Centrica PLC (LON:CNA) reported full-year results for 2019 period ended 31st December 2019, due to challenges faced by the company in the prevalent economic scenario, the operating profit and earnings were materially impacted in the year. The companyâs performance was impacted by the implementation of the default tariff cap in the United Kingdom and natural gas prices going south. However, Centrica managed to deliver growth in customer accounts against this backdrop. The company did well in attaining significant cost efficiencies and full-year adjusted operating cash flow and net debt in line with targets along with higher net promoter scores, which is a tool to measure customer satisfaction.

The companyâs performance in the second half of the fiscal year 2019 was better than the companyâs performance in the first half of the fiscal year, and the company shall carry the same momentum in 2020. As the lower commodity price environment could impact Upstream earnings in the fiscal year 2020, the company looks forward to deriving earnings from core customer divisions. However, the company practices financial discipline and shall opt for a prudent approach to find the right balance between cash flow and resources in the fiscal year 2020.

The company aims to reposition itself when it comes to customer relationships, energy solutions and looks forward to helping customers shift to a lower carbon emission future in the fiscal year 2020.

(Companyâs filings, London Stock Exchange)

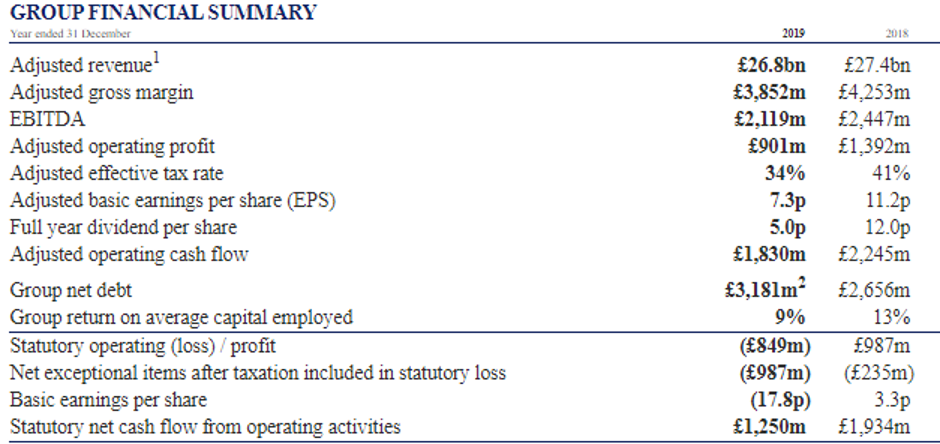

The companyâs adjusted revenue was recorded at £26.8 billion in the fiscal year 2019. The companyâs adjusted gross margin fell by 9 per cent to £3,852 million and adjusted operating profit fell by 35 per cent to £901 million during the period in comparison to the fiscal year 2018.

The adjusted gross margin (consumer) and adjusted operating profit were down by 11 per cent and 33 per cent respectively in comparison to the fiscal year 2018 for Centrica Consumer segment, which includes the negative impact of £300 million from the implementation of the UK residential energy supply default tariff cap. In addition, Centrica Consumer attained cost efficiencies of £229 million.

The adjusted gross margin and adjusted operating profit were up by 17 per cent and 189 per cent respectively in comparison to the fiscal year 2018 for Centrica Business segment, due to significant improvement achieved in power retail margins in North America, followed by a benefit from the decision to defer delivery of gas from 2019 into 2020 from the one remaining large legacy gas contract along with good European trading and optimisation performance. Furthermore, Centrica Business delivered £40 million of cost efficiencies in 2019.

The adjusted operating profit from Upstream was down by 68 per cent to £179 million. Due to extensions to outages at the nuclear power stations, the adjusted operating profit (Nuclear) was down by 59 per cent to £19 million. The adjusted operating profit from Exploration & Production was down by 69 per cent to £160 million due to the lower wholesale commodity price environment.

The companyâs Adjusted earnings attributable to shareholders went down by 34 per cent to £419 million, and adjusted EPS fell by 35 per cent to 7.3 pence during the period. The companyâs total statutory gross profit was down by 21 per cent to £3,206 million in FY19. The statutory gross profit includes the impact of an increased reported loss from a decline in gas prices on energy procured to meet the future requirements.

The companyâs statutory operating loss was £849 million in FY19 compared to a statutory profit of £987 million in FY18 reflecting the loss from certain re-measurements and higher exceptional charges and lower adjusted operating profit. The statutory loss of the company attributable to shareholders for the period was £1,023 million in FY19 compared to a profit of £183 million in FY18, after factoring net finance costs and taxation. The companyâs statutory basic EPS loss was recorded at 17.8 pence in FY19 as compared to the statutory earnings per share of 3.3 pence in FY18.

The Company is well placed for the long-term and focuses on being a leading Energy Services and Solutions provider in a rapidly changing world of energy.

Business overview: Centrica PLC

Centrica PLC (LON:CNA) is a British energy and services corporation based in Windsor, Berkshire. The company is primarily engaged in the supply of power and gas to businesses and consumers, and its target market includes the United Kingdom, Ireland and North America. It is the owner of British Gas, which is the largest energy provider in the United Kingdom, and along with five other power supplying company, it's a part of Britain's âBig Six' energy suppliers. The company is a constituent of the FTSE 100 index.

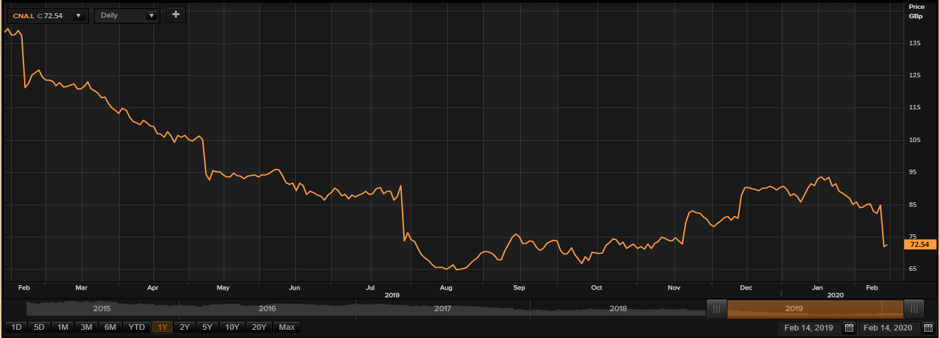

Centrica PLC -Stock price performance

Daily Chart as on 14-February-20, before the market closed (Source: Thomson Reuters)

On 14th February 2020, while writing at 11:53 AM GMT, Centrica PLCâs shares were clocking a current market price of GBX 72.54 per share. The companyâs market capitalisation was at £4.15 billion at the time of writing.

On 20th February 2019, the shares of Centrica PLC have touched a new peak of GBX 140.70 and reached the lowest price level of GBX 63.99 on 14th August 2019 in the last 52 weeks. The companyâs shares were trading at 48.44 per cent lower from the 52-week high price mark and 13.36 per cent higher than the 52-week low price mark at the current trading level as can be seen in the price chart.

The stockâs traded volume was hovering around 22,269,227 at the time of writing before the market close. The companyâs 5-day stock's daily average traded volume was 46,269,036.40; 30 days daily average traded volume- 23,666,905.67 - and 90-days daily average traded volume â 23,565,535.43. The volatility of the companyâs stock was 20 per cent lower as compared with the index taken as the benchmark, as the beta of the companyâs stock was recorded at 0.80 with a dividend yield of 6.96 per cent.

The shares of the company have delivered a negative return of 3.60 per cent in the last quarter. The companyâs stock plunged by 19.57 per cent from the start of the year to till date. The companyâs stock has given investors 48.05 per cent of a negative return in the last year.Â