Adairs Limited (ASX: ADH) is involved in the retailing of homewares and home furnishings in Australia and New Zealand via online and traditional stores. It was officially listed on ASX in 2015. Recently, the company updated the market that one of its substantial holders, namely Commonwealth Bank of Australia and its related bodies changed its voting power from 5.32% to 6.47% with effect from 20th June 2019.

Trading Update

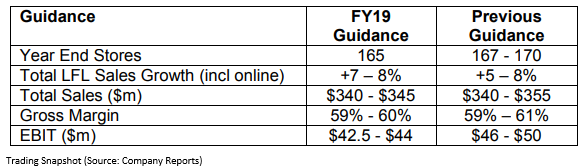

The company, on 21st June 2019, reported that it had experienced a negative change in its trading momentum. The company witnessed no change in like-for-like sales since 27th May 2019, with significant volatility observed from week-to-week. This performance marked a material reduction from more than 9% LFL sales growth delivered over the second half up to 27th May 2019. The change in sales performance in an important trading period coupled with a continuation of higher costs and the associated gross margin pressure have contributed to the revised guidance, as can be seen in a below table.

Notice of Ceasing to be a Substantial Holder

In another update, the company highlighted that Yarra Funds Management Limited, Yarra Capital Management Holdings Pty Limited, Yarra Management Nominees Pty Limited, AA Australia Finco Pty Limited, TA SP Australia Topco Pty Limited and TA Universal Investment Holdings Ltd ceased to be the substantial holder of the company since 31 May 2019.

Half Yearly Results

In 1H FY19, the company witnessed a growth in sales throughout both online and offline channels. The sales stood at $164.4 million, reflecting a rise of more than 10.6%. The sales growth was driven by the performance of expansion categories, including home décor and Adairs kids, with support from its core categories of bedlinen, bathroom and bedding. In terms of online sales, the company has outperformed the market in online penetration. The online sales witnessed a rise of 42% and contributed 15% of the total sales. The growth was delivered by strong execution of its digital strategy and omni channel approach.

Additionally, the continued investment in Linen Lover Loyalty Program has seen customers shop more frequently throughout channels.

The companyâs product category continued to deliver with significant upside potential. In the most expansion categories, the company remained a relatively small player in the fragmented market. It is focusing on furnishing more of its customersâ homes, allowing the company to grow its share of existing customers purchases rather than relying on acquiring new customers for growth.

The gross margin of the company amounted to 60.9% as compared to the industry median of 23.3%. The net margin of the company stood at 9.1% against the industry median of 5.7%. This represents that the company is in a better position in order to convert its top line into the bottom line. The current ratio of the company stood at 1.44x, reflecting a Y-o-Y growth of 4.6%. This implies that the company is improving its capabilities to address short-term obligations.

Importantly, the company, in Wilsons Rapid Insights Presentation, highlighted its Omni Channel success driving sales growth for ADH. The company has best-in-class omni channel retail capabilities with a âchannel agnosticâ approach that drives online sales and encourages engagement so that customers can easily research and browse online and shop in store or vice versa. The companyâs strategies link back to building more omni channel customers who are more engaged and overall, spend more in store and online. Additionally, the company continue to see online channel delivering significant sales growth as both existing and new customers prefer to shop online more.

The omni channel is driving traffic to the site, which has been the biggest driver of its online sales growth. The company further elaborated that it is utilising the customer database in order to build an effective email program, which is a cost-effective traffic driver. The organic social, with platforms such as Facebook and Instagram, has also been a strong channel for brand marketing and inspiration. When building traffic, the cost of customer acquisition is a key factor, and the company continue to see a reduction in its acquisition cost per first time customer.

Linen Lover Program: The company continues to grow its Linen Lover customers through a strong loyalty value proposition, which consists of $20 membership fee for 24 months membership, $20 voucher (min spend $50) on next purchase, exclusive Linen Lover offers and bi-annual shopping events and free online delivery and returns, with in-store team driving signing up Linen Lovers. The members represent more than 70% of its sales, allowing deeper insight into what members want and expect from the company. Additionally, the Linen Lovers spend on average 1.7x more per transaction than a non-Linen Lover.

The company has more inspiring larger stores as the larger store format enhances the shopping experience, differentiating ADH from its competitors and supports the strategy of category expansion. The company has 49 homemaker stores in Australia, with five mini homemakers stores in shopping centres and four stores in New Zealand, collectively representing 48% of the total sales. The additional growth has been delivered by the store roll out, selectively upsizing shopping centre and smaller homemaker stores. The selectively upsized stores delivered sales growth of 33.3% and store contribution growth of 31.4% in the first 12 months.

FY19 Guidance: In line with the long term targets, the company expects the full year like-for-like sales growth to be around 7% to 8%, indicating consistent growth throughout H1 and H2. The companyâs key strategies are continuing to drive above market sales growth. The online segment delivered growth of roundabout 40% in the second half to date and will demonstrate 17% of its total sales for FY19. Moreover, the companyâs New Zealand business as well continue to improve performance and build momentum.

The company further pointed out that the current inventory position and cash generation are in check with its internal plans. On the flip side, the growing pains within its distribution network are negatively impacting its earnings performance. It is focused on delivering a seamless omni channel experience and there are significant opportunities ahead for the company to further improve its conversion. The company expects to open four to six stores per annum over the next three years with a continued bias towards larger store formats.

At the time of writing on 26th June 2019, AEST 01:00 PM, the stock of ADH was trading at a price of $1.400, down 0.709%, with a market capitalisation of $233.88 million. The stock has provided negative returns of 17.54% and 22.31% for three months and six month period, respectively.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.