The benchmark index, S&P/ASX 200 is trading at an all-time high, thanks to the dazzling performance of top gunners such as of Rio Tinto Limited (ASX:RIO), BHP Group Limited (ASX:BHP), Fortescue Metals Limited (ASX:FMG) on the exchange.

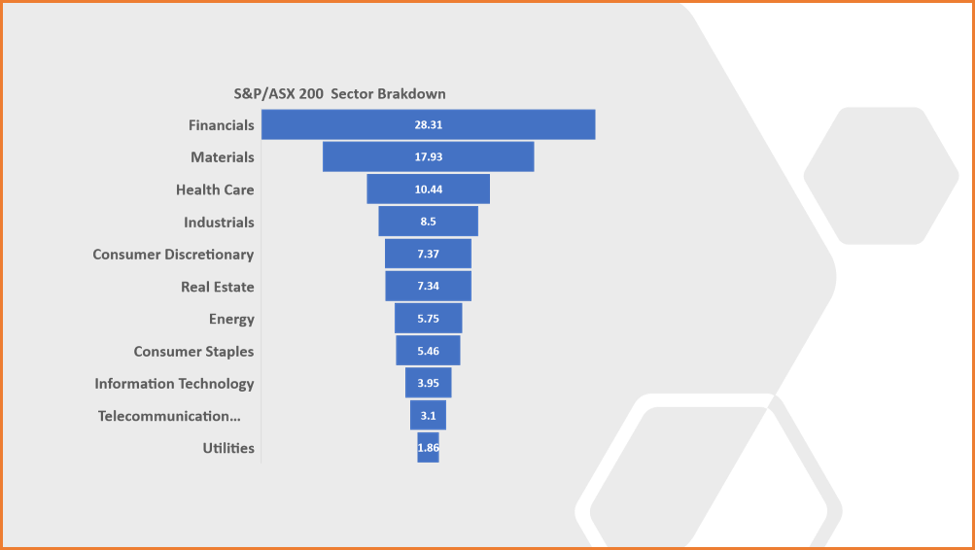

Material stocks are a charmer around this point of time since this sector holds 2nd largest weightage in the S&P/ASX 200, around 18 per cent is constituted by materials (resources) as on 17 January 2020.

Source: ASX

Also Read: Amidst Multiyear Index Highs, Resource Stocks-PRU, AWC, and S32 Announce Quarterly Report

While top gunners such as Rio, and BHP are reaping the benefits of being multi-commodity miners, the pure play gold stocks such as Northern Star Resources Limited (ASX: NST), Newcrest Mining Limited (ASX: NCM), Resolute Mining Limited (ASX: RSG), and many others are charging high on ASX over a sharp recovery in gold prices post a deep consolidation.

The resource sector has flourished so far in the wake of recovery in commodity prices such as of iron ore, copper, nickel, and cobalt, while gold stocks are under the run over much-anticipated rally in gold ahead.

Also Read: Get Ready to Pay ~2.8k for 24k Gold; Gold Bulls Break the Gated Cage

The currency depreciation along with recovery in commodity prices has played a significant part in pushing the resource and gold players up, which in a cascade, now igniting the S&P/ASX 200 Index to trade off the charts. However, many economists anticipate the home currency to gain strength ahead, which could have an impact on export earnings of resource and gold players.

To Know More, Do Read: ASX Gold Stocks Not as Shiny as Global Peers?

Albeit, despite headwinds, top gunners now intend to up the volume game in order to counter the issue of projected appreciation in the home currency.

Also Read: Global LNG Supply Glut Prompts ASX-Listed Oil & Gas Explorers To Play The Volume Game

Amidst record high S&P/ASX 200 index, Rio Tinto and Resolute Mining are out with their past performance and future intentions. Let us now take a look over their quarterly performance and try to gauge out how the resource players intend to sail across future gales.

Rio Tinto Limited (ASX:RIO)

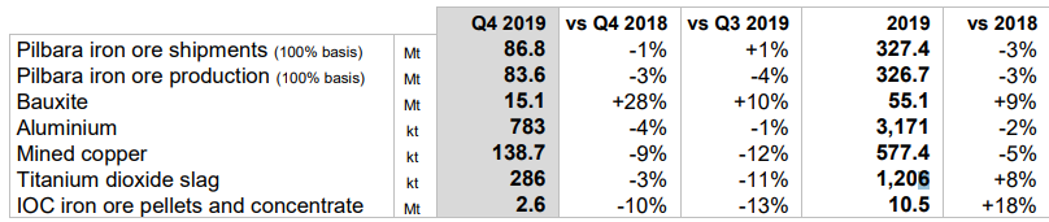

On a 100 per cent basis, Rio shipped 86.8 million tonnes of iron ore during Q4 2019, which remained a unit per cent up against the previous quarter, but a unit per cent down against the previous corresponding period (or pcp).

In 2019, Rio shipped 327.4 million tonnes (100 per cent basis) of Pilbara iron ore, down by 3 per cent against pcp. The production of Pilbara iron ore stood at 83.6 million tonnes in Q4 2019, down by 4 per cent against the previous quarter and down by 3 per cent against pcp.

the yearly Pilbara shipment took a hit from the weather challenges posted by the tropical cyclone Veronica on the Rio’s operations during the first half of the year 2019, while the quarterly Pilbara shipment took a strategic hit when the miner decided to reduce the production to maintain the quality of the Pilbara iron ore blend.

However, as stated above, the high prices supported the stock, and despite a slight slip in the production and shipment, the stock is trading near the 52-week high of $106.922 at $105.240 (as on 17 January 2020 3:58 PM AEDT).

Rio realised an average price of USD 79.0 per wet metric tonne of Pilbara shipment during 2019, up by 37 per cent against pcp.

The other segments of the company performed mix bagged and as below:

Source: Company’s Report

Future Intentions

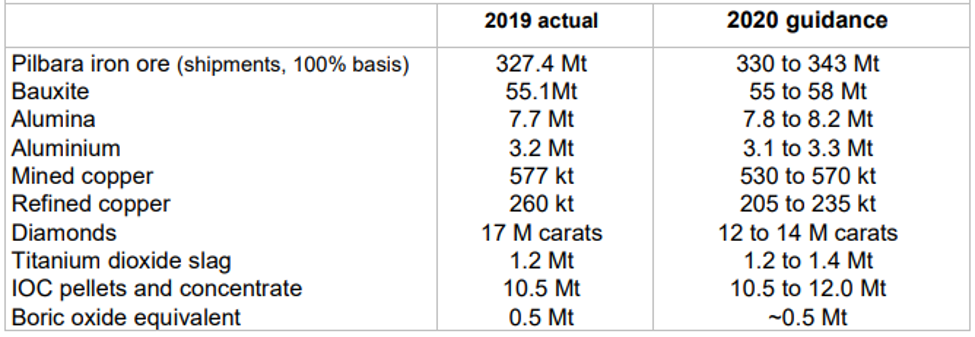

Rio kept the FY2020 production guidance for Pilbara shipment between 330 million tonnes to 343 million tonnes, up by ~0.79 per cent (at the lower end) from 2019 shipment and up by ~4.76 per cent (at the upper end) of the guidance range against 2019 shipment of 327.4 million tonnes.

The production guidance for other commodities are as below:

Source: Company’s Report

From the production guidance and indication from the higher management, it seems the mammoth is ready to counter the currency appreciation ahead with strong project pipelines and higher production.

Resolute Mining Limited (ASX:RSG)

After selling Ravenswood prospect to EMR Gear consortium, RSG is already flashing over the headlines of many media houses, and RSG is now out with the quarterly performance.

Also Read: Resolute Sells Ravenswood: Everything You Need to Know About the Deal

RSG managed to produce 105,293 ounces of gold during the December 2019 quarter with an all-in sustaining cost of USD 1,419 per ounce. The overall gold production for 2019 reached 384,731 ounces with an AISC of USD 1,090 per ounce.

The company sold 394,920 ounces of gold during FY 2019 at an average price of USD 1,344 per ounce; however, the higher cost of production at the present moment is keeping a lid on the gains, and the stock is relatively underperforming the peers on ASX.

RSG, WAF, and PRU Total Return (last one year) (Source: Thomson Reuters)

However, despite the cost challenges currently faced by RSG, it has kept the production guidance for FY 2020 at 500,000 ounces of gold with an AISC of USD 980 per ounce comprising 260,000 ounces at USD 960 per ounce from Syama, 160,000 ounces at USD 800 per ounce from Mako and 80,000 ounces at USD 1,200 per ounce from Ravenswood.

The company also projected an exploration and development investment of USD 25 million in FY 2020.

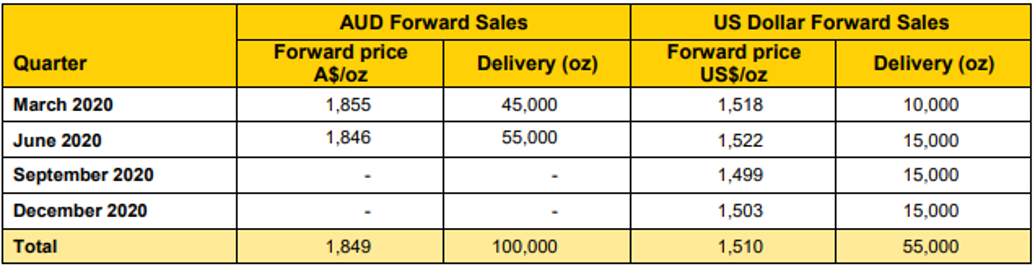

The current hedge book of the company is as below:

Source: Company’s Report

RSG is currently expanding its operational portfolio, and while the company decided to write-off Ravenswood off the books, it is acquiring various gold mine such as Mako gold mine and receiving some substantial results from exploration to expend its production ahead while running the cost low, which could be the problem solver for RSG ahead.

The stock of the company last traded at $1.190 (as on 17 January 2020 5:14 PM AEDT), up by 0.84 per cent against its previous close on ASX.