If you’re confused about what’s going on with the economy right now, you’re not alone. On one hand, unemployment is low, stocks are near all-time high, and inflation is cooling.

On the other, consumer confidence is falling, the Fed is stuck, and everyone is still talking about tariffs.

Some numbers say one thing. Sentiment says another. Markets don’t seem to care, until they suddenly do, and then they don’t again.

This isn’t just noise. It’s the result of conflicting forces playing out all at once.

And they’re creating an environment that feels stable on paper but uncertain in practice. Here’s what’s really happening, and what investors should expect next.

What the numbers say — and what they don’t

Start with the hard data. The US economy added 139,000 jobs in May.

Unemployment is at 4.2%, which is low by historical standards. Wages are still growing, up 3.9% year over year.

The stock market is near record highs, with the S&P 500 and Nasdaq both in the positives this year. These are not recession indicators.

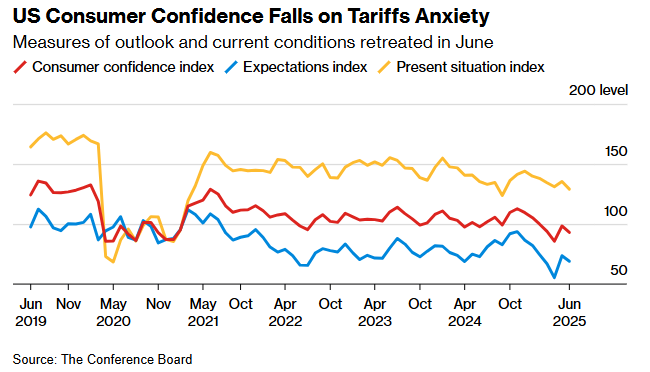

But now look at how people feel. Consumer confidence fell to 93 in June, according to The Conference Board.

That’s a 5.4-point drop from May and the lowest this year.

The index measuring expectations for the next six months is even worse. It dropped 4.6 points, with fewer people expecting better business conditions or job prospects.

That disconnect is where the confusion starts. Economic behavior usually follows sentiment.

But right now, people say they’re anxious. Anxious about jobs, interest rates, and global risks, while still spending and working.

Economists call this the “vibecession.” Data looks fine. Mood does not.

Why tariffs are back on the radar

In April, President Donald Trump paused most new tariffs for 90 days, except those on China. That window ends on July 9.

Markets largely ignored it at the time because geopolitical tensions with Iran had taken the spotlight. But investors are now turning their attention back to trade. And for good reason.

Morgan Stanley analysts say the inflation impact of tariffs tends to show up with a two- to three-month lag.

So while CPI data in May looked soft, that might not last. By late summer, prices for imported goods could rise again.

That would make it harder for the Fed to justify cutting interest rates, something many in the market still expect to happen.

Trump has signaled he wants to keep pushing what he calls “reciprocal tariffs” on countries that he claims overcharge US exports.

The problem is, that strategy adds complexity for businesses, raises input costs, and injects uncertainty into global supply chains.

If tariffs snap back in July, companies may pass those costs on to consumers. Inflation could return just as the Fed prepares for a possible rate cut.

That’s why the July 9 date matters more than markets currently acknowledge.

The Fed is stuck and everyone knows it

The Federal Reserve has a credibility problem. Not because it’s wrong, but because it’s constrained.

Chair Jerome Powell has said the Fed won’t cut rates until it’s more confident that inflation is under control. But with tariffs lingering and growth slowing, the pressure to act is building.

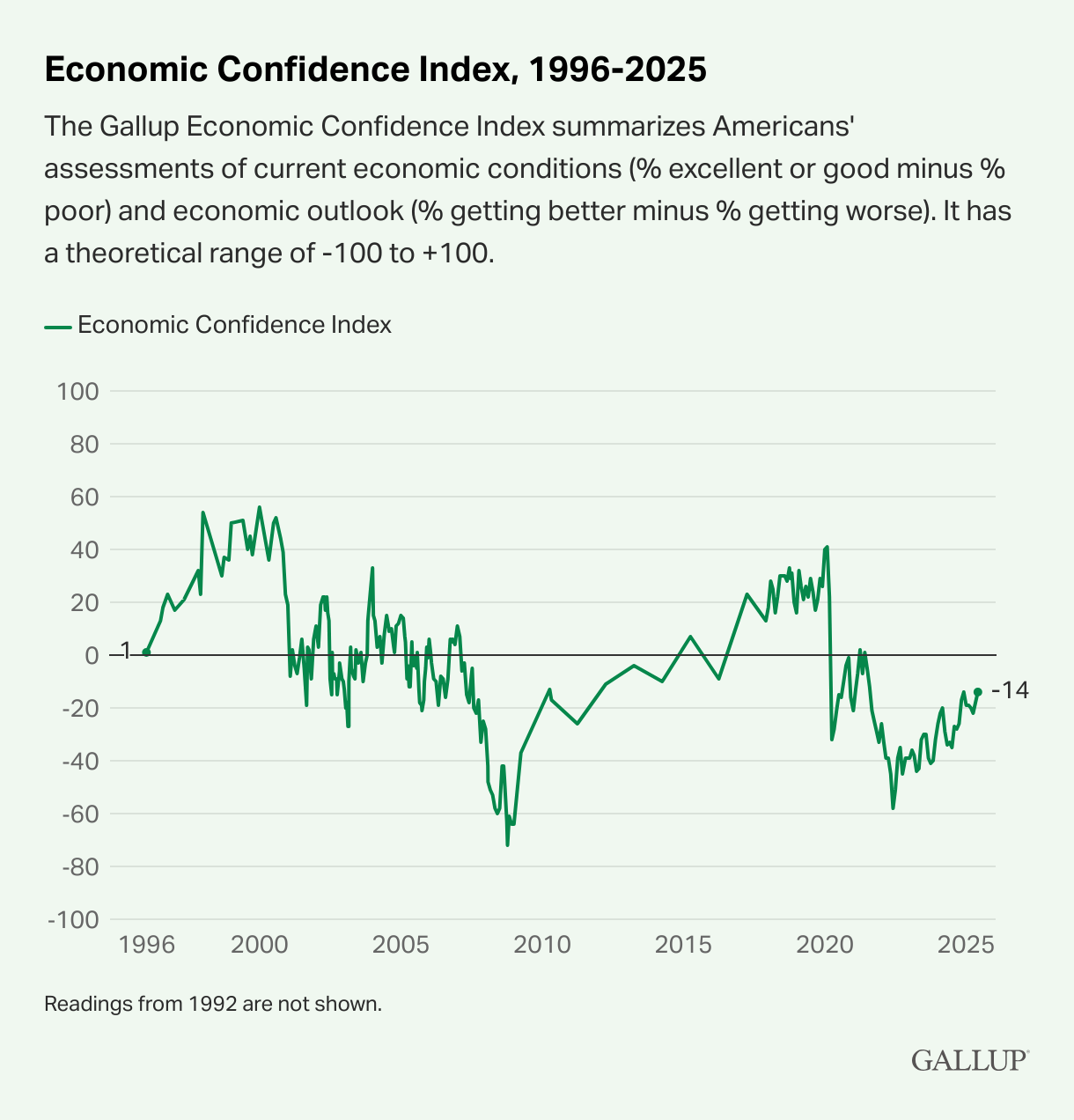

Gallup’s Economic Confidence Index remains in negative territory, at -14 in June. That’s up slightly from May, but still low. Sixty percent of Americans say the economy is getting worse.

Most Fed officials are still holding a wait-and-see stance, but some are pushing for action in July.

There’s no Fed meeting in August. That adds urgency to the next decision.

The problem is, the Fed doesn’t control tariffs. It reacts to their effects. If inflation rises later this summer because of trade policy, rate cuts might be delayed.

But if consumer spending slows first, the Fed may be forced to cut anyway.

Powell’s team is now navigating both inflation and recession fears at the same time. That’s a rare and uncomfortable place to be.

Is geopolitics off the table now?

Not entirely. But it has faded for now. Earlier this month, the US and Iran agreed to halt further escalation after a short military exchange.

That ceasefire caused oil prices to drop nearly 6% in a single week, easing fears of a global supply disruption.

Lower oil prices fed into a brief market rally. Energy-driven inflation pressure eased.

But the Middle East is not fully settled. Nor are US-China trade relations. Taiwan remains a flashpoint.

And the European Union has hinted at retaliatory tariffs of its own if Trump extends his strategy further. In this kind of environment, volatility can return quickly.

Markets are betting on peace. But if another flashpoint emerges, such as in Asia, Ukraine, or even at home, investor confidence could shift again.

Geopolitics aren’t driving the market today, that’s why the reaction to the latest developments was muted. But the worry hasn’t gone away.

Consumer confidence is likely to tick even lower for June, as it’s a lagging indicator.

What comes next? Scenarios and signals to watch

The most important date ahead is July 9. That’s when the White House must decide whether to extend the tariff pause or resume its trade war strategy.

A pause extension could calm inflation fears and give the Fed more room to cut rates in July or September.

A re-escalation would likely push inflation back up and force the Fed to stay put.

Another key signal is consumer behavior. So far, consumers say they’re worried, but they’re still spending.

If retail sales and auto purchases drop sharply in July and August, that may be the moment where sentiment finally catches up to reality.

Also closely watch the next CPI report. If price pressures rise, especially in goods categories tied to trade, that will confirm Morgan Stanley’s thesis about delayed inflation from tariffs.

That would complicate the Fed’s path and increase market volatility in Q3.

There is also political risk. Trump’s approval rating was 40% before the Iran strikes; the lowest of his second term. WIth many Americans disapproving Trump’s actions, that could drop even further.

Trade wars that hurt prices and confidence could weigh further.

But the administration may also view them as necessary to shore up support among industrial-state voters ahead of the 2026 midterms.

If tariffs resume in July, inflation ticks up in August, and the Fed hesitates to cut in September, markets may retreat from their current highs.

But if tariffs stay paused, inflation holds steady, and the Fed delivers a July cut, a broader rally could continue into the fall.

Either way, clarity won’t come from data alone. It will depend on policy and timing. Right now, we have little of either.

That’s why everything feels confusing.

The post Why economy and stock market feel strong, weak, and broken all at once appeared first on Invezz