Summary

- Appen and Austal playing critical roles in the tech sector and the nation’s sovereign shipbuilding capability, respectively

- AI performance relies on large volumes of training data and regular data updates. With AI spend growing at 28%, there is strong market opportunity for Appen, engaged in delivering essential training data for AI development and maintenance

- Austal upgraded FY2020 earnings guidance, backed by continued strong business performance and recent win of a new vessel construction contract from the Royal Australian Navy

Several businesses are facing critical times amid the COVID-19 pandemic; however, there are few businesses that experience negligible impact due to the nature of their operations, deemed as essential functions/services. On that front, in this article, we are discussing two ASX-listed players - Appen and Austal.

Austal introduced a range of measures to keep construction and maintenance of vessels ongoing, which also helped the Company to keep its people employed. The Company continues its shipbuilding and sustainment operations across the United States, Australia, Philippines, and Vietnam.

A coronavirus outbreak-led boost in the use of e-commerce, search, and social media platforms is aiding performance of Appen. The Company is making investments towards strengthening its position in the rapidly developing and exciting fields of machine learning and artificial intelligence.

Interesting Read: Will Artificial Intelligence Barge Higher in Post-Pandemic Era?

Let us discuss these businesses and their recent market updates in details.

Austal Limited (ASX:ASB)

Austal Limited (ASX:ASB) is Australia's global shipbuilder, maritime technology partner and defence prime contractor of choice. ASB is engaged in design and build of revolutionary vessels for the defence and commercial sectors. The Company is Australia’s largest defence exporter and the world’s largest aluminium shipbuilder.

FY2020 Earnings Guidance Upgraded: On 29 May 2020, ASB announced to have increased its earnings guidance for FY2020 to group revenue of ~ $2 billion and group EBIT of at least $125 million. Previously, the Company had rolled out FY20 guidance of group revenue of $1.9 billion and group EBIT of minimum $110 million.

ASB attributed its improved forecast performance for FY2020 to various factors including strong performance across its shipyards in the US, Australia, Philippines and Vietnam, and recognition of R&D tax credits in the US. ASB also experienced a limited impact of coronavirus on its performance than expected in April 2020 and May 2020.

Another factor that contributed towards the guidance upgrade was the award of a $324 million contract in early May, under which Austal would design and build 6 evolved CCPBs (Cape-class Patrol Boats) at its Henderson shipyard in Western Australia. In its 30 years of operations, this is the biggest construction contract for an Australian vessel.

The vessels would be an addition to the Royal Australian Navy’s fleet of two CCPB’s delivered in 2017, enhancing the nation’s ability to protect and secure its maritime borders. Moreover, the contract further expands Austal’s Cape-class Patrol Boat program to 18 vessels. The new contract ensures at least 700 jobs are maintained at Austal while engaging with thousands of suppliers.

Completion of Acceptance Trials in GoM: Recently, ASB announced acceptance trial completion for the future USS Oakland (LCS 24), the twelfth Independence-class Littoral Combat Ship built by the US segment of the Company for the US Navy.

During the lockdown period, the Company was able to complete the acceptance trials for high-speed, shallow-draft surface combatant, LCS 24, which shows the potential of Austal USA as well as its reliability to deliver vessels on time even during stressful situations. These vessels are designed to defeat increasing coastal threats and give access and control along coastal waters.

Acceptance trials involved the execution of several tests with the ship delivery due in June 2020.

Stock Information: By the market closure on 29 May 2020, ASB stock settled at $3.340, up 10.231% from the previous close. In the last one-month and six-month period, the stock has delivered a return of 8.44% and -20.48%, respectively.

Appen Limited (ASX: APX)

Appen Limited (ASX: APX) offers essential training data for AI development and maintenance. The Company is known for providing high-quality speech, natural language, image, video, and relevance data.

On 29 May 2020, Appen released its AGM presentation, highlighting below factors:

- High Growth Market

- Strong Performance

- Positioned to Win

High Growth Market: AI spending is increasing at 28%, according to IDC Worldwide Artificial Intelligence Systems Spending Guide, September 2019. This demonstrates huge opportunity for the Company to grow, as AI relies on large volumes of training data and regular data updates.

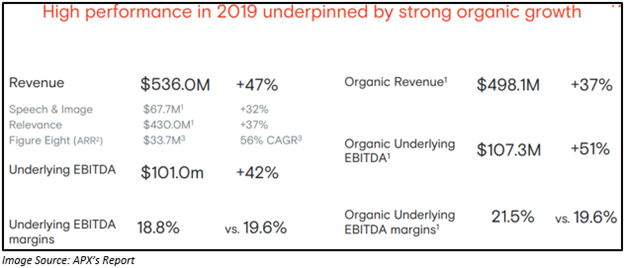

Strong Performance: The Company delivered a strong performance in 2019, supported by strong organic growth. For FY2019 ended 31 December 2019, Appen registered revenue of $536 million, up 47% on pcp, while organic revenue grew 37%.

Existing customers of the Company support revenue growth with improved demand for present as well as new projects. Appen has strong and enduring client relationships. The Company is also making a considerable investment in sales and marketing in FY2020 to lay a base for its future growth.

Growth Initiatives

Government: In the US, the known government AI budget is US$5 billion while in the UK it is £2.3 billion. In 2019, Appen won a US government customer. Government investment and setup on track with team and pipeline growing.

Sales and Marketing: The Company is making investments to secure new customers as well as diversify revenue. Appen is hiring sales teams with plans to cover sectors like tech, auto, and financial services. It is also preparing for geographic coverage such as North America, UK/Europe, Asia, and China.

China: In China, the Company is adding new customers and revenue, with focus on major technology companies and differentiated global offering.

COVID-19 Impact on Appen: During the COVID-19 pandemic, majority of the staff was operating from their home, except for secure work and in China. The people were ideally placed during the pandemic. There was negligible impact on customer delivery and support.

Appen noted resilient earnings and a strong balance sheet. Presently, the Company has a cash balance of over $100 million.

Outlook:

- APX continues investments in technology and customer growth and diversification, to strengthen its position in a high growth market.

- Based on the current data available with the Company, there is a negligible scope of pandemic impact.

- YTD revenue plus orders in hand for delivery in FY20 stood at ~$350 million at May 2020. FY2020 underlying EBITDA for the full year ending 31 December 2020 is expected between $125 million and $130 million, in line with the last guidance.

Stock Information: By the market closure on 29 May 2020, APX stock settled at $30.80, up 0.326% from the previous close. In the last one-month and six-month period, the stock has delivered a return of 27.33% and 25.77%, respectively.

Do Read: Investors Like Technology Disruptors on ASX: ALU and APX