During the pandemic and the ensuing lockdown, the banking sector remained operational, while many struggled with their business, one of the banking major concentrated on improving its operational efficiencies. The LLOYD BANKING GROUP Plc emphasised on strengthening its digital experience. The bank, despite going through the devastation, holds a competent business model and has sufficient headroom to grow.

- The bank has been enhancing customer experience and digital capabilities, with a surge in the adoption of digital services by its customers.

- With the launch of a new Scottish Widows branded equity release mortgage, the Group has also designed schemes that maximise the Group's capabilities for the benefit of its customers

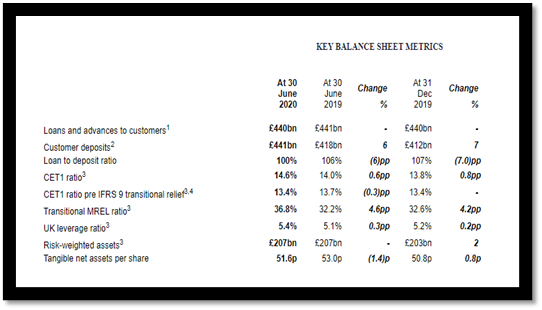

- The Group holds a strong balance sheet, with loans and advances of £440 billion

Lloyd Banking Group has invested its previous six months, during the lockdown in enhancing customer experience and digital capabilities, with a surge in the adoption of digital services by its customers. The bank is the UK's leading digital bank with 17 million active customers. The daily logins exceeded 11 million presently, an increase of 12 per cent on the prior year. The Group’s extraordinary Single Customer View has been expanded to include stock-broking portfolios, with over 6 million customers now being able to access their insurance and savings products alongside their bank accounts. The digital net promoter score of 69 has been the highest at all times, up 8 per cent in H1 2020, despite increased usage levels.

The company has rolled out new features to improve its mobile app in order to further enhance the functionality and accessibility of its services, which includes the transaction search functionality, and ability to use biometrics to allow new payments. In the Commercial category, approximately £350 million of payments per month are now being processed through a payables API launched in 2019, enabling business clients to send Faster Payments directly from their systems.

With the launch of a new Scottish Widows branded equity release mortgage, the Group has also designed schemes that maximise the Group's capabilities for the benefit of its customers, enabling its retail customers to use the equity in their home to help their family members onto the housing ladder or supplement their own retirement income.

Recent Financial Highlights (H1 2020)

The Group adapted with the situation of the lockdown swiftly, and the employees were willing to adopt new ways of working and collaborate remotely to support customers. The business has remained fully operational throughout the pandemic, and the Group’s technology infrastructure has contributed towards performing well under significant pressure. With 90 per cent of branches operating all through the coronavirus outbreak, the digital banking segment had performed well during the first half of the year, witnessing a significant increase in usage, achieving all-time high user feedback scores.

The operations of the company remained resilient, making strategic progress, primarily focusing on supporting its customers during the exceptional and challenging period. The benefits of investment made over the course of the third strategic phase, especially in digital, transformation and Single Customer View have helped the Group in positioning them well during the pandemic.

Industry Overview

The banking sector is one of the oldest sectors of the British economy. It covers the retail and commercial banking activities of deposit-taking institutions. Retail and commercial banks are involved in activities such as accepting deposits from and making loans to individuals and businesses. The primary sources of revenue generation for banks are charging interest on loans, while non-interest income from card fees and overdraft fees represents a secondary source of revenue.

The banking industry has seen various market cycles as the UK economy has now fallen into recession, low business confidence and an anticipated drop in business profit across most businesses will constrain commercial lending activity. The ongoing uncertainty created by the EU referendum surrounding the UK's future relationship will add further negative pressure to business morale. The industry was expanding at a moderate pace prior to the outbreak of the coronavirus. In the short term, the banking sector is expected to be subject to massive disruption. However, in the next five years, the industry is anticipated to recover gradually.

Lloyds Banking Group PLC, The Royal Bank of Scotland Group PLC, Barclays PLC and HSBC Holdings PLC are some of the companies holding the largest market share in the banks in the UK industry.

Lloyds Banking Group PLC (LON:LLOY) main focus includes activities such as retail, general insurance, commercial and corporate banking, pension and investment services, offering services through a number of well-known brands which includes Scottish Widows, Halifax, Bank of Scotland, Lloyds Bank, and a range of distribution channels. Headquartered in London, UK, Lloyd is the largest of the UK's retail bank. The Group is listed on the FTSE 100 index of the London Stock Exchange as well as the New York Stock Exchange.

Factors for growth

Robust Balance Sheet With High Levels Of Security- The Group holds a strong balance sheet, with loans and advances of £440 billion, an increase of £29 billion in customer deposits and CET1 ratio of 14.60 per cent. It is positioned well to absorb the Covid-19 ramifications.

Strong Funding And Liquidity Position- The Group has a strong liquidity position, with a loan to deposit ratio of 100 per cent, showing a significant potential to lend into recovery.

Loan Book Managed Carefully- The Company’s loan book was standing at £440 billion, remaining unchanged from the end of 2019, marginally behind the same point the year before.

The economic outlook remains largely uncertain and challenging since the Group’s first-quarter results. However, the Group's has witnessed early signs of recovery in core markets with the increased consumer spending levels, housing market activities re-energised, and the economy returning to growth, with the gradual easing of social distancing measures.

The Group has updated guideline for 2020, reflecting a proactive response to the challenging economic environment, based on the recently revised current economic assumptions.

- Net interest margin is expected to remain broadly stable on Q2 level at approximately 240 basis points for the rest of the year, resulting in a full year margin of approximately 250 basis points.

- Operating costs is estimated to be below £7.6 billion.

- Impairment charges are expected to be between £4.5 billion and £5.5 billion.

- Risk-weighted assets expected to be flat to modestly up, in comparison with H1 2020.

The Group witnessed significant deposit growth from the strong franchise and Government schemes. The Company has shown impressive growth in the last four years (FY15-FY19), indicating sound financial health and business model, and having sufficient headroom to grow. This will ensure that the Group can continue to support its customers and help Britain recover. However, the economic fragility will continue for at least the rest of the year.

Key Risks

The risk of a significantly prolonged recovery in the economic activity and a larger-than-anticipated dent on demand could even result in stresses surpassing the Group’s estimates.

Advancements in technology have proved to be helpful in bridging the gap between lenders and borrowers, resulting in the banks losing their monopoly position. The emergence of the P2P sector might disrupt the banking sector operations. The appearance of cryptocurrencies also poses a threat to the banking sector with the concept of a global currency.

The central banks are phasing out LIBOR (London Inter Bank Offered Rate) benchmark interest rate. According to top central bankers in Britain and the United States, the lenders and borrowers are expected to undergo transition by the end of 2021.

1 Year comparative share price chart of LLOY with FTSE 100

Image Source: Thomson Reuters