.jpg)

Source: H_Ko, Shutterstock

Summary

- Direct Line Insurance Group PLC had delivered a growth of 2.2% in Direct own brands in-force policies during FY20.

- The operating profit had declined by 4.5% during FY20.

- DLG had declared a final dividend of 14.7 pence per share attributable to FY20.

- DLG had delivered the combined operating ratio of 91.0% during FY20.

Direct Line Insurance Group PLC (LON:DLG) is the LSE listed financials stock. DLG’s shares have generated a return of approximately negative 0.61% in the last 12 months. It is listed on the FTSE 250 Index. The Company was incorporated in 1988.

Business Model

Direct Line Insurance Group PLC is a UK-based Company, which is the general insurer for small businesses. Overall, the Company has four reportable business segments –

- Motor

- Home

- Commercial

- Rescue & Other Personal Lines

(Source: Company website)

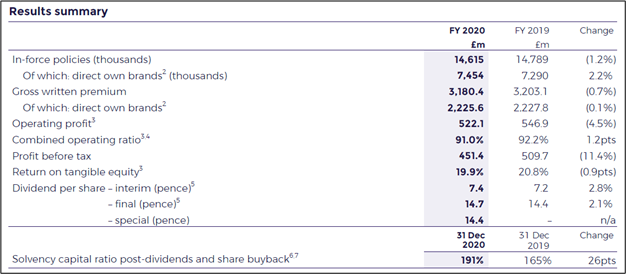

FY20 Financial Highlights (for the period ended on 31 December 2020, as of 08 March 2021)

(Source: Company result)

- DLG had delivered a growth of 2.2% in Direct own brands in-force policies from 7,290 thousand during FY19 to 7,454 thousand for FY20 driven by strong performance witnessed across Home, Commercial and Rescue segment. The Motor segment remained highly stable during the period.

- On the flip side, the total in-force policies had demonstrated a 1.2% decline due to reduced travel volumes and lower partnerships.

- Moreover, the operating profit got slightly reduced by 4.5% to £522.1 million during FY20 due to the increased significant weather cost of £43.0 million incurred during the period.

- Furthermore, DLG had delivered the combined operating ratio of 91.0% during FY20, while it was 92.2% during FY19. The profit before tax was £451.4 million during FY20.

- The Company had declared a final dividend of 14.7 pence per share during FY20, an increase of 2.1% from the levels of dividend declared during FY19.

- DLG had plans of buying back shares up to £100 million.

FY20 Divisional Highlights

- The Motor segment had delivered an operating profit of £363.5 million and a combined operating ratio of 87.7% during FY20, driven by the reduced claim frequency because of the Covid-19 pandemic. Moreover, DLG had launched the “Mileage Moneyback” initiative for all Direct Line customers.

- The Home division had delivered an operating profit of £101.4 million and a combined operating ratio of 87.1% during FY20. The reduction in FY20 operating profit was due to £27.0 million incurred as significant weather costs and reduced prior-year release of reserves.

- The “Rescue and other personal segments” division comprises Green Flag and other personal lines product such as Pet, Travel, Creditor and the UK Select. The operating profit of this division grew by £6.0 million to £51.2 million during FY20 due to the robust business performance of Green Flag.

- The Commercial business division had achieved an operating profit of £50.4 million and a combined operating ratio of 95.5% during FY20.

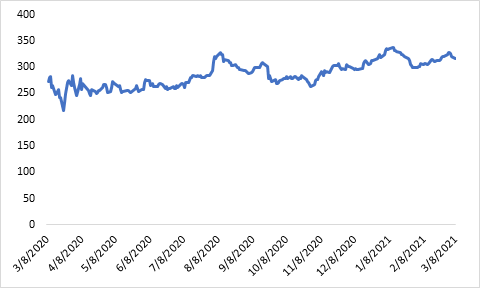

Share Price Performance Analysis of Direct Line Insurance Group PLC

(Source: EODHD/Others, chart created by Kalkine group)

DLG’s shares were trading at GBX 314.50 and were down by close to 1.84% against the previous closing price as of 08 March 2021 (before the market close at 11:01 AM GMT). DLG's 52-week Low and High were GBX 215.83 and GBX 342.10, respectively. Direct Line Insurance Group PLC had a market capitalization of around £4.37 billion.

Business Outlook

DLG had delivered significant business performance during FY20 driven by increasing digital penetration and achieved operational excellence through technological advancement. Moreover, the Company would aim to provide a substantial improvement in the customer efficiency aspect and achieve an operating expense ratio of 20% by 2023. Furthermore, DLG had anticipated generating benefit from counter-fraud initiatives and pricing sophistication. The Group had expected to achieve the target of a 15% return on tangible equity per annum. Also, DLG had anticipated a combined operating ratio ranging from 93% to 95% during 2021.

The Company had raised concerns regarding ongoing uncertainty related to the Covid-19 pandemic and implementation of FCA pricing practices. Overall, the Company is well-positioned to accelerate the progress of the growth trajectory through technological developments and a resilient business model.