids the following:

- EGI becoming a forced seller of assets that may not have realised their long-term value;

- Unintended costs and potential taxation implications for EGI; and

- Imposing the will of those shareholders who wish to exit early on those investors that have invested in the strategy for the medium to long term.

EGIâs Investment Strategy

EGI was launched in 2014 for the investors looking for access to international investment prospects with persuasive risk/reward profiles that are prominent in a domestic equity portfolio.

Specifically, EGI seeks to capitalise over the Manager's capabilities to pick suitable stocks and offers access to lesser-known companies that are usually unavailable in global equity funds or listed investment vehicles.

When EGI was launched, the formulated strategy of the Manager (unlike the majority of available global equity funds) was that the portfolio would be principally hedged against currency gains or losses, meaning that the return of EGI to reflect the underlying performance of the invested companies instead of the performance of the Australian Dollar.

As such, the Manager made use of MSCI World Index (Local), a global benchmark which also does not include any currency gains or losses, meaning that the EGIâs return profile not to be compared with the unhedged worldwide equity funds or listed investment vehicles.

EGIâs Portfolio Performance

As per the Company reports, the performance of the underlying portfolio as at 31 October 2019 has been strong and exceeded its benchmark on an annualised basis since incorporation.

The net of fees performance of the portfolio to its benchmark over corresponding periods is shown in the table below:

Figure 1 Portfolio Performance (Source: Company's Report)

The smooth performance of the portfolio is evident from the above returns that have been achieved while also achieving a lower level of volatility than the benchmark over the relevant period.

The Company management is of the view that the portfolio shall remain in pursuance of its objective to generate exceptional returns for shareholders over time, with a focus on managed risk and capital conservation.

EGI stock trading close to 52 weeks high

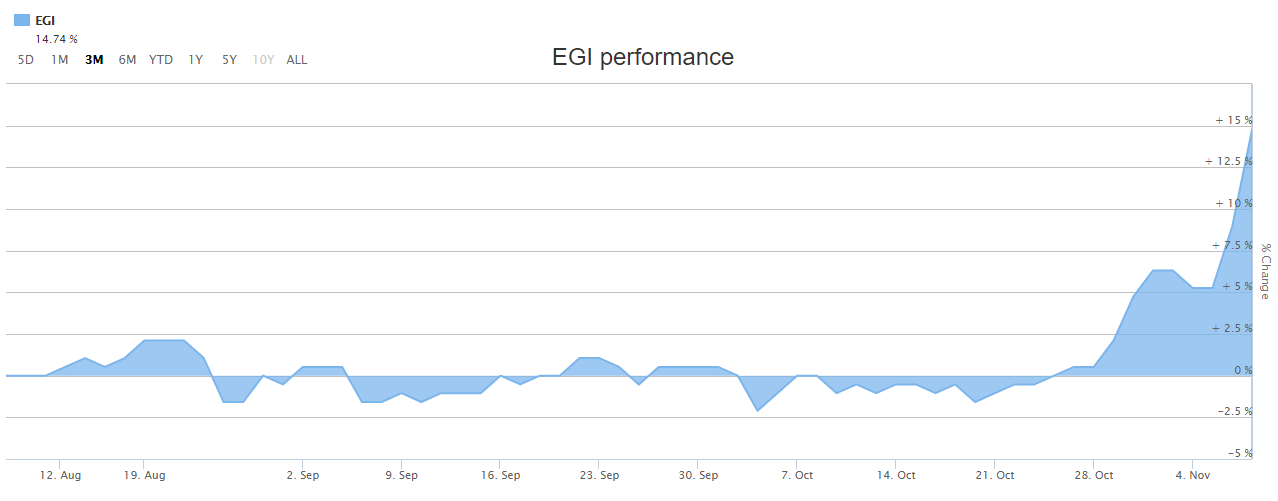

At the market close on 8 November 2019, EGI stock last traded at a price of $ 1.112, up 2%, close to its 52-week high price of $1.115 with a daily volume of ~585,428. The company has a market capitalisation of approximately $116.09 million with a 52-week low price of $0.875 with an average volume of ~208,545.

Figure 2 EGI 3-month return (Source: ASX)

Figure 2 EGI 3-month return (Source: ASX)

Over the period of last three months, EGI stock has provided 14.74% return.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.