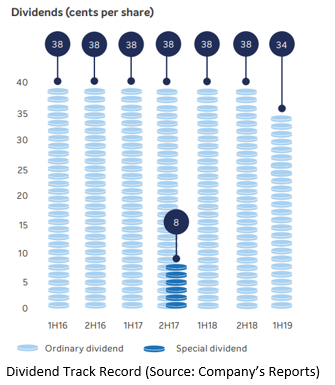

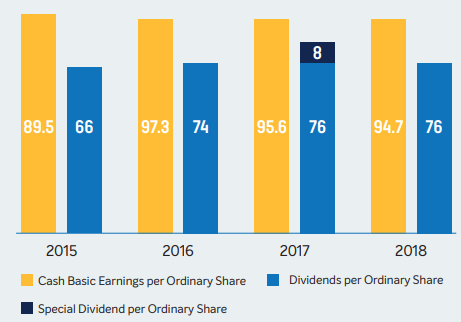

Bank of Queensland Limited (ASX: BOQ) is one of Australia's leading regional banks with more than 180 branches across Australia. The company has been rewarding its shareholders with a strong dividend track record. Currently, the annual dividend yield for the stock stands at 7.89%.

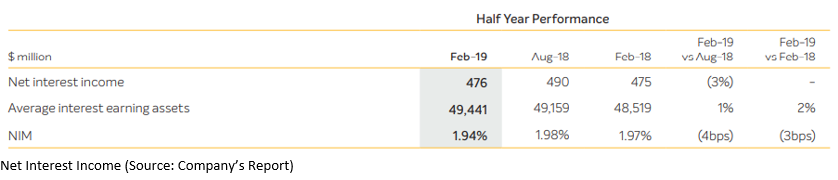

The bankâs NII (Net interest income) decreased by $14 million from the second half of FY18 and increased $1 million from the first half of 1H â18. It was primarily led by a 4 bps decline in NIM from the second half of FY18 and 3 bps decrease as compared with 1HFY18. Average interest earning assets were 1% up as compared to 2HFY18, and 2% up as compared to 1HFY18. Adjusting for the lower number of days in 1HFY19 as compared to 2HFY18 would contribute an extra $8 million (that is 2% higher) in underlying NII in 1HFY19.

Asset pricing and mix witnessed a flat performance over 1HFY19. Loan repricing actions attributed in favour of NIM by 4 bps. Offsetting the re-pricing impact benefits were the higher competitive environment for new loans, especially in key owner-occupied segments, increased retention discounting and lower interest income.

Funding costs led the higher NIM by 2 bps. The ongoing optimisation of the BOQâs retail deposit mix, along with a deposit growth strategy focused on transaction and savings accounts, benefited the funding costs. Wholesale funding costs were a tad down, with BOQ taking the opportunity to raise its long-term wholesale issuance in the starting phase of 1HFY19, before an upside in long-term wholesale credit spreads.

Margin pressure in 1HFH19 intensified due to growing competition for new lending as a result of lower system credit growth and higher hedging costs on the back of the elevated bank bill swap rate. These bearings were partially offset by the mortgage repricing, which started in July 2018 and January 2019 and lower funding costs. Net results came in the form of a decline in NIM in 1HFY19.

Annualised credit growth was 2% in 1HFY19 in a market characterised by slow loan growth, rising competition and a change in a regulatory environment. The Bank has continued to balance the growth with margins and asset quality. The Bank has adopted a strategy to target niche customer segments, which has delivered significant growth across BOQ Finance, BOQ Specialist and niche segments in the Bankâs branded commercial portfolio mix. Virgin Money mortgage has witnessed a strong growth, which is now comprised of a home loan portfolio of greater than $2.1 billion.

Annualised credit growth was 2% in 1HFY19 in a market characterised by slow loan growth, rising competition and a change in a regulatory environment. The Bank has continued to balance the growth with margins and asset quality. The Bank has adopted a strategy to target niche customer segments, which has delivered significant growth across BOQ Finance, BOQ Specialist and niche segments in the Bankâs branded commercial portfolio mix. Virgin Money mortgage has witnessed a strong growth, which is now comprised of a home loan portfolio of greater than $2.1 billion.

Looking at the hedging costs, the impact of hedging costs was higher in 1HFY19, primarily on the back of hedging costs, with basis portfolio spreads rising from an average of 34 bps to 46 bps as compared to 2HFY18. It has driven a 3 basis points decrease in net interest margin.

At the current market price of $9.050 (as on 24 May 2019), the stock is available at the price to earnings multiple of 11.410x. The annual dividend yield for the stock stands at 7.89%, with a market capitalisation of ~$3.7 billion. The stock has generated a negative return of 11.54% in the last one-year.

(Source: Company Reports)

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.