Overall global trends indicate low interest environment and future expected cuts in several economies across the world, in order to beat global growth concerns and meet domestic macro-economic objectives of stable inflation, decent employment levels and strong GDP growth rate.

Australian Reserve Bank recently undertook two consecutive rate cuts, with the current interest rate now standing at 1%. Market analysts are expecting another rate this year. The Reserve Bank of India is also expected to cut interest rates by 40 bps by the end of this fiscal year. Market analysts are also projecting European Central Bank to slash interest rates next week. In its next meeting in another two weeks, US Fed is also expected to reduce interest rates by a quarter point.

Amidst low interest rate regime, investors are flocking to safe haven assets such as gold and also equity markets for dividends and capital appreciation.

After the close of trading hours on the Australian Securities Exchange on 6 September 2019, the S&P/ASX 200 closed higher at 6647.3, up by 34.1 basis points or 0.51 per cent, relative to its last close.

Some of the drivers of this uptrend, or the gainers for the day included Speedcast International Limited (ASX: SDA), which was up by 9.61 per cent and quoted A$1.25, followed by Cooper Energy Limited (ASX:COE), which increased by 5.98 per cent and quoted A$0.62 and AMP Limited (ASX:AMP), which was up by 5.12 per cent, and quoted A$1.74.

The declines of the day included Pro Medicus Limited (ASX:PME), which plunged by 12.09 per cent and quoted A$33.38, followed by Charter Hall Group (ASX:CHC), down by 5.70 per cent at A$12.08 and Saracen Mineral Holdings Limited (ASX:SAR), which was down by 5.07 per cent, and quoted A$3.56 at the end of the dayâs trade session.

An Overview of Interest Rates

Interest rates and investments are highly related, and the understanding of their correlation is the key in breaking down strategies in the investing and business world. This is the reason that the investment community, economists and analysts as well as media players are always obsessing over the prevailing interest rates in the economy. In this article, we would understand the stance of investing in a low-interest rate scenario. Letâs dive in, brushing in some basics:

Simply put, the interest rate can be synonymous for a rental charge or a leasing charge. It refers to that amount which a lender charges for the use of assets, which could be in the form of goods, cash or assets, that he would have offered to a borrower. The interest rate is expressed as a percentage of the principal value, and is ideally noted on an annual basis, which is referred to as the annual percentage rate.

Factors That Influence Interest Rates

Interest rates are one of the key monetary policy instruments for the Reserve Bank of any economy. The rate of interest is purely determined by the laws of supply and demand. In economies with high loan demand, lending institutions increase the rate of interest. On the other hand, when banks and other institutions witness a slow loan demand, interest rates are typically lowered. Another key factor in the central bank monitoring interest rates is the progress on nationâs economic indicators (including inflation, employment, GDP, Balance of Payments, etc).

Application of Interest Rates

Interest rates are applicable in almost every lending or borrowing transactions. In an ideal scenario, an individual borrows money in order to buy amenities like house and vehicles, pay for education or commence a business. Businesses, on the other hand, borrow money to fund their capital, purchase assets like land, machinery and buildings.

The money which is due to be repaid is tagged along with an interest rate, and is usually more than the borrowed amount, as the lender would require a certain amount compensation for the loss of use of the money during the loan period, that is, when the particular amenity was with the borrower. In this period, the lender could have invested the funds rather than provide a loan, which would have in turn reaped income off the asset.

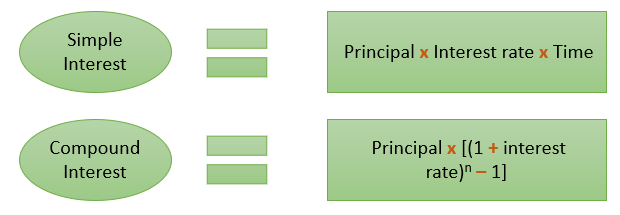

Below are the two calculations pertaining to interest rates:

Please note that in the above calculation, n= the total number of compounding periods.

Effect of Interest Rates on the Market

The rise and decline of the interest rates have an impact on both the consumer and business psychology. Once the rate is changed by the concerned governing authority, a ripple effect (which refers to a multiplier in terms of macroeconomics) spreads across the entire economy. This effect leaves its marks on the overall business environment, stock and bond market as well as overall economy.

The lower the interest rate, the more willing people are to borrow money in order to carry out purchases, as they have more money that is saved by paying lesser interest and leads to increased consumer spending behaviour. Consequently, there is an upsurge in output and productivity. On the other hand, higher interest rates mean that consumers are in a dearth of disposable income and cannot afford to spend lavishly. The lending institutions tend to make scarcer loans in a situation where interest rates are coupled with increased lending standards. Therefore, consumers are bound to cut down on their spending.

Low Interest Rate Scenario

A low interest rate environment occurs when the rate of interest set by the central bank is lower than the historic average for a long phase. In an ideal scenario, central banks or the economyâs governing bodies shun down the interest rates in order to tackle inflation scenario, low unemployment and boost the overall economic growth.

However, just like every aspect of the dynamic business world has its share of pros and cons, a low interest environment, if prolonged for a long period of time adversely impacts investments, which means that- anyone on the higher side of savings in bank accounts would not reap good returns in this phase, as the bank deposits drop. This leads to a phenomenon of cheaper borrowing costs, loss of bank profitability, a decrease in interest income, increase in the amount of debt. All these would cause a challenge once the interest rates are on a verge on increasing.

Millennials Versus Boomers Amid Low Interest Rates

As understood, the lower interest rates encourage additional investment spending and is a boon phase for the borrower, while lenders end up receiving lower returns. A section of market experts believe that the low interest rates are good for millennials, as they tend to borrow more, driven by the ideologies of student debt and likewise events. Older people, on the flip side, are the ideal savers, especially those nearing retirement and are advised to gradually shift their investments towards less risky assets.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.