This article talks about three stocks from the real estate space. Two of these companies, Villa World Limited (ASX: VLW) and AVJennings Limited (ASX: AVJ), are engaged totally in the development & sales of residential real estate. Meanwhile, Charter Hall Group (ASX: CHC) is an integrated property REIT, with a portfolio of Office, Industrial, Retail & Social Infrastructure.

Residential developers have depicted the signs of persisted slowdown during the last year in their recently released full-year results. However, REITs and commercial developer like Charter Hall Group has posted decent results, but with a slightly lower profit compared to the previous year.

Meanwhile, the green shoots have been acknowledged by the residential developers in the industry, which is backed by fiscal measures, and monetary stimulus. Villa World mentions that tax offsets, falling interest rates, improvement in credit availability, and the governmentâs focus on first-home buyers provide upside to the residential businesses.

Concurrently, AVJennings noted that the gloomy property days are over, and market sentiments have started to improve driven by favourable market fundamentals of tax cuts, rate-cuts along with relaxation in minimum mandatory servicing requirement by APRA for retail banks, which would be considered while assessing mortgage applications.

Charter Hall Group (ASX: CHC)

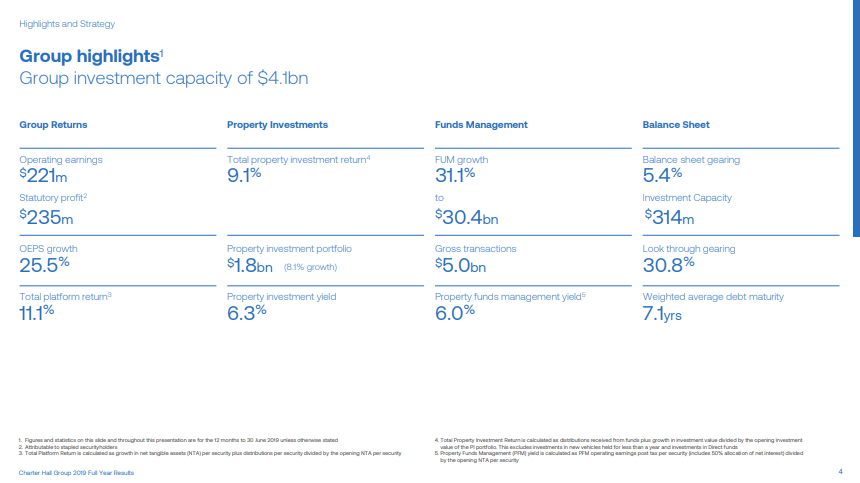

On 20 August 2019, the company announced results for the FY19 period ending 30 June 2019. Accordingly, the revenues of the group stood at $378.5 million in FY19 compared with $246.2 million in FY18. The statutory profit of the company was down by 6% to $235.3 million in FY19 compared with $250.2 million in FY18.

Meanwhile, the group distributed AU 33.7 cents per security in distribution during FY19, up by 6% from AU 31.8 cents per security in FY18. Besides, the group raised $3.4 billion of gross equity issues during the year and deployed $5 billion in gross transactions. Importantly, the funds under management stood at $30.4 billion as on 30 June 2019, an increase of $7.2 billion over the previous corresponding period.

Highlights (Source: CHCâs FY19 Results - Presentation)

Property Investment & Funds Management

Reportedly, the property investment portfolio generated a total property investment return of 9.1% while portfolio increased to $1.8 billion. The occupancy was at 97.7% with Weighted Average Lease Expiry (WALE) of 7.6 years.

Meanwhile, funds management portfolio (FUM) grew to 844 properties with 3,419 tenancies, WALE of 8.2 years, and delivered a net rental income of $1.7 billion. Besides, the FUM was driven by acquisitions, positive revaluation of $1.2 billion while capex on developments was $1 billion.

Balance Sheet

Reportedly, the company had $6.3 billion of new and refinanced debt facilities with no material maturities in FY20 period. The weighted average maturity of the debt was 7.1 years with balance sheet gearing of 5.4% (net of cash). Besides, the group had cash of $114 million as on 30 June 2019.

Outlook & Strategy

As per the release, the group anticipates achieving 18-20% growth in post-tax operating earnings per security in FY20, considering no material change in current market conditions. The FY20 guidance included CHOT performance fees of $132 million, payable in April 2020, and $50 million was accrued in FY19 earnings.

Besides, the group expects to report 11-13% growth in post-tax operating earnings per security during FY20 over FY19, after removing the impact from CHOT performance fees. Further, it expects to deliver a distribution growth of 6% over FY19.

On 20 August 2019, CHCâs stock last traded at A$12.4, up by 3.161% from the previous close.

Villa World Limited (ASX: VLW)

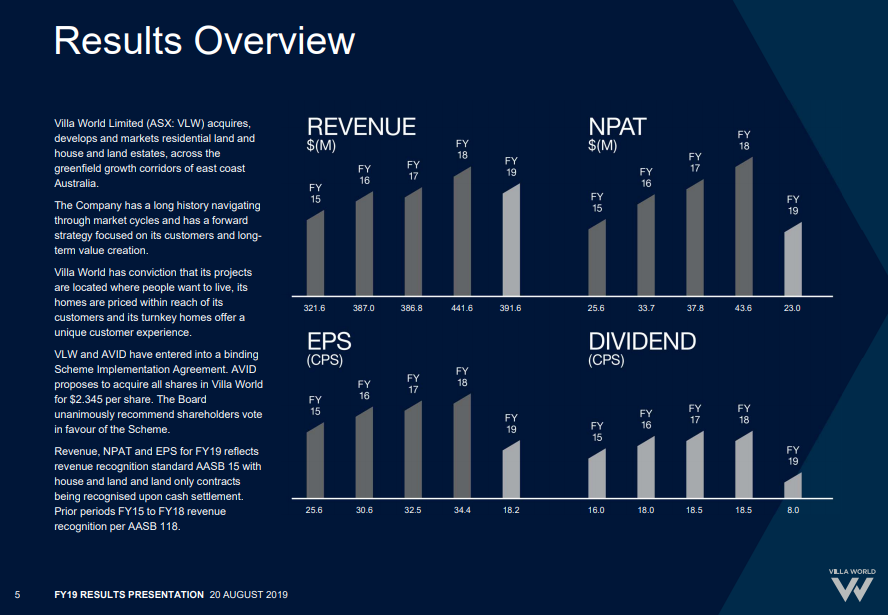

On 20 August 2019, the company declared results for the full year ended 30 June 2019. Accordingly, the company reported revenues of $391.6 million in FY19 compared with revenues of $441.6 million in FY18. Besides, the statutory profit after tax was at $23 million in FY19 against $43.6 million in FY18.

Results Overview (Source: VLWâs 2019 Full Year Results Presentation)

Acquisition

Reportedly, the company is amid acquisition by AVID, and it had entered into a Scheme Implementation Agreement with AVID. AVID has proposed to acquire all of the shares for a consideration of $2.345 per share.

Besides, if the scheme is approved and applied, the board of the company proposes to declare a special dividend (fully franked) of 31 cents per share. Subsequently, the scheme consideration will be reduced to $2.035 per share if the special dividend is declared. Further, the company expects to dispatch Scheme Booklet in September 2019, and the shareholders would be able to vote on it by mid-October 2019.

Operating Performance

As per the release, the revenues were driven by cash settlement of strong carried forward sales along with increases in average revenue per lot. The reported gross margin was down to 23.7% in FY19 from 25.2% in FY18 but within the companyâs range of 23-25%. Meanwhile, the company has been engaged in joint venture arrangements, which delivered a fee income of $1.3 million, and the share of profit from the JV stood at $2.1 million.

Balance Sheet

Reportedly, the company had net tangible assets of $285.5 million in FY19, which equates to NTA per share of $2.28 per share, up from $2.44 in FY18. The net debt of the company stood at $115.3 million, down from $171.1 million in FY18, and the gearing was down to 24.1% at the year end 2019 from 29.7% during previous year end.

Outlook

As per the release, the company intends to focus on operational delivery, along with cash settlement of carried forward sales. It would continue to manage the business cost structure due to current trading conditions, and cost-optimisation in 2HFY19 to be realised in FY20.

Meanwhile, the company would focus on improving sales during the FY20, and it expects gross margin to be in the range of 23-25%. Besides, the development management fee revenues from JVs would be consistent.

On 20 August 2019, VLWâs stock was at A$2.35 by the closure of the trading session, up by 0.427% from the prior close.

AVJennings Limited (ASX: AVJ)

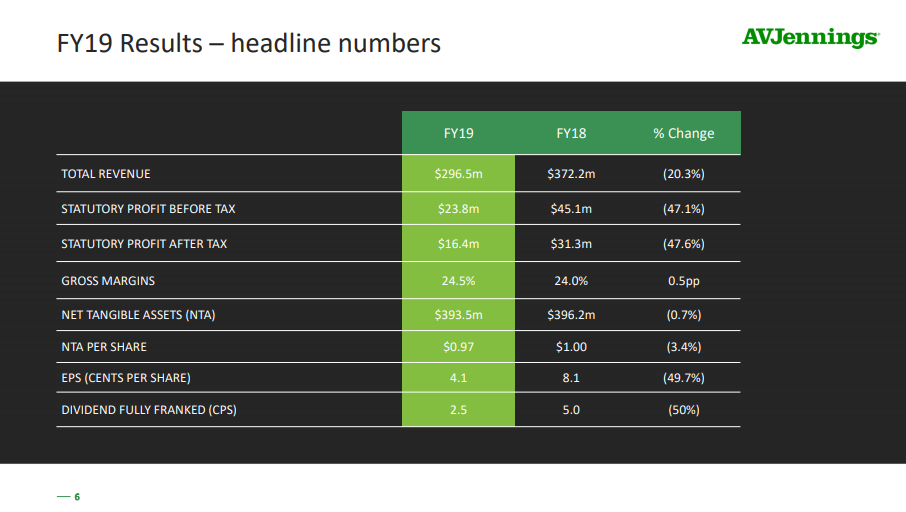

On 20 August 2019, the company announced results for the year ended 30 June 2019. Accordingly, the revenues of the company stood at ~$296.46 million down by 20.3% in FY19 compared with ~$372.16 million in FY18.

Highlights (Source: AVJâs FY19 Results Presentation)

Meanwhile, the profit after tax was down by 47.6% to $16.43 million in FY19 against $31.34 million in FY18. Besides, the company has declared a fully franked dividend of AU 1.5 cents per share payable on 20 September 2019. The divided would be ex on 5 September 2019 with a record date on 6 September 2019.

Reportedly, the subdued profit was the result of softer market conditions majorly in Melbourne & Sydney. The settlement of contracts signed during the previous periods allow to improve the results of the company, and these contracts carried favourable margin from the project in Victoria & New South Wales.

Besides, the land inventory of the company rose to 9,531 lots in FY19 compared to 9,373 in FY18 at the year end. The residential developer had signed an agreement to advance a 3,500-lot greenfield site at Caboolture.

As per the release, the company had 1600 lots under development as of 30 June 2019, which were 18% less than FY18 year end. The company had settled and initiated the development of Ara Hills in New Zealand along with the acquisition of the remaining 50% interest in âRivertonâ in Jimboomba, Queensland.

Consequently, the net debt climbed to $182.1 million as on 30 June 2019 compared to $130.7 million in the previous corresponding period. Besides, the gearing was at 26.6% as of 30 June 2019 compared to 20.4% in pcp, but within the companyâs range of 15-35%.

Outlook

Reportedly, the company noted that customer visits at sales offices & online had seen some improvement, and it expects this trend to continue over FY20. Besides, the company has advanced a number of existing projects, particularly in South-East Queensland, and it would improve the number of projects actively selling in FY20 period.

On 20 August 2019, AVJâs stock last traded at A$0.575, down by 0.862% from the last close.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.