US Markets: Major Wall Street stock indices slipped into the negative territory in the wee hours of trading on Tuesday, 23 November, with the technology stocks heavy Nasdaq Composite falling more than 1%. Dow Industrials traded flat, while S&P 500 dropped well below the psychological level of 4,700, making an intraday bottom of 4,652.66. In the session so far, the Dow Jones Industrial Average has oscillated between a high and low of 35,762.35 and 35,542.87, respectively.

Extending the losses after briefly touching an all-time high in the previous session, Nasdaq Composite made an intraday bottom of 15,603.30, down 250 points from the previous close as rising Treasury yields disturbed technology heavyweights. Shares of Zoom Video Communications crashed a little more than 19% after the California-headquartered teleconferencing major indicated a possibility of lower revenues.

The stock of Zoom Video Communications has been continuously falling since Tuesday last week. With today’s major correction in the market prices, the shares stand with a one-week loss of nearly 25%.

The lower-than-expected value of Services PMI for the month of November also discouraged the investors, at a time when resurgence of Covid cases across many countries in the Europe have forced the local governments to re-impose national lockdowns, effectively forcing all the consumer-facing settings to either shut, or operate in a curtailed manner.

According to the preliminary estimates by IHS Markit, the US Services PMI declined to 57 in November of 2021, sharply below the street expectations of 59 and well below the October’s reading of 58.7.

The relaxations allowed by the Washington administration has helped the businesses to alleviate the fears, while rising international, as well as domestic travel continues to support the ailing aviation and hospitality industry. Even with the lower value of Services PMU, the services sector in the US has expanded at a sharp scale in the present month so far.

The ongoing challenges including the short-staffed operations, malfunctioned supply chains and inadequacy of businesses in hiring the skilled workforce has weighed on the comprehensive growth. As a result of this, a large section of enterprises are not able to function with the maximum possible capacity, while input cost inflation hovers at a six-month high.

Meanwhile, a marginal improvement in the Manufacturing PMI reading in November partly favoured the mood of investors as it recovered to 59.1 from a 10-month low of 58.4 in October. However, the industry-wide supply side troubles, delays in the order of raw materials and dearth of human capital at the manufacturing units continued to deteriorate the performance of many businesses.

The Dow Jones Industrial Average added 52.35 points, or 0.15% to 35,676.24, the tech leader Nasdaq Composite shed 152.02 points, or 0.96% to 15,702.28, while the broader share indicator S&P 500 declined 8.47 points, or 0.18% to 4,674.47, after recovering marginally from the day’s bottom.

US Market News: Shares of Travelers Companies, JPMorgan Chase, Merck & Co, Goldman Sachs, UnitedHealth Group, Chevron, Verizon, Visa and Amgen rose up to 3%, contributing the major positive points to the Dow Industrials. While, on the other hand, the stocks of Salesforce, Walt Disney, Nike, Microsoft, American Express, Home Depot, Intel and Honeywell International effectively counterbalanced the positive points as these shares cracked 1-3%.

Amid the Nasdaq Components, shares of Peloton Interactive, CrowdStrike Holdings, Atlassian Corporation, Okta, Tesla, Dexcom, Advanced Micro Devices, eBay, Monster Beverage, Auto Desk, Adobe Systems, Illumina, Moderna, ASML, DocuSign, NXP Semiconductors, MercadoLibre, Analog Devices, Synopsys, Xilinx, Nvidia, Microsoft, Honeywell International, Cognizant Technology, Facebook, Intel and Qualcomm crashed 1-6%, dragging the market index into negative region.

A 1-7% uptick in shares of Pinduoduo, Ross Stores, Dollar Tree, JD.com, Baidu, Electronic Arts, Starbucks, Kraft Heinz, Comcast, Charter Communication, Amgen and Microchip Technology managed to offset the losses.

UK Markets: London equities ended on a flat note with the domestic benchmark FTSE 100 finishing flat at 7,266.69, staging a marginal comeback in the terminal deals on Tuesday. On the other hand, the mid-cap indicator FTSE 250 ended 200 points lower as the market index failed to resume the trade in the positive territory.

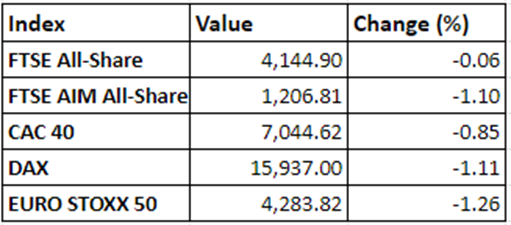

European equities are thoroughly affected due to the recent resurgence in the number of infections with the Austrian administration announcing a 10-day nation-wide lockdown. Investors are categorically concerned about the efforts by respective healthcare administrations as they are unable to contain the spread of virus even after maximising the number of immunised population.

FTSE 100 gained 11.23 points, or 0.15% to end at 7,266.69, while the mid-cap heavy FTSE 250 lost 208.09 points, or 0.89% to terminate at 23,221.61.

FTSE 100 (1-year performance)

Source: EODHD/Others

Market Snapshot

Top 3 volume leaders: Lloyds Banking Group, Vodafone Group and Glencore

Top 3 sectoral indices: Consumer Services, Construction and Industrial Metals

Bottom 3 sectoral indices: Automotive, Industrial Engineering and Electronic & Electrical Equipment

Crude oil prices: Brent crude up 3.31% at $82.34/barrel; US WTI crude up 2.50% at $78.67/barrel

Gold prices: An ounce of gold traded at $1,784.55, down 1.20%

Exchange rate: GBP vs USD - 1.3377, down 0.14% | GBP vs EUR - 1.1884, down 0.30%

Bond yields: US 10-Year Treasury yield - 1.665% | UK 10-Year Government Bond yield - 0.9970%

Markets @ 16:30 GMT