Turners Automotive Group Limited (ASX: TRA) provides a set of solutions across Automotive Retail, Finance and Insurance, as well as Credit Managemnt and is a leading player in the New Zealand automotive sector.

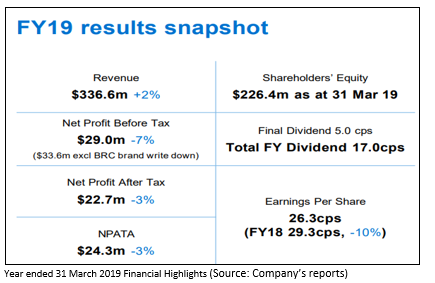

Looking at the financial performance. Turners reported a net profit before tax (NPBT) of $29 million for FY19. Setting aside a non-cash adjustment related to the rebranding of Buy Right Cars of $4.6 million, the companyâs FY19 NPBT stood at $33.6 million, which was more compared to Q4 guidance of $32 million and last year result of $31.1 million. The NPAT for the year amounted to $22.7 million, and revenue equalled to $336.6 million, up 2% from $330.5 million in FY18. The companyâs EPS has reduced to 26.3 cents per share from 29.3 cents per share in FY18.

A final quarterly fully imputed dividend of 5 cents per share was announced, resulting in a rise in full year dividend from 15.5 cents per share in PY to 17 cents per share in CY. The Directors also resolved to increase the previous pay-out ratio of 50%-60% to 60%-70%, following the strategy review.

The companyâs balance sheet position was characterised majorly by a reduction in cash balances due to the investment of insurance reserves and an increase in property, plant and equipment owing to the development of new sites.

Plans in Pipeline

Turners currently has a network of 33 sites across New Zealand and has assigned a proportion of its Insurance business to support retail expansion. It is planning to open a new North Shore branch by the end of 2Q â20 and seven more sites with two already having contracts in place.

Funding Strengthened

Turners issued a $25 million, three-year bond programme, which combined with the Securitisation Warehouse and the banking syndication with the ASB and BNZ, will help the company achieve the targeted growth.

Market credentials

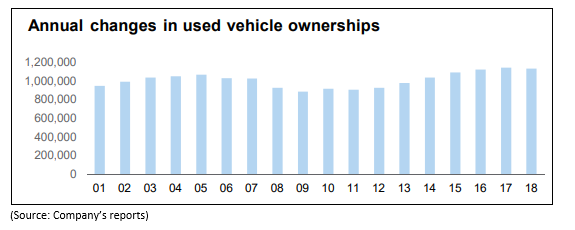

New Zealand used car market showcased remarkable performance with a demand of over 9.5 million cars at 20+ years old. The performance in the second half of the year was due to improved trading performance and vehicle margins in the fourth quarter of FY19.

The Auckland market was characterised by moderate demand and pressure on used vehicle import margins. While the excessive supply of import cars temporarily plummeted the prices and increased compliance costs, the local stock delivered stronger margins.

Segment-wise performance

Automotive Retail â The segment generated 67% operating revenue and 63% operating profit. It exhibited a 13% rise in operating profit (offsetting the downturn in Buy Right Cars impacted by the soft Auckland market).

Finance â This segment exhibited an 11% increase in operating revenue to $44.2 million and a marginal decrease in operating profit to $11.1 million due to change in accounting standards and Motor Trade Finance non-recourse offering. In FY19, the company added $28 million in new loans to Oxford Finance loan book.

Insurance â Autosureâs operating revenue rose by 3% to $48.5 million and operating profit rose by 126% to $8.2 million, including a gain on sale of an investment property.

Credit Management â EC Credit Control recorded a revenue of $18.2 million and operating profit of $6.3 million, up 4% as compared to FY18.

Strategy and outlook

As a part of its new strategy, Turners aims to focus on the core business of Automotive Retail and conduct a strategic review of Oxford Finance to consider alternative ownership options. The company is also planning to conduct a review of EC Credit in the next one to two years. In the coming years, Turners intends to expand its national network, develop in-house property expertise and enhance capital efficiency.

The stock of TRA last traded at $2.100, with a market cap of $182.46 million.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.