Dividend Yield

The dividend yield of a company is the ratio of its annual dividend in comparison to the price of its share. Mathematically, dividend yield = annual dividend/share price. The dividend yield increases when the share price falls and vise versa.

Via dividend yield, the amount of cash is measured that an investor gets for each dollar he/she has invested on that particular stock. It can also be referred as the return on investment for stocks with no capital gains.

In this article, we would be discussing recent updates of six ASX-listed stocks with above average dividend yield.

Iress Limited

Iress Limited (ASX:IRE), a provider of IT solutions to financial market participants as well as wealth managers, has a dividend yield of 3.73%, as on 03 September 2019. The shares of IRE opened at a price of A$12.20, slightly below its previous closing price. By the end of the dayâs trading on 03 September 2019, the closing price of the stock was A$12.160, down by 1.379% as compared to its last closing price. Iress has a market cap of A$2.15 billion with approximately 174.75 million outstanding shares and a PE ratio of 33.870x.

1H19 Highlights

Recently, on 23 August 2019, IRE released its 1H 2019 for the half year ended 30 June 2019. The company reported a 5% increase in its group revenue on a constant currency basis and a 10% growth in segment profit as compared to the previous corresponding period. The growth in revenue was the outcome of underlying performance in Australia, the United Kingdom as well as South Africa. The revenue was also driven by the acquisition of international market data business QuantHouse. The decline in net profit after tax was attributed to the adoption of the new lease accounting standard AASB16, QuantHouseâs acquisition along with the increased share-based payments after the changes to the remuneration models in recent years. However, excluding the new leasing standard and QuantHouse, there was a 2% growth in NPAT.

The company declared an interim dividend of 16 cents per share. Its fundamentals remained strong during the period with cash conversion of 100%, recurring revenue of circa 90% and net debt balance of $193.3 million, which represents a conservative debt ratio of 1.3x segment profit.

Outlook

The company expects segment profit growth for 2019 to be in line with the guidance provided in February 2019. This also included new accounting standards and excluded QuantHouse.

Data#3 Limited

Data#3 Limited (ASX:DTL), a leading provider of technology services and solutions, has an annual dividend yield of 4.25%, as on 03 September 2019. The shares of DTL opened at a price of A$2.580, slightly above at a gap of A$0.060 from its previous closing price. By the end of the dayâs trading on 03 September 2019, the closing price of the stock was A$2.520. DTL has a market cap of A$388.02 million with approximately 153.97 million outstanding shares and a PE ratio of 21.430x.

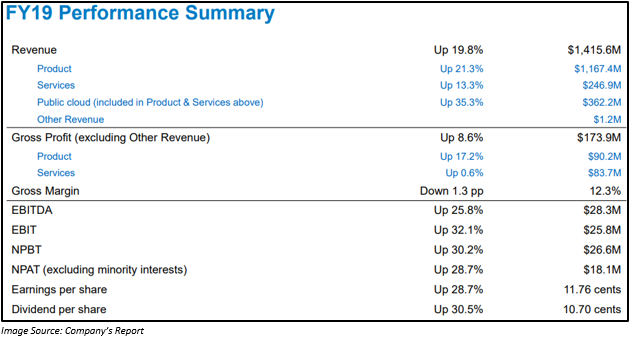

FY2019 Highlights

Recently, the company had represented its solid FY2019 results for the year ended 30 June 2019. Its revenue increased by 19.8% to $1.4 billion, with product revenue and services revenue increasing by 21.3% to $1,167.4 million and 13.3% to $246.9 million, respectively. The company also registered strong growth in public cloud revenues, which grew by 35.3% to $362.2 million during the period. NPAT after excluding minority interests increased by 28.7% to $18.1 million. The directors of the company declared a final fully franked dividend of 7.10 cents per share. Thus, the total dividend for FY2019 stands at 10.70 cents per share fully franked.

Outlook:

DTL based on the ongoing growth in the Australian IT market believes that it would be well placed to capitalise on the opportunities. Moreover, DTL would continue to build its strength as well as improve its shareholder value. The overall financial goal of the company is delivering sustainable earnings growth.

Recent Appointment:

DTL, on 30 August 2019, announced the appointment of Mark Esler to its board of directors. Mark Esler started his career at IBM in the year 1976 and played a number of roles before joining DTL in 1984 as an Executive Director. From 1997 to 2002, he served as the executive director and also played the senior management roles in sales and marketing, operations as well as supply chain before retiring from the position as Queensland General Manager in 2014.

Class Limited

Class Limited (ASX:CL1), which is engaged in providing cloud-based self-managed superannuation fund administration software solutions and services, has an annual dividend yield of 3.98%, as on 03 September 2019. The shares of CL1 opened at a price of A$1.265, at a gap up of A$0.010 from its previous closing price. By the end of the dayâs trading on 03 September 2019, the closing price of the stock was A$1.280, up by 1.992%% as compared to its last closing price. CL1 has a market cap of A$147.67 million with approximately 117.66 million outstanding shares and a PE ratio of 16.380x.

FY2019 Highlights

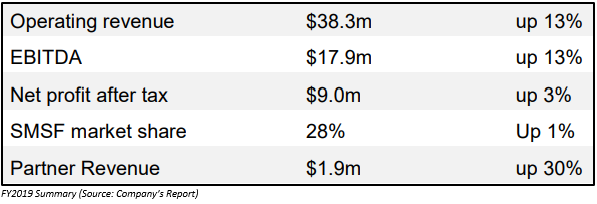

Class Limited, on 20 August 2019, reported a 13% increase in operating revenue to $38.3 million and a 13% growth in EBITDA to $17.9 million in its FY2019 results announcement. Growth in revenue was majorly driven by continued account boost as well as partner initiatives. The partner revenue increased by 30% to $1.9 million. CL1âs SMSF market share increased by 1% to 28%. CL1 declared a final dividend of 2.5 cents per share (fully franked).

The position of total accounts of the company including 171,447 Self Managed Super Funds (SMSFs) on the Class Super products stood at 179,082 accounts. Class Portfolio as on 30 June 2019 stood at 7,635 accounts.

During the period, the company was the 2019 Investment Trends Winner. It also received 2019 Fintech Business Awards. The independent surveys along with these awards prove that CL1 provides the best cloud solution for SMSF administration. In order to accelerate market share growth and extend the lead over its competitors, the company feels that it needs to focus on the product development. For this, it would be working on improving its sales, marketing and product development capability for creating a gap between itself and its competitors.

Class Portfolio did not perform as per the expectation in FY2019. There were insufficient investments which indicate that the customerâs pain points were not addressed during the period. Now, the company has plans to expand its product suite with Class Trust, as trusts are the primary wealth vehicle apart from SMSF. The company would soon be launching a new product that would enable in increasing its addressable market.

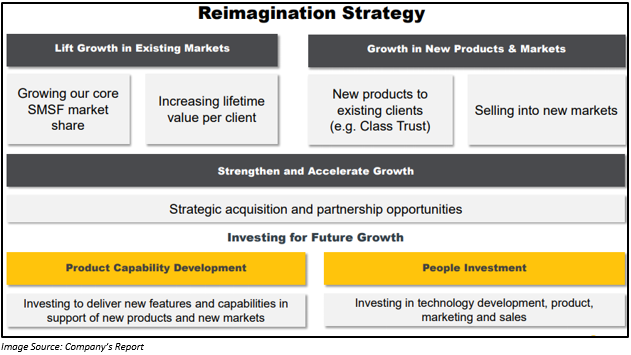

Reimagination Strategy:

The company would focus on lifting growth in the existing markets. It would also work towards the growth in new products and markets.

Outlook

CL1 in FY2020 would be increasing its investments in product development and technical capability by 33% to $12 million. Moreover, the company expects material growth in revenue as well as EBITDA performance in FY2021 and beyond that.

DWS Limited

DWS Limited (ASX: DWS), a provider of IT services, has an annual dividend yield of 7.08%, as on 03 September 2019. The shares of DWS opened at a price of A$1.060, down by A$0.070 from its previous closing price. By the end of the dayâs trading on 03 September 2019, the closing price of the stock was A$1.070, down by 5.31% as compared to its last closing price. DWS has a market cap of A$148.97 million with approximately 131.83 million outstanding shares and a PE ratio of 14.490x.

FY2019 Highlights:

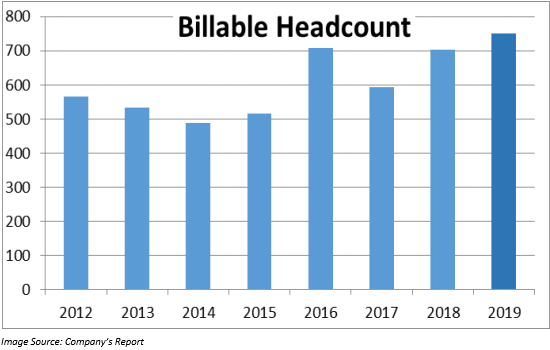

Operating revenue of the company increased from $126.1 million in FY2018 to $163.5 million in FY2019, which was primarily driven by the acquisition of Projects Assured. Underlying EBITDA grew by 15.7% to $26.4 million. However, EPS declined from 12.1 cents in FY2018 to 7.8 cents in FY2019, which was the outcome of accounting treatment for costs related with the Projects Assured acquisition as well as investment in RPA and licensed products. The total billable consultants increased during the period and stood at 751 by 30 June 2019. It was driven by constant focus on productivity as well as management of consultant numbers and acquisition of Projects Assured.

The balance sheet of the company remained healthy, with a cash position of $8.88 million as on 30 June 2019. Net debt in FY2019 was $33.12 million. The company unveiled total dividend for FY2019 at 8 cents per share.

Outlook

- DWS would monitor investment in licensed products during FY2020, in order to ensure that the business registers satisfactory progress or alternatively lowers investment or exit.

- DWS would aim at taking advantage from its core and acquired businesses in order to grow and diversify earnings, pay down acquisition debt and provide appropriate shareholder returns.

Reckon Limited

Reckon Limited (ASX: RKN), a provider of financial management software, has an annual dividend yield of 9.09%, as on 03 September 2019. The shares of RKN opened flat at A$0.660 and traded flat on ASX on 03 September 2019. The company has a market cap of A$74.77 million with approximately 113.29 million outstanding shares and a PE ratio of 9.57x.

FY2019 Highlights:

On 20 August 2019, RKN released its FY2019 results for the half year ended 30 June 2019. Revenue in 1H 2019 declined by 1.8% to $39.2 million as compared to previous corresponding period (pcp). However, EBITDA increased by 4.3% year-on-year to $17.1 million and NPAT grew by 2.1% year-on-year to $5.3 million.

The period witnessed a strong cash flow which resulted in the reduction of net debt by $7 million in 1H 2019. The bank facilities also got extended for another 3 years. The board declared a fully franked interim dividend of 3 cents per share which would be paid to the shareholders on 18 September 2019.

Adacel Technologies Limited

Adacel Technologies Limited (ASX:ADA), a developer of advanced simulation and control systems for aviation and defence, has an annual dividend of 7.07%, as on 03 September 2019. The shares of ADA traded last on 02 September 2019 and closed at a price of A$0.495. ADA has a market cap of A$37.74 million and ~ 76.25 million outstanding shares.

FY2019 Highlights

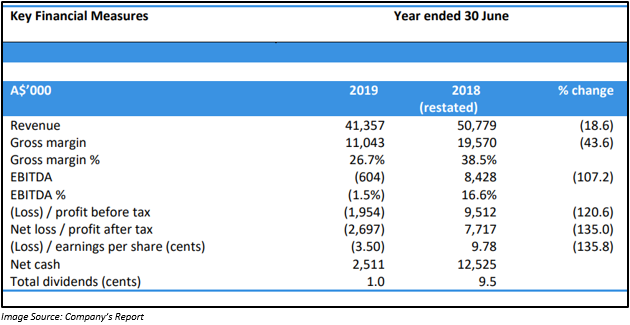

On 14 August 2019, ADA released its full year results for the period ended 30 June 2019. Revenue from continuing operations declined by 18.6% to $41.36 million. A significant decline of 107.2% was registered in EBITDA to A$0.604 million. ADA incurred a loss before tax of $1.954 million. EPS declined by 135.8% to 3.50 cents per share. The total dividends for FY2019 was 1 cent per share.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.