For many investors, the main aim of investing in the stock market is to make spectacular returns. Finding such companies is difficult but certainly not impossible. Once identified, they can generate significant returns over a long time. As we all know, the outbreak of COVID-19 impacted several sectors. It can be said that New Zealanders rely on primary industries when there are global uncertainties. This company enjoys a debt-free position, and this can help it to achieve decent growth moving forward.

The a2 Milk Company Limited

Summary

- ATM has witnessed a significant improvement in the performance between FY 2015 - FY 2019.

- The company has generated attractive growth opportunities by expanding into new geographies.

- ATM is a debt-free company and is possessing a robust balance sheet.

Stellar Growth in Diluted EPS

Over FY 2015- FY 2019, the company moved from a loss-making company with low market capitalization into a company with the top 10 market capitalization and has become part of S&P/NZX10 Index. This stock has delivered a return of ~63.97% in the span of 9 months. Such remarkable performance has attracted the attention of investors.

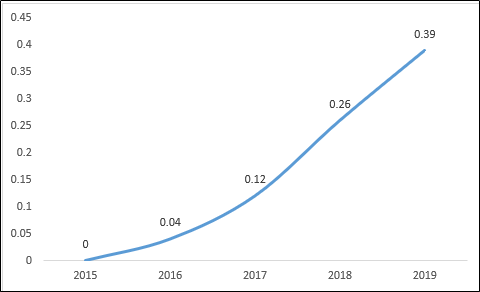

A key metric investors need to track is EPS. It gives an overall picture as to how the company has performed. The below given image provides an idea as to how ATM’s EPS has changed over time:

Diluted EPS (Including Extraordinary Items) (Source: EODHD/Others (Thomson Reuters))

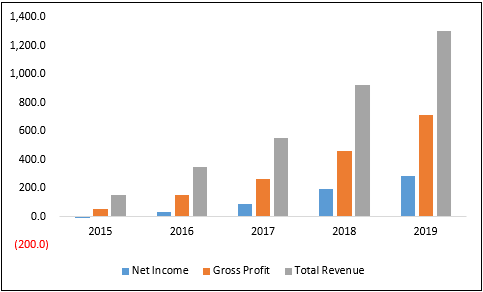

Let us have a look at the past financial performance of the company. Over FY15 to FY19, the company has grown its total revenue from NZ$154.8 million to NZ$1,304.3 million. During the same period, its gross profit rose from NZ$54.4 million to NZ$713.8 million.

Financial Performance (Source: EODHD/Others (Thomson Reuters))

The company registered CAGR of 70.37 percent over the period of FY15 to FY19 in the top line and, during the same time, it registered a CAGR of 90.32 percent in the gross profit. The growth witnessed reflects the company’s ability to sail through different market scenarios. In FY 2019 annual report, the company stated that its infant nutrition market share has been strengthened to 6.4% in China.

ATM Increases Stake in Synlait Milk Limited

ATM has increased its stake in Synlait Milk Limited. It has acquired shares at a market price of NZ$4.95 per share, which is below the company’s average entry price for the interest in Synlait. This increases its interest in Synlait from 17.4 percent to 19.84 percent.

Because of the decline in Synlait’s share price, the company saw it as an opportunity to complete strategic holding. The company has no plans of increasing its stake in Synlait Milk beyond 19.9%.

The a2 Milk™ Brand Expands into Canadian Market

ATM has entered into an exclusive licensing agreement with Agrifoods Cooperative with respect to production, distribution, sale, as well as marketing of a2 Milk™ branded liquid milk for Canadian market.

This agreement will give the company a capability to leverage the brand development work it has already undertaken in North America and grow into the Canadian market with the well-recognized partner.

The company would be providing Agrifoods with access to IP and marketing assets as well as the proprietary systems and know-how with respect to the processing and sourcing of a2 Milk™ and would work with Agrifoods along with local Canadian dairy farmers in order to source milk locally.

Agrifoods would be leveraging its significant resources in-market to create distribution throughout Canada and has a primary task for financing this venture. It is estimated that a variety of liquid milk products will be introduced later this calendar year.

Sitting on a Pile of Cash

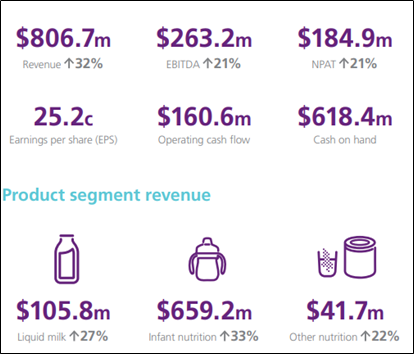

In addition to decent performance, the company is also sitting on a pile of cash. At the end of the first half (ended December 31, 2019), the company had $618.4 million in cash. Notably, the cash balance implies growth in revenue as well as earnings, partially offset by higher working capital.

It is also a debt-free company that can help it in achieving long-term growth objectives.

Total Revenue Rose 31.6%

For the half-year ended 31 December 2019, the company reported total revenue of $806.7 million, an improvement of 31.6%. EBITDA also increased by 20.5% to $263.2 million. The company stated that its overall result implies continued growth in the infant nutrition segment, with sales coming at $659.2 million. This reflects a rise of 33.1 percent on pcp.

In-line with the strategy, there was a robust growth in China label infant nutrition products, with sales amounting to $146.7 million. This reflects a rise of 100%.

Group Performance (Source: Company Reports)

ATM Remains Uncertain About Future

The outlook for both revenue and earnings is uncertain due to the current COVID-19 pandemic. Also, there is still uncertainty around the potential impact on consumer demand and supply chains in core markets and the resulting financial impact on performance.

However, the company expects revenue for FY20 in the range of $1,700 million to $1,750 million. Full-year EBITDA margin is now expected to be above that was provided in February and in the range of 31% to 32%.

Key Points to Ponder Over

The company’s business is exposed to short-term as well as long-term climate and environment related risks. Notably, these risks are inherent in dairy industry as well as consumer marketplace.

The company has experienced significant growth in recent years, driven mainly by the success of liquid milk and infant formula businesses in Australia, China, and the US. As a result, it is exposed to increasing competitive intensity, which could lead to an erosion of market share positions in core markets.

On August 14, 2020, The a2 Milk Company ended the session at NZ$20.950 per share which implies an increase of 0.87% on an intraday basis.