The increasing importance of connectivity is a worldwide trend and a number of ongoing trends in telecommunication markets in Australia reflect developments that are also occurring internationally. As a consequence of the unique structural characteristics of the telecom industry, Australian consumers pay a significant pay premium. Let have a look at 2 telecom stocks 5GN and VOC with their recent updates.

Vocus Group Limited (ASX:VOC)

Vocus Group Limited (ASX: VOC) is a telecommunications services provider, which operates in the New Zealand and Australian markets. The company was officially listed on ASX in 1999. Recently, the company released a Presentation Briefing highlighting its strategies and financial performance. The company primarily operates with three independent businesses: (1) Vocus Network Services; (2) Vocus Retail; (3) Vocus NZ. The Vocus Network Services is a leading provider of fibre and network solutions, wherein it targets wholesale and enterprise markets, as well as federal, state and local government. It has network assets with 17 owned data centres, more than 5500 on-net buildings and around 25,000km of fibre. In terms of Vocus Retail, it is a reseller of broadband, mobile, voice and energy, with price sensitive consumers and is targeting small to medium enterprises. Vocus NZ offers the full suite of fibre connectivity, broadband, voice, energy and mobile. The targeted markets for Vocus NZ are consumer, government, enterprise and wholesale. Vocus NZ has network assets with 4,200km of inter capital fibre and three owned data centres.

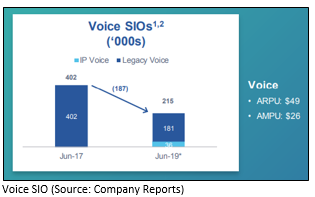

Importantly, Voice Retail is more than halfway through navigating the structural headwinds in voice and broadband. The business faced material margin dilution due to loss of legacy voice and copper ADSL SIOs, together with the migration to lower margin NBN products. However, it expects the impact of erosion to be fully offset by new revenue streams and cost savings during H2 FY21.

The reasons why customer choose Vocus are: A, the company has its customer covered with dedicated local account management with 24/7 local network operational centres; B, It is trusted by leading brands and government agencies with security-cleared staff operating to secure network, as the company has separate and secure network for government customers, among others. It has a 35% market opportunity in state government and 65% market opportunity in the federal government, collectively representing a total addressable government market of around $600 million. The company has a specialised network to grow government share and has existing contracts with major Federal Government customers, with partitionable network and management systems.

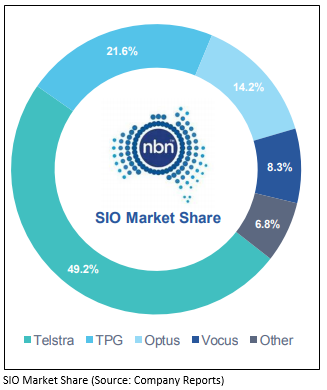

Furthermore, the company invests in its people and channel and partnership, with an action plan to enhance relevant industry experience, build capability to offer partner-billed services and digitise all Vocus processes. The company has upskill to match the growth ambition, single sales and account management methodology and technical sales capability to support new products. It is a 4th leading NBN provider, with the majority of customers on unlimited plans and 8.3% share in SIO market.

Vocus New Zealand witnessed a consistent and sustained revenue growth over the past five years from core telco and energy bundles and has delivered incremental EBITDA, while consolidating merged companies and investing for growth. Vocus NZ posted revenues and EBITDA of $188 million and $30.6 million, respectively in 1H FY19. It has significant opportunities to increase broadband and energy bundles, along with mobile to reduce churn and increase customer lifetime value.

Previously, in another update, the company informed the market that AGL Energy has secured access to Conduct Due Diligence on VOC.

Leading Fibre Assets: The fibre and core transport network are the companyâs key assets, connecting Australia with Asia. It has 15,020km of the inter-capital network in Australia, over 9,500km of metropolitan and regional fibre in all major centres and 4,200km of the inter-capital network in New Zealand. Australia Singapore Cable gateway to Asia is a great example of the companyâs leading fibre assets alo.ng with North West Cable System connecting offshore oil and gas facilities.

The gross margin, EBITDA margin and net margin of the company amounted to 40.9%, 17.7% and 1.7% in 1H FY19 against the industry median of 61.2%, 32.6% and 8.7%, respectively. The liquidity position (current ratio) for the period stood at 0.79x in 1H FY19 against the industry median of 0.92x. The asset to equity ratio was at 1.80x for the period as compared to the industry median of 3.01x. The return on equity stood at 2.0% against the industry median of 7.9%.

Guidance: For FY 2019, the company expects underlying EBITDA to be in the range of $350 million to $370 million. The cash conversion excluding ASC to be in the vicinity of 90% to 95% and remains unchanged for the fiscal year 2020, with the net leverage ratio to be 2.90x to 2.95x for the period. For FY 2020, the company is projecting no change in the underlying EBITDA from FY19 guidance and capital expenditures to in the ambit of $200 million to $210 million. The company estimates EBITDA growth for Vocus Network Services to be in the ambit of $20 million to 30 million, offset by a similar decline in Vocus Retail. For FY 2021 and beyond, the company expects that the Vocus Network Services will accelerate EBITDA growth, with a retail business to stabilise during H2 FY21 and prime for growth in FY22.

Stock Performance: At the time of writing on 4th July 2019 (AEST 12:45 PM), the stock of VOC is trading at a price of $3.190 per share, down 0.312%, with a market capitalisation of $1.99 billion. The stock has produced returns of -29.36%, -11.11% and 0.63% for the one month, three months and six month period, respectively.

5G Networks Limited (ASX:5GN)

5G Networks Limited (ASX: 5GN) is a supplier of cloud-based solutions, network and managed services. The company was officially listed on ASX in 2017. Recently, the company, via a release dated 23rd May 2019, informed the market about CBA bank facility. The company further stated that it has increased its debt facility to $7.2 million with the Commonwealth Bank of Australia. In addition, the company continued to implement its strategy on the back of the increased facility and a recent capital raise of $8 million. Furthermore, it will also continue to pursue accretive acquisitions in key areas, such as AWS partners and software development companies, data centre facilities and managed service providers.

1H FY19 Results: The company published its half yearly presentation, reporting its operational and financial performance for the first half of the financial year 2019. The company witnessed strong organic growth of 112% in its data network services as compared to 2H FY18. The annuity-based service agreements protected around 70% of the product revenues. The companyâs multi-product sales proposition has driven several contract wins, including both upsell and new customers. The revenue comprises five months of Hostworks and Anittel acquisition. 5GNâs focus remains on network services growth, including leveraging of owned fibre and wireless infrastructure.

In terms of cash position, the company reported decent numbers to help 5GN move forward. 5GN reported a growth of 62% in cash receipts from the previous quarter to $23 million, with H1 normalised net operating cash flow of $1.4 million and $1.7 million payment for the Annitel/Hostworks acquisition for H1 FY19. The company adopted new accounting standards, including capitalisation of lease liabilities. 5GNâs network expansion will support direct customer demand while reducing reliance on third-party fibre.

The integration, cross-sell and up-sell for customer revenue growth and acquisitions are the three important levers of the company to grow its shareholder value. In terms of integration, the company has optimised the operational efficiencies by successfully integrating people, platforms, business systems and processes and has ironed out outdated systems and functions to avoid duplication or obsolescence costs. With respect to cross-sell and up-sell for customer revenue growth, it harvests acquired customers, which typically have only single product holdings, with targeted network infrastructure investment to high-density customer locations. On the acquisition front, the company has a disciplined approach to ensure that the underlying financial value is defined.

Previously, the company also announced a rollout of Nationwide High-Speed Managed Data Network.

Change in Substantial Holding: The company recently announced that JD Management Group Pty Ltd, JMD Superannuation Fund, Studio Incorporate Pty Ltd and Joseph Demase have changed their interest in the company with 25.46% voting power compared to the previous voting power of 31.62% on 26th April 2019. In another notice, the company highlighted that Eckert Investments Pty Ltd, MIH Investments Pty Ltd and Mark Eckert ceased to be substantial holders of the company since 8th April 2019.

Outlook: The market sentiment for progressing merger and acquisition opportunities remains positive and attractively priced in 2019. The company expects revenue and EBITDA growth to accelerate in 2H FY19. Additionally, future capital investment will be funded through operating cash flows. 5GNâs improved operating efficiencies by rationalisation of systems will continue cost reductions in 2H FY19. The company projects its EBITDA margins to revert back to >7% in 2H FY19.

Stock Performance: At the time of writing on 4th July 2019 (AEST 12:51 PM), the stock of 5GN is trading at a price of $1.545 per share, down 1.905%, with a market capitalisation of $100.01 million. The stock has produced returns of 31.80%, 67.55% and 250% for the one month, three months and six month period, respectively.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.