_07_03_2026_03_50_21_133108.jpg)

Summary

- The competition is rising in the Australian market to offer a low-interest rate to the borrowers. The lenders in the market are giving less than 2 per cent variable interest rates on new mortgages, while the smart borrowers are getting opportunities to compare and choose.

- Coronavirus pandemic may have caused a reduction in new mortgages, but the number of homeowners shifting towards new lenders, with low-interest rate has increased.

- Federal and State Government housing initiatives are helping home buyers to fulfill their aspiration of home-ownership through schemes like- The First Home Loan Deposit Scheme, The First Home Owner Grants, The First Home Super Saver Scheme and The HomeBuilder Scheme.

A new full-fledged war on home loan interest rate has broken out in Australia.

Just when Australia had begun to celebrate its win over novel coronavirus pandemic, COVID-19 cases started resurfacing. On 31 July, Victoria recorded 627 fresh cases in last 24 hours, with 8 deaths.

In the month of March, Reserve Bank of Australia (RBA) officially slashed cash rate by 0.25 per cent in response to tackling the coronavirus crisis. However, many lenders did not initially approve to pass on the cut to their existing home loan customers.

The scenario changed in just a few months down the line. Currently, the lenders are competing over variable interest rates even below 2 per cent for the first time. As the competition flares-up in Australia for new mortgages, people have started taking advantage of it.

The lenders in the market are giving less than 2 per cent variable interest rates on new mortgages, the smart borrowers are getting opportunities to compare and save money.

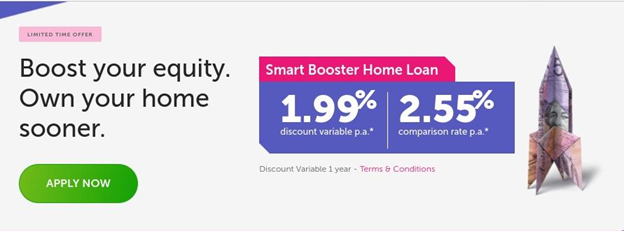

Online lender, loans.com.au is offering 1.99 per cent variable on home loan rate for owner-occupied purchasers and refinancers, which would be applicable for borrowers paying principal and interest repayments with a security of 20 per cent or more. The discounted rate is only for a year, starting from the second year the rate reverts to 2.57 per cent. The offer is also time limited.

After the announcement from this smaller fintech lender, competition for new mortgages seems to have intensified.

Also read: Housing market revives, home loan lending rates accelerate

Image source: loans.com.au

Let’s now glance at the 3 untouched aspects pertaining to Home Loan.

Competition Build Up:

Australia And New Zealand Banking Group Limited (ASX:ANZ) home loans since June1 are offering up to $1,000 cashback for eligible first home buyers with home loans over $250,000. This offer includes State or Territory government first home buyer concessions recipients. That too for single property purchase for an owner-occupier purpose.

Suncorp Bank, a subsidiary company of Suncorp Group Limited ASX:SUN since May is also offering cashback on home loan refinance segment. The offer is up to $4,000 for health, education, and emergency services workers with eligible home loans. The bank executives said that this is another way for them to extend gratitude towards frontline workers. Also, Suncorp is offering cashback of up to $3000 to mortgage consumers.

Industry experts believe that the lenders are finding innovative ways to attract homeowners to refinance the new home loan rate. The pandemic may have caused a reduction in new mortgages, but the number of homeowners shifting towards new lenders with low-interest rate has increased.

An Array of Government Grants and Schemes

People’s home ownership dreams may also benefit from various Federal and State Government housing initiatives.

- The First Home Loan Deposit Scheme (FHLDS)

- The First Home Owner Grants (FHOG)

- The First Home Super Saver Scheme (FHSSS)

- The HomeBuilder Scheme

Under The First Home Loan Deposit Scheme (FHLDS), a borrower can get home loan options from 27 lenders. This scheme was launched by the Australian Government to support eligible first home buyers purchase their first home sooner. Under which, the buyer can buy a modest home with a deposit of as low as 5 per cent.

A $10,000 First Home Owner Grant (FHOG) is provided when one buys or build first new home valued at $750,000 or less. The grant is not available for an investment property or holiday home. Also, if one is constructing a house in regional Victoria, the grant is of $20,000.

Under HomeBuilder scheme, the government assist eligible owners or occupiers with a grant of $25k to construct a new house or refurbish the existing one. First home buyers can also avail a scheme introduced by the Australian Government to reduce pressure on housing affordability.

The First Home Super Saver (FHSS) scheme helps buyers save money on their first home inside the super fund. It also helps the buyers save their funds quicker with the concessional tax treatment of superannuation.

With various government schemes accessible in the market, homeowners can take advantage of it along with the new home loan interest rates.

Non-Major Banks Participation:

Australia and New Zealand Banking Group Limited (ASX:ANZ), Commonwealth Bank of Australia (ASX:CBA), National Australia Bank (ASX:NAB) and Westpac Banking Corporation (ASX:WBC) are the big four banks in Australia, which dominate the market in home loan category, with 80 per cent of all residential mortgages. If we compare the interest rates of these banks with smaller organisations, they appear to be a bit higher.

Industry experts believe that customer-owned banks can pass on profits to their customers in terms of lower rates and fees.

A non-major bank, Bendigo and Adelaide Bank Limited (ASX:BEN) is now offering Complete Home Loan to the customers. It comes with an optional 100 per cent offset on all fixed and variable loan products. The offer also extends online redraw facilities and flexible repayments. According to the bank, this specially crafted product is what market needs in the current pandemic situation.

Last month, Auswide Bank Ltd (ASX:ABA) released a new product keeping Australia’s current requirement on priority. A non-major bank offers homeowners/ occupiers access to “no fuss” loan, with low variable interest rate and free online redraw. The bank is also providing certain features to help repay loan amount earlier than the decided timeframe.