Last year was a very challenging period for financial services providers in Australia. Following the rigorous investigation by the Royal Commission, various leading banks of Australia were called out for failing to meet customer expectations and, in some cases, breaching their trust.

The revelations made by Royal Commission negatively impacted the performances of various banks. The observation and recommendations of Royal Commission highlighted the fact that there is something wrong with the Banks and they need to be governed properly.

Following the release of the Royal commission report, many banks have time and again reiterated that they are putting in policing and provisions to gain back the trust of the customers and to work in line with regulators.

NAB under Money Laundering Trap

One of Australiaâs leading banks National Australia Bank (ASX: NAB) has released its 2019 Annual financial report today, wherein the group has reported that it may be involved in a breach or alleged breach of laws governing bribery, corruption and financial crime.

NAB has confirmed that supervision, regulation and enforcement regarding antibribery and corruption, anti-money laundering (AML) and counter-terrorism financing (CTF) laws and trade sanctions has increased.

NAB has reported a number of compliance breaches to relevant regulators and has responded to a number of requests from regulators requiring the production of documents and information.

Other issues identified by NAB include:

- Certain weaknesses with the implementation of âKnow Your Customerâ requirements

- other financial crime risks

- Systems and process issues that impacted transaction monitoring

NAB continues to keep AUSTRAC (Australian Transaction Reports and Analysis Centre) informed of its progress in resolving issues, and intends to continue to cooperate with, and respond to queries from the regulators. NAB believes that it may find further issues in the coming future.

Last year in June, at the request of APRA, NAB undertook a Self-Assessment into governance, accountability and culture to identifed shortcomings in aspects of the Group's approach to non-financial risk management, with particular focus on operational, compliance and conduct risk. NAB identified 26 actions to deliver structural, procedural and cultural change.

Later, when NAB was called out by Royal commission for breaching the trust of its customers, it led to NAB outgoing Chairman and former Group CEO resigning.

In its 2019 Annual financial Report, NAB has assured that it is addressing the issues of the past and preparing the bank for the future and has taken clear actions designed to ensure that it meet customer and community expectations.

Precautionary and corrective measures taken by NAB

- NAB has strengthened its financial settings;

- It has increased customer-related remediation provisions;

- It has lowered its dividend payout, by 16% from financial year 2018;

- Nab has also raised a significant amount of capital to ensure that it is on track to meet APRAâs âUnquestionably Strongâ requirements for 1 January next year;

- A comprehensive program of work is well underway to improve non-financial risk management at NAB;

- Nab has started an extensive and considered reform program to achieve cultural and risk transformation, arising out of the Self-Assessment and sitting alongside the Royal Commission response;

- Intensive effort is underway to continue to overhaul processes and practices, but it is early days and there is more work to be done to achieve sustainable change.

NAB Chairman Commented:

âWe are making things right where we have made mistakes. We have improved processes to remediate customers fairly, consistently and more quickly, with a dedicated remediation team of more than 950 people driving this workâ

NABâs transformation, which has been underway for over two years, is delivering real benefits in terms of productivity and supporting business growth in a challenging, low-rate environment. It is also improving the resilience of NABâs technology and enabling it to adapt to a new digital future. NABâs focus on becoming simpler, faster and less complex for customers and employees has resulted in 30% fewer products, 30% fewer over the counter transactions and a 17% decrease in calls to its call centres.

Although NAB trying to make this right and is taking several precautionary and corrective measures to improve the situation, the risk of significant penalties by regulators still prevail.

NAB in its report has informed that Australian Securities and Investments Commission (ASIC) could bring more proceedings against NAB regarding other matters referred to it by the Royal Commission. And as a consequence of this, civil or criminal penalties could be imposed on the Bank.

FY19 Financial Performance

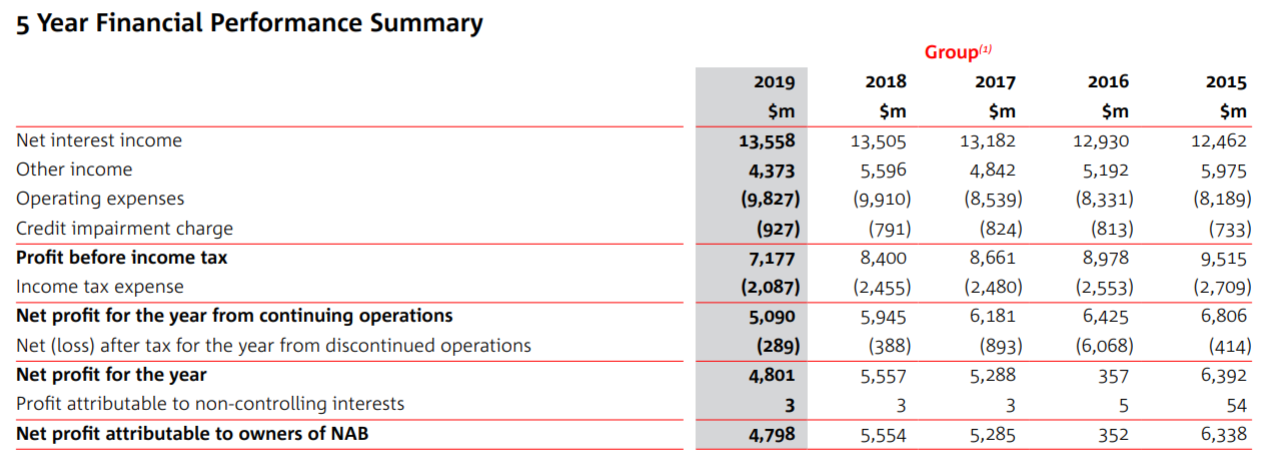

For FY19, NAB earned Net profit attributable to owners of $4,798 million which is lower than the net profits of the last two years (refer below image).

FY19 highlights

- During FY19, the NABâs cash earnings decreased by 10.6% to $5,097 million, as compared to prior year;

- the bank reported a total dividend of 166 cents per share, down by 16.2% on pcp;

- Credit impairment charges increased 18% to $919 million, and as a percentage of gross loans and acceptances rose 2bps to 15bps;

- Excluding customer-related remediation, revenue rose 1.1% mainly reflecting growth in business lending partly offset by lower margins;

- Net Interest Margin (NIM) declined 7 basis points (bps) to 1.78%;

- Group Common Equity Tier 1 (CET1) ratio of 10.38%, up 18bps from September 2018.

NAB Stock Performance

Despite facing several challenges over last year, NAB stock price has increased by 16.17% in last one year. At market close on 15 November 2019, NAB stock was trading at a price of $27.640, down by 0.576% intraday, with a market cap of $80.15 billion and outstanding shares of 2.88 million. The stock is trading at a PE multiple of 16.210x with an annual dividend yield of 5.97%. NAB has a 52 weeks high price of $30- and 52-weeks low price of $22.520 with an average volume of 6,194,633.

Bottom Line

Financial institutions like banks are highly regulated and are subject to various regulatory regimes, due to which, ensuring compliance with all applicable laws is very difficult. However, it is very necessary for bank to ensure that it is complying with each and every law so that the interest of its customers could be safeguarded. This is a reason why Governance is important for banks.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.