_07_03_2026_03_50_21_133108.jpg)

Summary

- With the Australian economy gradually opening up, the insurance industry is on the path of recovery after hitting rock bottom in March 2020.

- Recession proof model, higher net profits coupled with declining interest rates on cash assets in Australia makes it a safe bet to invest in.

- Heavily guarded by regulation, the industry is embracing technology such as Artificial Intelligence and Blockchain to understand customer behaviour and enhance value chain.

- Investments in digitisation and better processes to provide seamless customer experience is trending in the industry.

The insurance sector is a safe bet for investors looking for long term returns. An insurance company earns from a huge resource pool as premiums and pays fewer claims to earn huge profits. As the money received is huge compared to pay-outs, the surplus money also known as float is used to buy safe investments, creating more returns for the insurance companies. The industry is also recession proof as most of the people try to maintain asset related coverage.

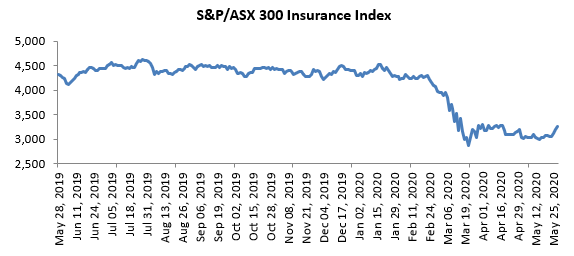

However, the current COVID-19 pandemic coupled with bushfires (earlier this year) has exposed the insurance companies to an unprecedented risk exposure. The S&P/ASX 300 insurance index closed at 3,264.20 points on May 27th, 2020, a decrease of 24.39%, affected by the bushfire and pandemic events from February 2020. The S&P/ASX 300 insurance index hit 52-week low on March 23, 2020 hitting 2,872.34 points and since then has increased by 14% within ~2 months period, indicating path towards recovery.

Insurance Australia Group Limited (ASX:IAG), QBE Insurance Group Limited (ASX:QBE) and Suncorp Group Limited (ASX:SUN) are the leading insurance providers in the Australian market with billion dollar market capitalisation. Share prices of all the leading insurance providers have plummeted significantly in last three months due to the pandemic. However, all these stocks are showing signs of recovery.

Also Read: Private health insurers continue to struggle in Australia

But how to know which stock is worth investing?

Following key performance indicators (KPIs) are instrumental to understand the strength of an insurance company

- Claim Ratio - total claims to net premiums

- Average cost per claim – total payout of the organisation by total number of customers

- Loss Ratio – total losses sustained (both paid and reserved) mentioned in the claims combined with adjustment expenditures divided by the total premiums earned

- Expense Ratio - expenses associated with acquiring, underwriting, and servicing premiums by the net premiums

These KPI’s allows an investor to analyse the performance of any insurer covering any product. An insurer generally covers life risk, health, medical costs, property, accidents, and many valuable assets for individuals. For businesses, losses incurred through damage, injury, natural calamities, and others are covered by insurance.

Unforeseen events such as pandemics and climatic disasters lead to a huge pay-out in a very short span of time. These events also disrupt economies and affect income of individuals and businesses creating uncertainty on maintaining future premiums. Other issues such as reduced capacity, legislation changes, and advance d technologies are also affecting the companies profoundly.

Let us see in detail the factors favouring the insurance industry and what not.

Factors favouring the insurance Industry

- High Earning Profits of the companies; Insurer provides a guaranteed payment covering an uncertain future incident in lieu of a premium to be collected periodically over a certain period of time. The total premium collected is huge compared to claims paid out, leading to huge profits.

- Recession proof model: The industry is considered recession proof as most of the people try to maintain asset related coverage. Recession proof model make insurance shares less volatile in the market, providing long term returns.

- Declining Interest rates: Declining interest rates in Australia has made investment income for the insurance industry more desirable as they provide better returns compared to cash assets.

- Advent of technology: The industry is currently experiencing technological advancements such as use of AI and robotics to understand human behavior and activity. The industry is also using the blockchain technology to make the whole value chain transparent through real-time data.

Risk Factors

- Regulatory agenda: Insurance companies are subjected to heavy regulation. Recently, the Australian government had set up an ambitious regulatory agenda by implementing all the recommendations of the Royal Commission that are relevant to insurance sector. The agenda completely safeguards customer interests with respect to fraudulent contracts, fairness in contract and regarding selling ad distribution of insurance.

- Cyber security: Cyber security challenges the insurer and the client equally as it involves data breach. Apart from regulatory fines, the companies also incur cost because of litigations and lawsuit claims filed by customers. A cyber threat or attack also hampers the business operations.

- Coping up with customer dynamics: The insurance industry is turning towards becoming more customers centric by managing premiums and policies suitable to both clients and own business. The companies are focusing hard to enhance customer experience through products customized as per customer need. However, matching with customer expectations comes with a cost. In order to provide seamless journey to the customers, the companies invest in various technologies and customer care processes. To gain and retain customers, a company shrinks its profit margin further by making products affordable.

- Climate change: Global warming has led to increased number of natural calamities such as bushfires, storms and floods impacting business production, income, and property damage. These losses have led to a spike in insurance claims. According to ABS, the claims from the bushfire (earlier this year) accumulated nearly equally in both the December last year period and March quarter, as per data received from the insurance sector. With climatic disaster turning common, the insurance is subjected to more pay-outs than earlier.

- Pandemic Effect: The pandemic has demobilised the entire economy with social distancing and other containment measures. Social distancing has led to less travel and hence, travel and auto-related insurance sales have plummeted. The pandemic has also prompted people to file for home and content insurance claims, affecting liquidity the profit margin of the insurers.