Summary

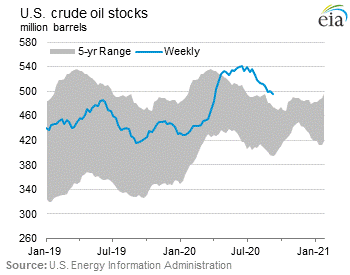

- The U.S crude oil inventory dropped below 500 million barrels at the beginning of September

- The U.S import of crude declined to 5.5 million barrels per day and exports soared to six months high level of 1.2 million barrels per day.

- The hurricane in the Gulf of Mexico could further squeeze the production and impact on crude oil prices may be seen in near terms.

U.S. crude oil stockpiles are declining as imports from Saudi Arabia are declining and exports rising. The exports have increased by 1.2 million barrels per day, with China being the major consumer. China has imported nearly 1 million barrels per day throughout the month of July.

The Chinese U.S Crude oil imports have increased more than two folds as compared to the imports registered in the year 2018 and US-China trade relations were on a better footing. U.S crude inventory fell to 496 million barrels in the first week of September. This is the lowest level since April and is expected to decline further.

U.S imports from Saudi Arabia declined in the month of July and August. Saudi Arabia has been abiding by the production output cut deal as decided by the OPEC+ countries.

Source: Energy Information Administration

The OPEC+ nations followed the production cut accord for the entire month of July. China is also in compliance with the first phase of the “Trade Deal”.

Also Read: OPEC And Russia Meet to Push for Iraq and Nigeria Compliance

The crude oil prices have shown little upward movement since July. But the future market is still susceptible to the price, which can be witnessed in the widened gap between the prices of near-term and longer-term stocks. The widened gap may be the indication of reduced purchase from the downstream industry, or it may also indicate an increase in the supply, which in turn suggests a slower rate of growth in demand in the global market.

The EIA data suggests that the huge inventory withdrawals during the second half of 2020 will cease next year, leading to a more balanced market. According to the EIA estimates, the inventory withdrawals will be around 3.4 barrels per day in 2020 which could slip to around 0.3 million barrels per day.

OPEC Reference Basket (ORB) increased by 4% month on month basis in August. Future price also increased by nearly 4% showing positive indications of price recovery. But the contango formation in the crude oil Future market has kept Hedge Fund managers away from taking clear positioning in August.

Global Crude Oil Demand

According to OPEC statistics, the global crude oil demand will stand at about 90.2 million barrels of oil per day. The demand from OECD countries is expected to rise more quickly because of the early recovery from the Covid-19 crisis and better performance of other sectors of the economy. The demand is forecasted to be weaker in non-OECD countries, particularly in Asia.

Fear of the second wave of the virus spread and no availability of potential vaccine soon is still plaguing the market. Demand from other sectors of the economy has also dropped as people have opted to buy only essential items and have curbed their spending habits. The transportation sector is the second-highest consumer of crude oil. Since demand is low in the economy for the non-essential items, the transportation system is yet to pick up steam, and thus, lesser will be the growth in demand from this segment. The OPEC estimates that global demand for crude oil in 2021 to increase to 96.9 million barrels per day.

Global Crude Oil Supply

The latest August data shows that OPEC+ crude oil production stands at 30.76 million barrels per day. The non-OPEC countries are producing 63.84 million barrels per day. The production cut by OPEC+ has helped to maintain the demand and supply gap. The crude Oil production forecast for 2021 is estimated to be around 100 million barrels per day, which is still higher than the 2021 demand forecast. OPEC+ and Russia have to formulate methods to cut the production output irrespective of the market share.

Monthly Average Crude Oil Price (Pre-Covid and during Covid Scenario)

Factors impacting crude oil prices

- Market Share: Recently, it was seen that Saudi Arabia started supplying China with crude oil at a price lower than the International market. Except for Iraq, other Middle East countries are increasing their production. Russia is trying to increase its market share, and the crude oil market was under pressure last time Russia did the same in February 2020. China is compelled to buy the U.S. crude oil due to the trade agreement. After a brief shutdown in the Gulf of Mexico, the production from the U.S. is set to rise in the near future.

- Strait of Hormuz is becoming hot zone due to the friction between Iran-USA and Iran- Saudi Arabia. Any war or conflict can escalate the prices very rapidly.

- There has been production disruption in Libya, Nigeria (offshore) and Iraq. These factors may cause a spike in the crude oil market.

- The U.S. presidential election may impact the drilling of Shale Oil.

Conclusion

The crude oil Future market is optimistic about improving the economic situation with each passing day. But the formation of contango is inducing doubts in the minds of Hedge funds and other fund managers. They are not in a position to take a clear stand on the trend of the crude oil market. At the same time, the USA inventory stockpile is decreasing, OECD Europe’s stockpile has also reduced indicating increased refinery operations and demand for the finished products. Also, the second wave of Covid-19 has been not reported on a large scale, and some news from Russia of developing the potential vaccine might bring positivity in the market and, help in increasing the demand to pre-pandemic levels.